Who Did Lee Radziwill Leave Her Money To? Lee Radziwill’s estate planning reveals a complex web of financial decisions, and at money-central.com we break down who the beneficiaries were. Understanding her asset distribution is crucial for grasping estate planning nuances, and it can help you learn how to manage your assets.

1. Who Was Lee Radziwill?

Lee Radziwill, born Caroline Lee Bouvier, was a prominent American socialite, actress, and interior designer, and the younger sister of First Lady Jacqueline Kennedy Onassis. Her life was one of high society, marked by marriages to notable figures, including a Polish prince and a Hollywood director.

-

Birth and Family Background: Born on March 3, 1933, in New York City, Lee was the daughter of John Vernou Bouvier III and Janet Norton Lee.

-

Marriages: She was married three times:

- Michael Temple Canfield (m. 1953, div. 1959)

- Prince Stanisław Albrecht Radziwiłł (m. 1959, div. 1974)

- Herbert Ross (m. 1988, div. 2001)

-

Career: Radziwill pursued various careers, including acting and interior design, but was best known for her socialite status and fashion influence.

-

Death: Lee Radziwill passed away on February 15, 2019, in New York City at the age of 85.

2. What Was Lee Radziwill’s Estimated Net Worth?

At the time of her death, Lee Radziwill’s estimated net worth was approximately $50 million. This wealth was accumulated through various sources, including inheritances, settlements, and her own business ventures.

- Inheritances: Radziwill benefited from family wealth, including a trust established by her mother, Janet Lee Auchincloss.

- Settlements: She received settlements from her divorces, particularly from her marriage to Herbert Ross, a successful film director.

- Real Estate: Radziwill owned valuable real estate, including a co-op apartment in Manhattan and a pied-à-terre in Paris.

- Personal Belongings: Her estate included valuable personal belongings such as jewelry, art, and designer clothing.

3. Who Was the Primary Beneficiary of Lee Radziwill’s Estate?

The primary beneficiary of Lee Radziwill’s estate was her lone surviving child, Anna Christina “Tina” Radziwill. According to her Last Will and Testament, Tina inherited the majority of her mother’s estimated $50 million estate.

- Anna Christina “Tina” Radziwill: Tina, born in 1960, has maintained a relatively private life compared to her mother and aunt. Her occupation is listed as a producer, and she was briefly married to Ottavio Arancio, a professor of medicine at Columbia University.

- Trusts: Tina also became the beneficiary of trusts established by her grandmother, Janet Lee Auchincloss, and managed by Lee Radziwill.

4. Who Was Excluded From Lee Radziwill’s Will?

Despite close relationships with certain individuals, Lee Radziwill’s will specifically excluded several family members and close associates:

- Carole Radziwill: Lee’s daughter-in-law, Carole Radziwill, the former star of “The Real Housewives of New York City,” was not mentioned in the will.

- Caroline Kennedy Schlossberg: Lee’s niece, Caroline Kennedy Schlossberg, the daughter of Jacqueline Kennedy Onassis, was also excluded.

- Caroline Kennedy’s Children: Rose, Tatiana, and John Schlossberg, Caroline Kennedy’s children, were not included in the will.

Lee Radziwill died age 85 at her home in New York City. Her daughter Tina followed her mother

Lee Radziwill died age 85 at her home in New York City. Her daughter Tina followed her mother

5. Why Was Carole Radziwill Excluded From the Will?

The exclusion of Carole Radziwill from Lee Radziwill’s will raised questions, given their close relationship, especially after the death of Anthony Radziwill. There are several potential reasons for this decision:

- Estate Planning Preferences: Lee may have had specific intentions regarding the distribution of her assets, prioritizing her direct descendants.

- Financial Independence: Carole Radziwill has her own career and financial resources, which may have influenced Lee’s decision.

- Personal Relationships: While they were close, their relationship reportedly had its ups and downs, which might have played a role.

- Will Specificity: Wills are legal documents that reflect the testator’s wishes at a specific time, and these wishes can change over time.

6. What Was Jackie Kennedy’s Influence on Lee Radziwill’s Estate?

Jacqueline Kennedy Onassis, Lee’s older sister, played a significant role in Lee’s financial life, although she did not directly include Lee in her own will.

- Financial Support: Jackie provided financial support to Lee throughout her life, helping her maintain her lavish lifestyle.

- Trusts: Jackie was involved in the creation of trusts for Lee’s benefit, ensuring her financial security.

- Jackie’s Will: In her own will, Jackie stated that she had already provided for Lee during her lifetime, which is why she did not leave her any specific inheritance.

- Shared History: The sisters had a complex relationship, marked by both rivalry and deep affection, which influenced their financial decisions.

