Living off dividends means building a robust investment portfolio that generates consistent passive income to cover your living expenses, and at money-central.com, we can show you how. This approach offers financial freedom, allowing you to separate your income from your working hours, and with strategic dividend investing, you can achieve financial independence and a secure retirement income stream. Let’s explore the financial planning and wealth management principles that make this lifestyle possible, including income streams, financial security, and retirement planning.

1. Understanding the Basics of Living Off Dividends

Living off dividends is a financial strategy where you invest in dividend-paying stocks, exchange-traded funds (ETFs), and mutual funds to generate a steady income stream. This income covers your living expenses, potentially eliminating the need for a traditional job. Let’s explore the mechanics of this strategy.

1.1. What Are Dividends?

Dividends are distributions of a company’s earnings to its shareholders, typically paid out quarterly. They represent a portion of the company’s profits that are returned to investors as a reward for owning the stock. This payment is in addition to any potential capital appreciation of the stock’s price.

1.2. How Do Dividends Work?

When a company earns a profit, it can choose to reinvest the money back into the business or distribute it to shareholders as dividends. The board of directors decides on the amount and frequency of dividend payments. Once declared, dividends are paid to shareholders on a per-share basis. For example, if a company declares a dividend of $1 per share, an investor owning 100 shares would receive $100.

1.3. Types of Dividend-Paying Investments

Several investment options can provide dividend income, each with its own characteristics:

-

Individual Stocks: Investing in individual dividend-paying stocks allows you to select companies with a history of consistent dividend payments and growth.

-

Dividend ETFs: These are baskets of dividend-paying stocks, offering instant diversification and reducing the risk associated with holding individual stocks.

-

Dividend Mutual Funds: Similar to ETFs, dividend mutual funds are managed by professionals who select dividend-paying stocks according to the fund’s investment strategy.

1.4. Benefits of Living Off Dividends

There are several compelling benefits to living off dividends:

- Passive Income: Dividends provide a steady income stream without requiring active participation, freeing up your time for other pursuits.

- Financial Independence: Dividend income can cover your living expenses, allowing you to achieve financial independence and retire early.

- Potential for Growth: Both the dividend income and the underlying value of your investments can grow over time, providing inflation protection and increased wealth.

- Flexibility: You can adjust your dividend income by adding to or reducing your investment holdings.

- Psychological Comfort: Receiving regular dividend payments can provide peace of mind and a sense of financial security, especially during retirement.

1.5. Challenges of Living Off Dividends

While living off dividends offers numerous advantages, it’s essential to be aware of the challenges:

- Capital Requirements: Building a dividend portfolio large enough to generate sufficient income requires a significant amount of capital.

- Market Risk: Stock prices can fluctuate, affecting the value of your portfolio and potentially reducing your dividend income.

- Dividend Cuts: Companies can reduce or suspend dividend payments, especially during economic downturns, impacting your income stream.

- Tax Implications: Dividends are generally taxable, which can reduce the net income you receive.

- Inflation Risk: The purchasing power of dividend income can erode over time if dividend growth doesn’t keep pace with inflation.

2. Calculating How Much Money You Need

Determining how much money you need to live off dividends requires careful planning and consideration of various factors. Let’s break down the steps involved in this calculation.

2.1. Estimate Your Annual Expenses

The first step is to estimate your annual living expenses. This includes housing, food, transportation, healthcare, insurance, taxes, and discretionary spending. It’s helpful to create a detailed budget to track your spending and identify areas where you can potentially reduce costs.

2.2. Determine Your Desired Dividend Income

Next, determine how much dividend income you need to cover your annual expenses. This may be the full amount of your expenses or a portion of it, depending on whether you have other income sources, such as Social Security, pensions, or part-time work.

2.3. Calculate the Required Portfolio Size

To calculate the required portfolio size, you’ll need to estimate the average dividend yield you expect to earn from your investments. Dividend yield is the annual dividend income divided by the stock’s price. A reasonable range for a diversified dividend portfolio is between 3% and 5%.

