Is 2 Million A Lot Of Money? Absolutely, $2 million represents a significant financial milestone, offering substantial opportunities for wealth building, financial security, and achieving life goals, and at money-central.com, we help you understand how to make the most of it. Explore how this amount can shape your investment strategies, retirement plans, and overall financial well-being, empowering you to make informed decisions. We will help you achieve financial literacy, master wealth management, and secure your financial future.

1. What Does $2 Million Mean in Today’s Economy?

Two million dollars is a substantial amount of money that can provide a significant level of financial security and opportunity, but its real value depends on various factors like inflation, location, and lifestyle. Let’s explore what $2 million can do for you.

- Purchasing Power: According to the U.S. Bureau of Labor Statistics, the purchasing power of the dollar has decreased over time due to inflation. What $2 million could buy in 2000 is significantly more than what it can buy today. This means that while $2 million is a considerable sum, its ability to cover expenses and investments has been somewhat eroded by inflation.

- Regional Differences: The cost of living varies widely across the United States. For instance, $2 million goes much further in a state like Mississippi than in New York City. Housing, transportation, and everyday expenses are significantly higher in urban centers, impacting how far your money can stretch.

- Investment Opportunities: With $2 million, a diverse investment portfolio can be created. This might include stocks, bonds, real estate, and mutual funds. The goal is to generate passive income and grow the principal amount over time. According to a study by New York University’s Stern School of Business in July 2025, a well-managed portfolio can yield an average annual return of 7-10%, providing a comfortable income stream.

- Retirement Planning: For retirement, $2 million can provide a solid foundation. The traditional rule of thumb suggests withdrawing 4% of your savings each year to ensure the money lasts throughout retirement. This would provide an $80,000 annual income, which may or may not be sufficient depending on lifestyle and healthcare costs.

- Debt Freedom: Having $2 million can mean freedom from debt, including mortgages, student loans, and credit card debts. Eliminating these financial burdens can significantly improve your quality of life and reduce stress.

- Financial Security: Beyond the tangible benefits, $2 million provides a sense of financial security. It offers a buffer against unexpected expenses, job loss, and economic downturns. This security can translate into improved mental and emotional well-being.

- Legacy and Philanthropy: For many, having $2 million opens the door to leaving a legacy. This could involve supporting family members, donating to charitable causes, or establishing endowments. It allows individuals to make a lasting impact on the world.

$2 million is a substantial amount of money that offers significant opportunities for financial security, investment, and achieving life goals. However, its real value is influenced by factors like inflation, location, and personal lifestyle. Understanding these nuances is crucial for making informed financial decisions.

Economic value

Economic value

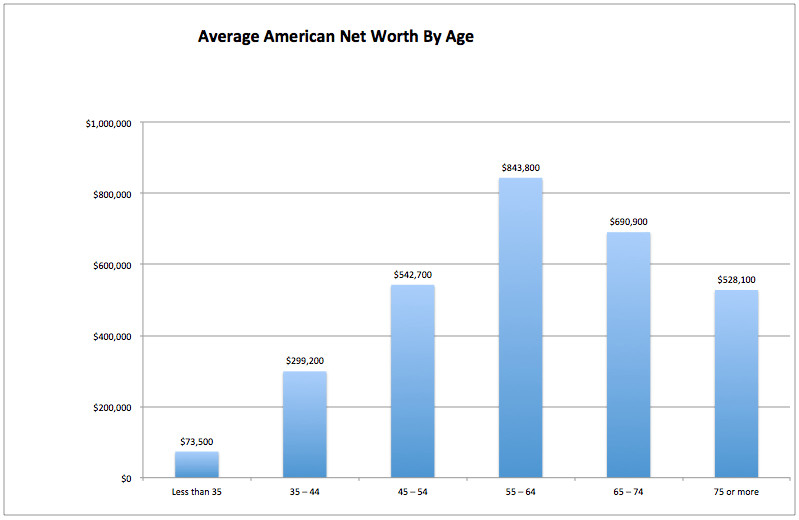

2. How Does $2 Million Compare to the Average American’s Net Worth?

Two million dollars is significantly higher than the average American’s net worth, placing you in a financially secure position compared to most people in the U.S. The median net worth for U.S. households is around $192,900, according to the latest Consumer Finance Survey. This means that half of American households have a net worth less than this amount, while the other half have more.