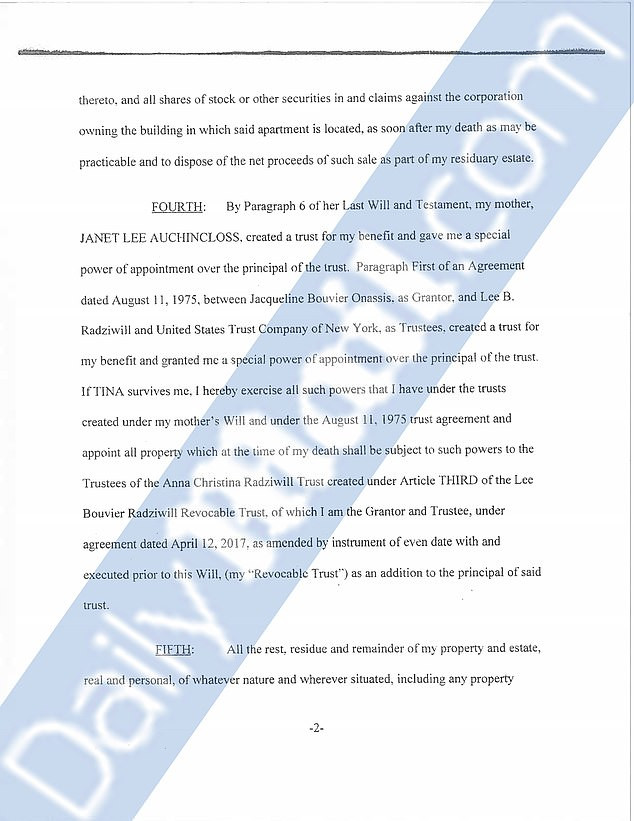

7. How Was Lee Radziwill’s Co-op Apartment Handled in the Will?

Lee Radziwill’s will directed her executors to sell her co-op apartment located at 160 East 72nd Street in Manhattan. The proceeds from the sale were to be included as part of her residuary estate.

- Property Details: The apartment was Lee’s primary residence at the time of her death, although she previously split her time between New York and Paris.

- Downsizing: In 2017, Lee had put the apartment on the market for $4 million, indicating a desire to downsize.

- Executor Responsibilities: The executors were responsible for selling the apartment as soon as practicable after her death and managing the funds appropriately.

8. Who Were the Executors of Lee Radziwill’s Estate?

Instead of appointing a family member, Lee Radziwill chose two close friends to serve as co-executors of her estate:

- Hamilton South: A public relations professional and close friend of Lee’s niece, Carolyn Bessette Kennedy.

- Martin B. O’Connor II: A managing partner at the law firm of O’Connor, Morss & O’Connor.

Hamilton South

Hamilton South

Why These Executors?

- Trust and Integrity: Lee expressed great confidence in their integrity and abilities.

- Financial Acumen: O’Connor’s financial expertise was a key factor in her decision.

- Prior Relationship: O’Connor had served as Lee’s attorney in the past, establishing a long-standing relationship.

- Dual Role: Both South and O’Connor were also named successor co-trustees under the revocable trust agreement.

9. What Were the Executor’s Fees for Managing Lee Radziwill’s Estate?

The executors of Lee Radziwill’s estate were entitled to receive commissions based on the value of the probate estate. According to New York State statutory rates, these commissions could range from two to four percent.

- Commission Calculation: For example, if the probate estate was valued at $1,000,000, the executors would be entitled to receive commissions of $34,000.

- Legal Guidelines: The exact commission amount would depend on the final valuation of Lee’s estate and the applicable state laws.

10. How Did Lee Radziwill Address Funeral Expenses in Her Will?

Lee Radziwill’s will specifically addressed funeral expenses, ensuring they would be paid promptly.

- Priority Payment: The will directed that all debts and funeral expenses be paid as soon as practicable after her death.

- Tax Avoidance: Lee instructed that no extraordinary means or special accounting loopholes be used to avoid paying any death taxes.

- Cremation: After the funeral service, Lee’s remains were cremated, and her ashes were presented to her daughter, Tina.

11. How Estate Planning Can Benefit You?

Estate planning is a critical process that ensures your assets are distributed according to your wishes after your death. Whether you’re managing millions or starting with modest savings, understanding the basics can save your loved ones stress and potential legal battles.

- Clear Distribution of Assets: A well-structured estate plan clearly outlines who receives what, minimizing confusion and disputes among family members. This is particularly important for those with significant assets or complex family dynamics.