For example, if you need $50,000 in annual dividend income and expect a 4% dividend yield, you would need a portfolio of $1,250,000 ($50,000 / 0.04).

2.4. Account for Taxes and Inflation

Remember to factor in taxes on dividend income, which can reduce the net income you receive. Also, consider inflation, which can erode the purchasing power of your dividend income over time. You may need to increase your portfolio size or adjust your investment strategy to account for these factors.

2.5. Consider Additional Income Sources

If you have other income sources, such as Social Security, pensions, or part-time work, you can reduce the amount of dividend income you need to generate, thereby reducing the required portfolio size.

2.6. Example Calculation

Here’s an example of how to calculate the required portfolio size:

- Annual Expenses: $60,000

- Other Income Sources: $20,000

- Required Dividend Income: $40,000

- Expected Dividend Yield: 4%

- Required Portfolio Size: $1,000,000 ($40,000 / 0.04)

In this example, you would need a portfolio of $1,000,000 to generate $40,000 in annual dividend income, which, when combined with your other income sources, would cover your annual expenses.

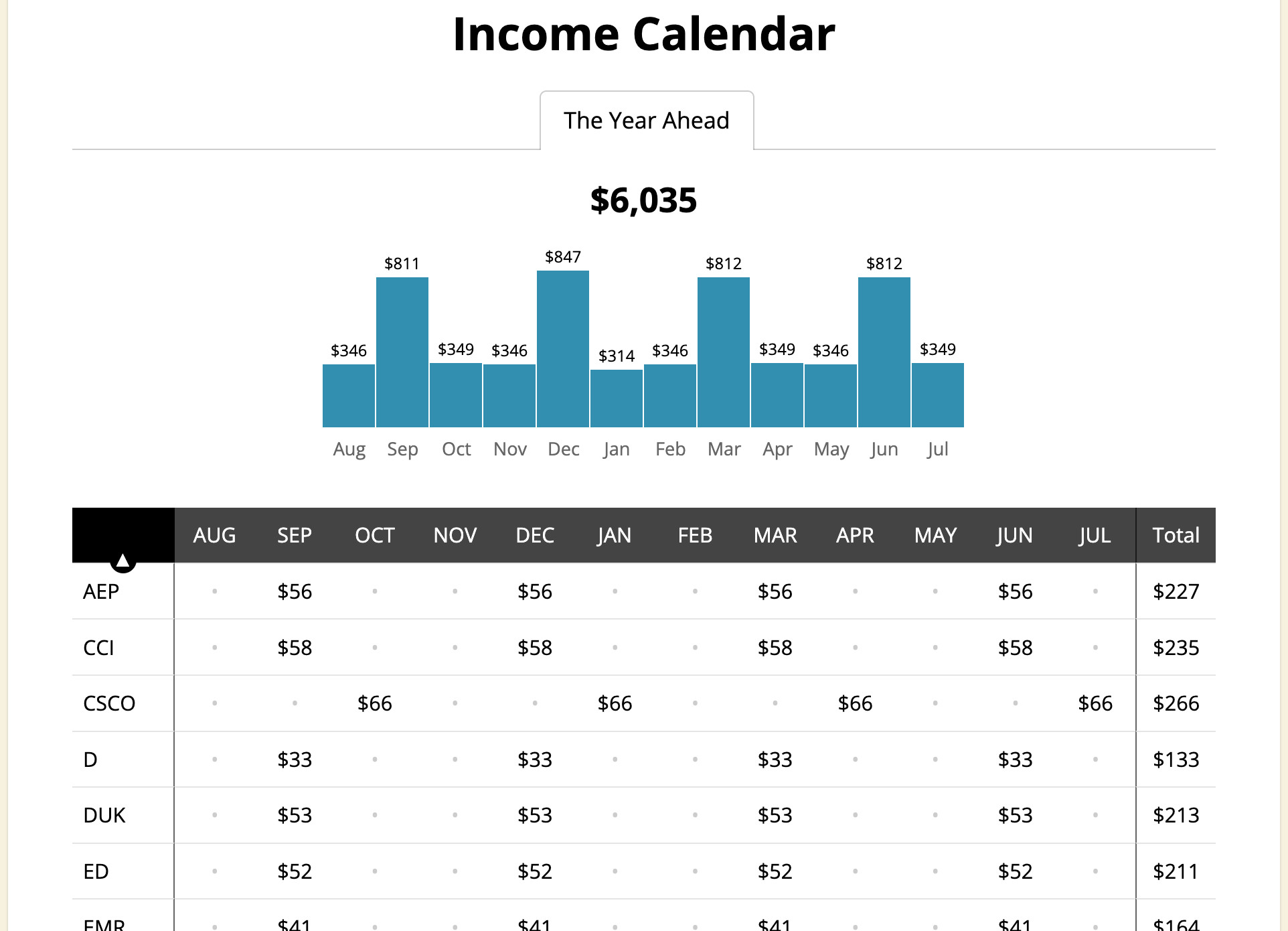

Dividend income calendar showing consistent payouts

Dividend income calendar showing consistent payouts

2.7. Utilizing Financial Tools and Calculators

Money-central.com offers various financial tools and calculators that can help you estimate your expenses, determine your desired dividend income, and calculate the required portfolio size. These resources can simplify the planning process and provide valuable insights into your financial situation.

3. Building a Dividend Portfolio

Once you know how much money you need, the next step is to build a dividend portfolio that can generate the required income. Let’s explore the key considerations in building a dividend portfolio.

3.1. Choose Dividend-Paying Stocks and Funds

Select dividend-paying stocks and funds that align with your investment goals and risk tolerance. Consider factors such as dividend yield, dividend growth rate, payout ratio, and financial health of the company.

3.2. Diversify Your Portfolio