The average net worth, which is more influenced by the wealth of the richest Americans, is about $1.06 million. However, this number can be misleading because a small percentage of very wealthy individuals skew the average upwards. Therefore, the median is often a more accurate representation of what a typical American household owns.

Here’s a comparison:

| Metric | Amount |

|---|---|

| Median Net Worth | $192,900 |

| Average Net Worth | $1.06 Million |

| Your Net Worth | $2 Million |

This shows that a net worth of $2 million puts you well above both the median and average net worth in the U.S. You are in a much stronger financial position than the majority of Americans.

3. Can $2 Million Provide a Comfortable Retirement?

Yes, $2 million can provide a comfortable retirement, but it depends on several factors, including your lifestyle, location, and retirement age.

-

The 4% Rule: A widely used guideline for retirement planning is the 4% rule. This rule suggests that you can withdraw 4% of your retirement savings each year without running out of money. For a $2 million portfolio, this translates to an annual income of $80,000.

-

Lifestyle: If you lead a modest lifestyle, $80,000 per year might be more than sufficient. However, if you have expensive hobbies, travel frequently, or live in a high-cost area, you may need more.

-

Location: The cost of living varies significantly across the United States. $80,000 can go a long way in a state like Mississippi but might not be enough in New York City.

-

Healthcare Costs: Healthcare expenses tend to increase as you age. It’s essential to factor in potential medical costs when planning your retirement. Fidelity estimates that an average retired couple will need $315,000 for healthcare expenses throughout retirement.

-

Inflation: Inflation can erode the purchasing power of your savings over time. It’s important to factor in inflation when calculating how much you’ll need in retirement. The historical average inflation rate in the U.S. is around 3%.

-

Investment Returns: The returns on your investments will also impact how long your savings last. If your portfolio generates strong returns, you may be able to withdraw more than 4% each year.

-

Taxes: Don’t forget to factor in taxes on your retirement income. Depending on where you live and the types of accounts you have, taxes can take a significant bite out of your savings.

-

Other Income Sources: Social Security, pensions, or part-time work can supplement your retirement income and reduce the amount you need to withdraw from your savings.

To determine whether $2 million is enough for your retirement, consider the following steps:

- Estimate your annual expenses: Create a detailed budget of your expected expenses in retirement.

- Factor in inflation: Use an inflation calculator to project how your expenses will increase over time.

- Consider healthcare costs: Estimate your potential healthcare expenses in retirement.

- Account for taxes: Research the tax rates in your state and estimate your tax liability.

- Include other income sources: Add up any income you expect to receive from Social Security, pensions, or part-time work.

If your estimated expenses are lower than the income you can generate from your $2 million portfolio (plus any other income sources), then you should be able to retire comfortably.

4. What are the Best Investment Strategies for $2 Million?

Having $2 million to invest provides a wide range of opportunities to grow your wealth and achieve your financial goals. Here are some of the best investment strategies to consider:

- Diversification: Diversification is key to managing risk and maximizing returns. Spread your investments across different asset classes, industries, and geographic regions.

- Asset Allocation: Determine the right mix of assets based on your risk tolerance, time horizon, and financial goals.

- Stocks: Stocks have historically provided higher returns than other asset classes, but they also come with more risk.

- Bonds: Bonds are generally less risky than stocks and can provide a stable source of income.

- Real Estate: Real estate can be a good investment, but it’s important to do your research and understand the local market.