- Tax Efficiency: Estate planning can help minimize estate taxes, ensuring that a larger portion of your wealth is passed on to your beneficiaries rather than being absorbed by taxes.

- Guardianship for Minor Children: If you have minor children, estate planning allows you to designate guardians who will care for them in the event of your passing, providing security and stability for their future.

- Protection of Assets: Estate plans can include trusts that protect assets from creditors, lawsuits, or mismanagement, ensuring that your beneficiaries receive the intended benefits.

- Healthcare Directives: Estate planning isn’t just about money; it also includes healthcare directives that specify your wishes regarding medical treatment in case you become incapacitated, giving you control over your healthcare decisions.

- Business Succession: For business owners, estate planning ensures a smooth transition of ownership and management, preserving the business for future generations or facilitating a sale under favorable terms.

- Charitable Giving: If you’re passionate about certain causes, estate planning allows you to incorporate charitable giving into your legacy, supporting organizations that matter to you.

- Avoiding Probate: A well-designed estate plan can help your estate avoid or minimize probate, a potentially lengthy and costly legal process.

12. Common Estate Planning Mistakes to Avoid

Many people delay or avoid estate planning, often due to discomfort or a lack of understanding. However, neglecting this important aspect of financial management can lead to significant issues for your loved ones. Here are some common estate planning mistakes to avoid:

- Procrastination: Delaying estate planning is perhaps the most common mistake. Life is unpredictable, and waiting until you’re “ready” can mean it never gets done.

- DIY Wills: While online templates may seem convenient, they often lack the personalization needed to address your specific circumstances. A poorly drafted will can lead to legal challenges and unintended consequences.

- Failing to Update: Life changes—marriage, divorce, births, deaths, and significant changes in assets—require updates to your estate plan. Review your plan regularly to ensure it still reflects your wishes.

- Not Funding Trusts: Creating a trust is only half the battle. You must also transfer assets into the trust to ensure it functions as intended.

- Ignoring Digital Assets: In today’s digital age, it’s important to include digital assets like online accounts, social media profiles, and digital wallets in your estate plan.

- Lack of Communication: Failing to inform your family or executors about your estate plan can lead to confusion and conflict. Open communication ensures everyone understands their roles and responsibilities.

- Neglecting Healthcare Directives: A will only covers asset distribution. Healthcare directives, such as a living will and power of attorney for healthcare, are essential for guiding medical decisions if you become incapacitated.

- Not Seeking Professional Advice: Estate planning is complex. Consulting with an estate planning attorney, financial advisor, and tax professional can ensure your plan is comprehensive and tailored to your needs.

- Underestimating Estate Taxes: Estate taxes can significantly reduce the value of your estate. Proper planning can help minimize these taxes and maximize the inheritance for your beneficiaries.

- Assuming Joint Ownership Avoids Probate: While joint ownership does transfer assets outside of probate, it can also lead to unintended consequences, such as loss of control and potential tax issues.

13. Key Components of an Estate Plan

A comprehensive estate plan consists of several key documents and strategies, each serving a specific purpose. Understanding these components can help you create a plan that meets your unique needs and goals.

- Will: A will is a legal document that outlines how your assets should be distributed after your death. It also allows you to name an executor who will manage your estate and guardians for minor children.

- Trust: A trust is a legal arrangement in which you (the grantor) transfer assets to a trustee, who manages them for the benefit of your beneficiaries. Trusts can be used to avoid probate, protect assets, and provide for loved ones with special needs.

- Power of Attorney: A power of attorney is a legal document that authorizes someone (your agent) to act on your behalf in financial and legal matters if you become incapacitated.

- Healthcare Proxy: A healthcare proxy (also known as a medical power of attorney) allows you to appoint someone to make healthcare decisions for you if you are unable to do so.

- Living Will: A living will (also known as an advance directive) outlines your wishes regarding medical treatment in end-of-life situations, such as whether you want to receive life-sustaining treatment.

- Beneficiary Designations: Beneficiary designations specify who should receive assets held in retirement accounts, life insurance policies, and other financial accounts.

- Letter of Intent: A letter of intent is a non-binding document that provides additional guidance to your executor or trustee, such as your wishes regarding funeral arrangements or specific personal items.

- Inventory of Assets: An inventory of assets is a detailed list of all your assets, including real estate, bank accounts, investments, and personal property. This list helps your executor or trustee manage your estate efficiently.

- Digital Estate Plan: A digital estate plan outlines how your digital assets should be managed after your death, including access to online accounts, social media profiles, and digital wallets.

- Tax Planning: Tax planning involves strategies to minimize estate taxes, gift taxes, and income taxes, ensuring that more of your wealth is preserved for your beneficiaries.