Diversification is crucial to reduce risk. Invest in a variety of stocks and funds across different sectors and industries. This can help mitigate the impact of any single company or sector performing poorly.

3.3. Reinvest Dividends

Consider reinvesting your dividends to accelerate the growth of your portfolio. Reinvesting dividends allows you to purchase more shares, which in turn generate more dividend income, creating a snowball effect.

3.4. Monitor Your Portfolio Regularly

Regularly monitor your portfolio’s performance and make adjustments as needed. Track your dividend income, dividend yields, and the financial health of your holdings. Be prepared to sell underperforming stocks or funds and reallocate your capital to better opportunities.

3.5. Consider Dividend Safety

Focus on companies with a history of consistent dividend payments and a strong financial position. Avoid companies with high dividend yields that may be unsustainable. Look for companies with a low payout ratio, indicating that the company can comfortably afford to pay its dividends.

3.6. Tax-Efficient Investing

Consider tax-efficient investing strategies to minimize the impact of taxes on your dividend income. This may involve investing in tax-advantaged accounts, such as 401(k)s or IRAs, or using tax-loss harvesting to offset capital gains.

3.7. Sector Allocation

Your industry allocation significantly influences your portfolio’s income stability and growth potential. Sectors like utilities and consumer staples often provide steady dividends but may offer limited growth, whereas technology and healthcare might offer higher growth but potentially lower initial dividends. Money-central.com offers tools to analyze sector-specific risks and opportunities, helping you balance income and growth in your portfolio.

3.8. Geographic Diversification

Consider investing in international dividend stocks to diversify your portfolio geographically. This can help reduce your exposure to the economic conditions of any single country.

4. Factors Affecting Dividend Income

Several factors can affect your dividend income, both positively and negatively. It’s essential to be aware of these factors and how they can impact your financial plan.