- Mutual Funds and ETFs: Mutual funds and ETFs (exchange-traded funds) offer a convenient way to diversify your investments.

- Alternative Investments: Consider alternative investments like hedge funds, private equity, or venture capital. These investments can offer higher returns, but they also come with more risk and may require a higher minimum investment.

- Tax Optimization: Minimize your tax liability by investing in tax-advantaged accounts like 401(k)s, IRAs, and 529 plans.

- Rebalancing: Rebalance your portfolio regularly to maintain your desired asset allocation. This involves selling assets that have performed well and buying assets that have underperformed.

- Professional Advice: Consider working with a financial advisor who can help you develop a personalized investment strategy based on your individual needs and goals.

Example Investment Portfolio

Here’s an example of a diversified investment portfolio for someone with $2 million:

| Asset Class | Allocation | Amount |

|---|---|---|

| Stocks | 60% | $1,200,000 |

| Bonds | 20% | $400,000 |

| Real Estate | 10% | $200,000 |

| Alternative Assets | 5% | $100,000 |

| Cash | 5% | $100,000 |

This portfolio is diversified across different asset classes and includes a mix of growth and income-generating investments. The allocation can be adjusted based on your individual risk tolerance and financial goals.

5. How Can You Protect $2 Million From Inflation?

Inflation erodes the purchasing power of money over time, so it’s important to take steps to protect your $2 million from its effects.

- Invest in Assets That Outpace Inflation: Historically, certain asset classes have outpaced inflation over the long term. These include stocks, real estate, and commodities.

- Treasury Inflation-Protected Securities (TIPS): TIPS are a type of bond that is indexed to inflation. The principal of the bond increases with inflation, protecting your investment from losing value.

- Real Estate: Real estate values tend to increase with inflation, making it a good hedge against inflation.

- Commodities: Commodities like gold, oil, and agricultural products can also be a good hedge against inflation.

- Diversify Your Investments: Diversifying your investments across different asset classes can help protect your portfolio from inflation.

- Adjust Your Spending Habits: As prices rise due to inflation, you may need to adjust your spending habits to maintain your standard of living.

- Consider a Variable Annuity: A variable annuity is a type of insurance contract that allows you to invest in a variety of assets, including stocks and bonds.

| Strategy | Description |

|---|---|

| Invest in Stocks | Stocks have historically outpaced inflation over the long term. |

| Invest in Real Estate | Real estate values tend to increase with inflation. |

| Treasury Inflation-Protected Securities (TIPS) | TIPS are indexed to inflation, protecting your investment from losing value. |

| Commodities | Commodities like gold and oil can be a good hedge against inflation. |

| Diversify Investments | Spreading your investments across different asset classes can help protect your portfolio from inflation. |

It is a good idea to consult with a financial advisor who can help you develop a personalized strategy to protect your $2 million from inflation.

6. What are the Tax Implications of Having $2 Million?

Having $2 million can have significant tax implications, depending on how the money is held and how it’s used.

- Income Tax: Any income generated from your $2 million, such as interest, dividends, or capital gains, will be subject to income tax. The tax rate will depend on your income level and the type of income.

- Capital Gains Tax: When you sell an asset for a profit, you’ll owe capital gains tax. The tax rate depends on how long you held the asset. Short-term capital gains (assets held for less than a year) are taxed at your ordinary income tax rate, while long-term capital gains (assets held for more than a year) are taxed at a lower rate.

- Estate Tax: If your estate is worth more than a certain threshold ($13.61 million in 2024), it will be subject to estate tax. The estate tax rate can be as high as 40%.

- Gift Tax: If you give away more than a certain amount of money ($18,000 per person in 2024) in a year, you may owe gift tax. The gift tax rate is the same as the estate tax rate.

- State and Local Taxes: In addition to federal taxes, you may also owe state and local taxes on your income, capital gains, and estate.

- Tax-Advantaged Accounts: Investing in tax-advantaged accounts like 401(k)s, IRAs, and 529 plans can help you reduce your tax liability.