14. Estate Planning for Different Life Stages

Estate planning is not a one-time event; it’s an ongoing process that should be adjusted as you move through different life stages. Each stage brings unique challenges and opportunities that require careful consideration.

-

Young Adulthood (18-30):

- Focus: Basic planning, such as designating beneficiaries for life insurance and retirement accounts.

- Key Documents: Beneficiary designations, power of attorney, healthcare proxy.

- Considerations: Designating guardians for minor children (if applicable), creating a simple will.

-

Early Family Years (30-45):

- Focus: Protecting your family and assets, especially if you have young children.

- Key Documents: Will, trust, power of attorney, healthcare proxy, life insurance.

- Considerations: Establishing a trust to provide for children, updating beneficiary designations, reviewing life insurance needs.

-

Mid-Career (45-60):

- Focus: Maximizing wealth transfer, minimizing taxes, planning for retirement.

- Key Documents: Will, trust, power of attorney, healthcare proxy, advanced tax planning strategies.

- Considerations: Creating a charitable giving plan, exploring estate tax reduction strategies, reviewing retirement plans.

-

Retirement (60+):

- Focus: Ensuring financial security, managing healthcare costs, passing on your legacy.

- Key Documents: Will, trust, power of attorney, healthcare proxy, long-term care insurance.

- Considerations: Planning for long-term care needs, updating estate plan to reflect changing circumstances, reviewing asset allocation.

-

Late Life (75+):

- Focus: Simplifying estate plan, addressing end-of-life issues, providing clear instructions.

- Key Documents: Will, trust, power of attorney, healthcare proxy, letter of intent.

- Considerations: Consolidating assets, clarifying end-of-life wishes, ensuring family members are aware of your plans.

15. Understanding Wills and Trusts in Estate Planning

Wills and trusts are fundamental tools in estate planning, each offering unique benefits and serving different purposes. Understanding the differences between them is crucial for creating an effective estate plan.

Wills:

- Definition: A will is a legal document that outlines how your assets should be distributed after your death.

- Key Features:

- Allows you to name an executor who will manage your estate.

- Allows you to name guardians for minor children.

- Goes through probate, a legal process that can be time-consuming and costly.

- Becomes a public record once probated.

- Advantages:

- Relatively simple to create and modify.

- Provides clear instructions for asset distribution.

- Disadvantages:

- Subject to probate.

- Becomes a public record.

- May be challenged in court.

Trusts:

- Definition: A trust is a legal arrangement in which you (the grantor) transfer assets to a trustee, who manages them for the benefit of your beneficiaries.

- Key Features:

- Avoids probate, allowing for a quicker and more private transfer of assets.

- Can be used to protect assets from creditors, lawsuits, or mismanagement.

- Can provide for loved ones with special needs.

- Offers greater flexibility and control over asset distribution.

- Advantages:

- Avoids probate.

- Provides asset protection.

- Offers greater flexibility and control.

- Remains private.

- Disadvantages:

- More complex to create and manage.

- Requires ongoing administration.

- May be more expensive to set up than a will.

Choosing Between a Will and a Trust:

-

Consider a Will if:

- Your estate is relatively simple.

- You are comfortable with the probate process.

- Privacy is not a major concern.

-

Consider a Trust if:

- You want to avoid probate.

- You need asset protection.

- You want greater control over asset distribution.

- You have complex family dynamics or special needs beneficiaries.

16. The Role of a Financial Advisor in Estate Planning

A financial advisor plays a critical role in estate planning by providing expertise in financial matters, helping you make informed decisions, and coordinating with other professionals, such as estate planning attorneys and tax advisors.

- Financial Assessment: A financial advisor can assess your current financial situation, including assets, liabilities, income, and expenses, to determine your net worth and identify potential estate planning needs.

- Goal Setting: A financial advisor can help you define your estate planning goals, such as minimizing taxes, providing for loved ones, supporting charitable causes, or ensuring business succession.

- Investment Management: A financial advisor can manage your investments to maximize growth and minimize risk, ensuring that your assets are sufficient to meet your estate planning goals.

- Retirement Planning: A financial advisor can help you plan for retirement, ensuring that you have enough income and assets to maintain your lifestyle and cover healthcare costs.

- Insurance Planning: A financial advisor can assess your insurance needs, including life insurance, long-term care insurance, and disability insurance, to protect your assets and provide for your loved ones.

- Tax Planning: A financial advisor can help you minimize taxes through various strategies, such as tax-deferred investments, charitable giving, and estate tax reduction techniques.

- Coordination with Other Professionals: A financial advisor can coordinate with other professionals, such as estate planning attorneys, tax advisors, and insurance agents, to ensure that your estate plan is comprehensive and well-integrated.