4.1. Economic Conditions

Economic conditions can significantly impact dividend income. During economic downturns, companies may reduce or suspend dividend payments to conserve cash. Conversely, during economic expansions, companies may increase dividend payments as profits grow.

4.2. Interest Rates

Interest rates can affect dividend yields. When interest rates rise, bond yields become more attractive, potentially putting downward pressure on dividend yields as investors shift their investments from stocks to bonds.

4.3. Company Performance

A company’s financial performance directly impacts its ability to pay dividends. Poor performance can lead to dividend cuts or suspensions, while strong performance can lead to dividend increases.

4.4. Dividend Policy

A company’s dividend policy determines how much of its earnings it distributes to shareholders as dividends. Some companies have a policy of consistently increasing their dividends over time, while others may have a more variable dividend policy.

4.5. Tax Laws

Tax laws can affect the net income you receive from dividends. Changes in tax laws can impact the amount of taxes you pay on dividend income, which can reduce the overall return of your investment.

4.6. Inflation

Inflation can erode the purchasing power of your dividend income over time. If dividend growth doesn’t keep pace with inflation, your income may not be sufficient to cover your expenses.

4.7. Market Volatility

High market volatility can affect the value of your portfolio and potentially impact your dividend income. During periods of market uncertainty, stock prices can fluctuate, which can affect the yield of your portfolio.

5. Strategies for Increasing Dividend Income

If you want to increase your dividend income, there are several strategies you can consider. Let’s explore some of the most effective approaches.

5.1. Invest in Dividend Growth Stocks

Dividend growth stocks are companies that have a history of consistently increasing their dividend payments over time. Investing in these stocks can provide both dividend income and capital appreciation, as the stock price tends to rise as the company’s earnings and dividends grow.

5.2. Reinvest Dividends

Reinvesting dividends allows you to purchase more shares, which in turn generate more dividend income. This creates a compounding effect that can significantly increase your income over time.

5.3. Add New Capital

Adding new capital to your portfolio can increase your dividend income. This may involve saving more money or reallocating assets from other investments.

5.4. Increase Your Allocation to High-Yield Stocks

Consider increasing your allocation to high-yield stocks, which are companies with dividend yields that are higher than the market average. However, be sure to carefully evaluate the financial health and dividend safety of these companies before investing.

5.5. Use Options Strategies

Options strategies, such as covered calls, can generate additional income from your dividend stocks. A covered call involves selling a call option on a stock you already own, which gives the buyer the right to purchase your stock at a specified price before a certain date. In exchange for selling the call option, you receive a premium, which can increase your income.

5.6. Regularly Review and Adjust Your Portfolio

Regularly review your portfolio to identify underperforming stocks or funds and reallocate your capital to better opportunities. This can help improve your overall dividend yield and income.

5.7. Dividend Reinvestment Plans (DRIPs)

DRIPs allow you to automatically reinvest your dividends to purchase additional shares of the company’s stock, often without paying brokerage fees. This can be an efficient way to compound your returns over time. Many companies and brokerages offer DRIP programs, making it easier to participate.

6. Common Mistakes to Avoid

When pursuing a dividend investing strategy, it’s essential to avoid common mistakes that can jeopardize your financial goals. Let’s explore some of the most prevalent pitfalls.

6.1. Chasing High Yields

Chasing high yields can be tempting, but it’s often a risky strategy. Companies with very high dividend yields may be financially unstable or facing challenges that could lead to dividend cuts. Focus on companies with sustainable dividend payouts and a history of consistent dividend payments.

6.2. Ignoring Dividend Safety

Dividend safety is crucial. Invest in companies with a strong financial position and a low payout ratio, indicating that they can comfortably afford to pay their dividends. Avoid companies with a high payout ratio, as they may be more vulnerable to dividend cuts during economic downturns.

6.3. Lack of Diversification

Lack of diversification can increase your risk. Invest in a variety of stocks and funds across different sectors and industries to reduce the impact of any single company or sector performing poorly.