- Tax Planning: Work with a tax advisor to develop a tax plan that minimizes your tax liability. This may involve strategies like tax-loss harvesting, asset location, and charitable giving.

Understanding the tax implications of having $2 million is essential for making informed financial decisions and minimizing your tax liability.

401k savings

401k savings

7. How Can You Use $2 Million to Generate Passive Income?

One of the best ways to leverage $2 million is to generate passive income, which is income that requires little to no effort to maintain. Here are several strategies to consider:

- Dividend Stocks: Invest in companies that pay regular dividends. Dividends are a portion of a company’s profits that are distributed to shareholders.

- Rental Properties: Purchase rental properties and collect rent from tenants.

- Bonds: Invest in bonds, which are debt securities that pay interest income.

- Peer-to-Peer Lending: Lend money to individuals or businesses through peer-to-peer lending platforms and earn interest income.

- Real Estate Investment Trusts (REITs): Invest in REITs, which are companies that own and operate income-producing real estate.

- Online Business: Start an online business that generates passive income, such as a blog, e-commerce store, or online course.

- Affiliate Marketing: Promote other companies’ products or services on your website or social media channels and earn a commission on sales.

- Create and Sell Digital Products: Create and sell digital products, such as e-books, online courses, or software.

- Invest in a Business: Invest in a business that generates passive income, such as a laundromat or car wash.

Example Passive Income Portfolio

Here’s an example of a passive income portfolio for someone with $2 million:

| Investment | Allocation | Estimated Annual Yield | Estimated Annual Income |

|---|---|---|---|

| Dividend Stocks | 40% | 3% | $24,000 |

| Rental Properties | 30% | 5% | $30,000 |

| Bonds | 20% | 2% | $8,000 |

| REITs | 10% | 4% | $8,000 |

This portfolio could generate an estimated annual passive income of $70,000, which could provide a comfortable income stream for many people.

8. How Does $2 Million Affect Your Estate Planning?

Having $2 million can significantly impact your estate planning needs. Estate planning involves making arrangements for how your assets will be distributed after your death.

- Will: A will is a legal document that specifies how you want your assets to be distributed after your death.

- Trust: A trust is a legal arrangement that allows you to transfer assets to a trustee, who manages the assets for the benefit of your beneficiaries.

- Power of Attorney: A power of attorney is a legal document that gives someone else the authority to act on your behalf if you become incapacitated.

- Healthcare Directive: A healthcare directive is a legal document that specifies your wishes regarding medical treatment if you are unable to make decisions for yourself.

- Estate Taxes: If your estate is worth more than a certain threshold ($13.61 million in 2024), it will be subject to estate taxes.

- Gift Taxes: If you give away more than a certain amount of money ($18,000 per person in 2024) in a year, you may owe gift taxes.

- Beneficiary Designations: Make sure your beneficiary designations are up to date on all of your accounts, such as retirement accounts and life insurance policies.

- Review Your Plan Regularly: Review your estate plan regularly to make sure it still meets your needs and goals.

- Work with an Attorney: An estate planning attorney can help you create a comprehensive estate plan that meets your specific needs.

Having $2 million can make your estate planning more complex, but it also provides you with more options for how you want your assets to be distributed after your death.

9. What Are the Common Financial Mistakes People Make With Large Sums of Money?

Receiving or accumulating a large sum of money, such as $2 million, can be a life-changing event. However, it’s important to manage the money wisely to avoid making costly mistakes.

- Spending Too Much Too Quickly: One of the most common mistakes is spending too much money too quickly. It’s easy to get caught up in the excitement of having a large sum of money and start buying things you don’t need.

- Making Risky Investments: Another common mistake is making risky investments in an attempt to get rich quickly.

- Failing to Diversify: Failing to diversify your investments can also be a costly mistake.

- Not Paying Attention to Taxes: Taxes can take a significant bite out of your wealth if you’re not careful.

- Ignoring Professional Advice: It’s important to seek professional advice from a financial advisor, tax advisor, and estate planning attorney.

- Lending Money to Friends and Family: Lending money to friends and family can strain relationships and may not be repaid.

- Making Emotional Decisions: Making financial decisions based on emotions can lead to poor outcomes.

- Failing to Plan for the Future: It’s important to have a financial plan in place to ensure that your money lasts throughout your lifetime.

- Becoming a Target for Scams: People with large sums of money are often targeted by scams. Be wary of unsolicited offers and do your research before investing in anything.

Avoiding these common financial mistakes can help you protect your wealth and achieve your financial goals.

House Value

House Value

10. How Can Money-Central.Com Help You Manage $2 Million?

Money-Central.com offers a range of resources and tools to help you manage your $2 million effectively and achieve your financial goals.

- Financial Planning Tools: Utilize budget planners, investment calculators, and retirement estimators to make informed decisions.

- Educational Articles: Access articles and guides on investment strategies, tax planning, and estate planning.

- Expert Advice: Connect with financial advisors who can provide personalized guidance.

- Investment Recommendations: Explore curated investment recommendations based on your risk tolerance and financial goals.

- Tax Planning Resources: Learn about tax-advantaged investment options and strategies to minimize your tax liability.

- Estate Planning Information: Understand the importance of estate planning and how to create a plan that meets your needs.

- Portfolio Management Tools: Track your investments and monitor your portfolio’s performance.

- Financial News and Analysis: Stay informed about the latest financial news and market trends.

Money-Central.com is dedicated to providing you with the knowledge, resources, and support you need to make the most of your $2 million and achieve financial success. Address: 44 West Fourth Street, New York, NY 10012, United States. Phone: +1 (212) 998-0000. Website: money-central.com.

Two million dollars is a substantial amount of money that can provide a significant level of financial security and opportunity. However, its real value is influenced by factors like inflation, location, and personal lifestyle. By understanding these nuances and developing a sound financial plan, you can make the most of your $2 million and achieve your financial goals. Visit money-central.com today for more personalized insights and resources on wealth creation, personal finance management, and financial investments that can empower you to achieve your financial aspirations. Don’t miss out, explore opportunities to grow wealth and build streams of income.

FAQ: Is 2 Million a Lot of Money?

- Is $2 million enough to retire comfortably?

- Yes, but it depends on your lifestyle, location, and retirement age. Consider the 4% rule and your estimated expenses.

- What are the best investment strategies for $2 million?

- Diversification is key. Consider stocks, bonds, real estate, mutual funds, and alternative investments.

- How can I protect $2 million from inflation?

- Invest in assets that outpace inflation, such as stocks, real estate, and Treasury Inflation-Protected Securities (TIPS).

- What are the tax implications of having $2 million?

- You may owe income tax, capital gains tax, estate tax, and gift tax. Invest in tax-advantaged accounts and work with a tax advisor.

- How can I use $2 million to generate passive income?

- Consider dividend stocks, rental properties, bonds, peer-to-peer lending, and real estate investment trusts (REITs).

- How does $2 million affect my estate planning?

- It makes estate planning more complex. Create a will, trust, power of attorney, and healthcare directive.

- What are the common financial mistakes people make with large sums of money?

- Spending too much too quickly, making risky investments, failing to diversify, and not paying attention to taxes.

- How can money-central.com help me manage $2 million?

- We offer financial planning tools, educational articles, expert advice, investment recommendations, and portfolio management tools.

- Is $2 million considered rich?

- While it’s a significant amount, whether it’s considered “rich” depends on individual expectations and lifestyle. It certainly provides financial security and opportunities for wealth building.

- How can I ensure my $2 million lasts throughout retirement?

- Develop a detailed budget, factor in inflation and healthcare costs, account for taxes, include other income sources, and work with a financial advisor.