6.4. Neglecting Taxes

Neglecting taxes can reduce your net income. Consider tax-efficient investing strategies, such as investing in tax-advantaged accounts or using tax-loss harvesting to offset capital gains.

6.5. Not Monitoring Your Portfolio

Not monitoring your portfolio can lead to missed opportunities or unrecognized risks. Regularly review your portfolio’s performance and make adjustments as needed.

6.6. Overlooking Inflation

Overlooking inflation can erode the purchasing power of your dividend income over time. Factor inflation into your financial plan and adjust your investment strategy accordingly.

6.7. Ignoring Total Return

Focusing solely on dividend income while ignoring total return (capital appreciation plus dividend income) can be a mistake. A balanced approach that considers both income and growth is essential for long-term financial success.

7. Real-Life Examples and Case Studies

To illustrate the possibilities of living off dividends, let’s explore some real-life examples and case studies.

7.1. The Early Retiree

Consider an individual who retired early at age 55 with a dividend portfolio of $1.5 million. The portfolio generates an average dividend yield of 4%, providing an annual income of $60,000. This income, combined with Social Security benefits, covers the retiree’s living expenses, allowing them to enjoy a comfortable retirement without working.

7.2. The Dividend Growth Investor

Another example is a dividend growth investor who started investing in dividend stocks at age 30. By consistently reinvesting dividends and adding new capital to the portfolio, the investor has built a substantial income stream over time. At age 65, the portfolio generates enough dividend income to cover the investor’s living expenses, providing financial independence and security.

7.3. Case Study: The Impact of Dividend Cuts

A case study of a retiree who relied heavily on dividend income from a single company illustrates the importance of diversification. When the company cut its dividend during an economic downturn, the retiree’s income was significantly reduced, causing financial hardship. This highlights the risk of concentrating your investments in a single company or sector.

7.4. Case Study: The Power of Reinvesting Dividends

A case study of two investors, one who reinvests dividends and one who doesn’t, demonstrates the power of reinvesting dividends. Over a 30-year period, the investor who reinvests dividends accumulates significantly more wealth and income than the investor who doesn’t, illustrating the compounding effect of dividend reinvestment.

7.5. Testimonials from Money-Central.Com Users

“Thanks to the resources and tools on money-central.com, I was able to create a dividend portfolio that now provides me with a steady income stream in retirement. The dividend safety scores and portfolio tracking tools are invaluable.” – John S., New York

“I started investing in dividend stocks a few years ago, and with the help of money-central.com, I’ve been able to build a portfolio that generates a growing income stream. The articles and guides on the site are easy to understand and have helped me make informed investment decisions.” – Mary L., California

8. Getting Started with Money-Central.Com

Money-central.com offers a wealth of resources and tools to help you achieve your financial goals, including living off dividends.

8.1. Articles and Guides

Access a library of articles and guides on dividend investing, portfolio management, and financial planning. Learn about different dividend strategies, how to select dividend stocks, and how to manage your portfolio.

8.2. Financial Tools and Calculators

Use our financial tools and calculators to estimate your expenses, determine your desired dividend income, and calculate the required portfolio size. These tools can simplify the planning process and provide valuable insights into your financial situation.

8.3. Dividend Safety Scores

Utilize our dividend safety scores to assess the financial health and dividend sustainability of different companies. These scores can help you identify companies with a strong track record of consistent dividend payments.

8.4. Portfolio Tracking Tools

Track your portfolio’s performance and dividend income with our portfolio tracking tools. Monitor your dividend yields, dividend growth rates, and the financial health of your holdings.

8.5. Expert Advice

Get expert advice from our team of financial professionals. We can help you develop a personalized dividend investing strategy that aligns with your goals and risk tolerance.

8.6. Community Forum

Connect with other dividend investors in our community forum. Share ideas, ask questions, and learn from the experiences of others.

8.7. Personalized Financial Checklists

Money-central.com provides personalized financial checklists that guide you through each step of building and managing your dividend portfolio. These checklists ensure you don’t miss critical steps in your financial planning.

9. The Future of Dividend Investing

Dividend investing remains a viable strategy for generating income and building wealth. As the population ages and more people seek financial independence, dividend investing is likely to become even more popular.

9.1. Trends in Dividend Investing

Several trends are shaping the future of dividend investing:

-

Increased Focus on Dividend Safety: Investors are becoming more focused on dividend safety, seeking companies with a strong financial position and a history of consistent dividend payments.

-

Growing Popularity of Dividend ETFs: Dividend ETFs are becoming increasingly popular, offering instant diversification and reducing the risk associated with holding individual stocks.

-

Greater Use of Technology: Technology is playing a greater role in dividend investing, with investors using online tools and platforms to research stocks, track portfolios, and manage their finances.

9.2. Predictions for the Future

- Dividend yields may remain relatively low in the near term due to low interest rates and a strong stock market.

- Dividend growth is likely to be strong as companies continue to generate profits and increase their dividend payments.

- Dividend investing will continue to be a popular strategy for generating income and building wealth, especially among retirees and those seeking financial independence.

9.3. Adapting to Changing Market Conditions

To succeed in dividend investing, investors must adapt to changing market conditions. This may involve adjusting your portfolio allocation, rebalancing your holdings, and staying informed about economic trends and company performance. Money-central.com is committed to providing you with the resources and tools you need to navigate the ever-changing world of finance.

10. Frequently Asked Questions (FAQs)

10.1. How Much Money Do I Need to Start Investing in Dividends?

You can start investing in dividends with as little as a few hundred dollars. You can buy shares of individual dividend-paying stocks or invest in dividend ETFs or mutual funds.

10.2. What Is a Good Dividend Yield?

A good dividend yield depends on market conditions and your investment goals. Generally, a dividend yield between 3% and 5% is considered attractive.

10.3. Are Dividends Taxable?

Yes, dividends are generally taxable. The tax rate depends on your income and the type of dividend. Qualified dividends are taxed at a lower rate than ordinary income.

10.4. What Is a Payout Ratio?

The payout ratio is the percentage of a company’s earnings that it pays out as dividends. A low payout ratio indicates that the company can comfortably afford to pay its dividends, while a high payout ratio may be unsustainable.

10.5. How Often Are Dividends Paid?

Most companies pay dividends quarterly, but some pay monthly or annually.

10.6. What Is a Dividend Reinvestment Plan (DRIP)?

A dividend reinvestment plan (DRIP) allows you to automatically reinvest your dividends to purchase additional shares of the company’s stock.

10.7. How Can I Find Dividend-Paying Stocks?

You can find dividend-paying stocks by using online stock screeners or by consulting with a financial advisor.

10.8. What Are the Risks of Dividend Investing?

The risks of dividend investing include market risk, dividend cuts, and tax implications.

10.9. How Can I Reduce the Risks of Dividend Investing?

You can reduce the risks of dividend investing by diversifying your portfolio, investing in companies with a strong financial position, and monitoring your portfolio regularly.

10.10. Is Dividend Investing Right for Me?

Dividend investing may be right for you if you are seeking a steady income stream, financial independence, and long-term capital appreciation.

Living off dividends is an achievable goal with careful planning, disciplined investing, and a commitment to monitoring your portfolio. With the resources and tools available at money-central.com, you can take control of your financial future and achieve your dreams of financial independence.

Ready to take control of your financial future? Explore our articles, use our tools, and seek expert advice at money-central.com. Start building your dividend portfolio today and pave the way for a secure and prosperous tomorrow. Visit us at 44 West Fourth Street, New York, NY 10012, United States, or call +1 (212) 998-0000. Your journey to financial freedom starts here.