- Ongoing Monitoring and Review: A financial advisor can monitor your estate plan on an ongoing basis and make adjustments as needed to reflect changing circumstances, such as changes in your financial situation, family dynamics, or tax laws.

17. Estate Tax Planning Strategies

Estate tax planning is a critical aspect of estate planning, especially for individuals with significant wealth. The goal is to minimize estate taxes and maximize the amount of assets that are passed on to your beneficiaries.

- Gifting: Gifting assets to your loved ones during your lifetime can reduce the size of your estate and lower estate taxes. The annual gift tax exclusion allows you to gift a certain amount each year without incurring gift tax.

- Charitable Giving: Donating assets to charitable organizations can reduce your estate tax liability and support causes that you care about. Charitable bequests in your will or trust can also qualify for an estate tax deduction.

- Irrevocable Life Insurance Trust (ILIT): An ILIT is an irrevocable trust that owns your life insurance policy. By removing the life insurance proceeds from your estate, you can reduce your estate tax liability.

- Qualified Personal Residence Trust (QPRT): A QPRT is a trust that allows you to transfer your home to your beneficiaries while continuing to live in it for a specified term. This can reduce the value of your estate and lower estate taxes.

- Grantor Retained Annuity Trust (GRAT): A GRAT is a trust that allows you to transfer assets to your beneficiaries while receiving an annuity payment for a specified term. This can reduce the value of your estate and lower estate taxes.

- Family Limited Partnership (FLP): An FLP is a limited partnership that allows you to transfer assets, such as real estate or business interests, to your family members while retaining control over the assets. This can reduce the value of your estate and lower estate taxes.

- Disclaimer Trust: A disclaimer trust is a trust that is created upon the death of the first spouse. The surviving spouse can disclaim assets, which are then transferred to the trust, reducing the estate tax liability of the surviving spouse.

- Portability: Portability allows the surviving spouse to use any unused portion of the deceased spouse’s estate tax exemption. This can simplify estate tax planning and ensure that the full estate tax exemption is utilized.

18. How to Handle Digital Assets in Estate Planning

In today’s digital age, it’s essential to include digital assets in your estate plan. Digital assets include online accounts, social media profiles, digital wallets, and other electronic information.

- Inventory of Digital Assets: Create a detailed list of all your digital assets, including usernames, passwords, and account information.

- Designate a Digital Executor: Appoint a digital executor who will manage your digital assets after your death.

- Provide Instructions: Provide clear instructions on how you want your digital assets to be managed, such as whether you want them to be closed, transferred, or memorialized.

- Use a Password Manager: Use a password manager to securely store your usernames and passwords and share them with your digital executor.

- Include Digital Assets in Your Will or Trust: Include digital assets in your will or trust to ensure they are properly managed and distributed.

- Review and Update Regularly: Review and update your digital estate plan regularly to reflect changes in your digital assets and preferences.

- Legal Considerations: Be aware of legal considerations, such as privacy laws and terms of service agreements, when managing digital assets.

- Communicate with Family Members: Communicate with your family members about your digital estate plan to ensure they are aware of your wishes and responsibilities.

19. International Estate Planning Considerations

If you have assets or family members in multiple countries, international estate planning is essential. International estate planning involves navigating complex legal, tax, and cultural issues to ensure that your estate is properly managed and distributed.

- Cross-Border Wills: Create wills in each country where you have assets to ensure that your estate is properly managed and distributed according to local laws.

- Tax Planning: Consult with a tax advisor to understand the tax implications of owning assets in multiple countries and develop strategies to minimize taxes.

- Treaties: Be aware of treaties between countries that may affect your estate planning, such as tax treaties and estate tax treaties.

- Cultural Differences: Consider cultural differences in estate planning practices and traditions when creating your estate plan.

- Language Barriers: Ensure that all estate planning documents are translated into the appropriate languages to avoid misunderstandings.

- Legal Expertise: Consult with attorneys who are experienced in international estate planning to ensure that your estate plan is compliant with all applicable laws.

- Currency Exchange: Be aware of currency exchange rates and how they may affect the value of your assets.

- Communication with Family Members: Communicate with your family members about your international estate plan to ensure they are aware of your wishes and responsibilities.

DailyMailTV exclusively obtained Lee Radziwill

DailyMailTV exclusively obtained Lee Radziwill

20. Common Questions About Estate Planning

- What is estate planning?

Estate planning is the process of arranging for the management and distribution of your assets after your death or in the event of incapacitation.

- Why is estate planning important?

Estate planning is important because it ensures that your assets are distributed according to your wishes, minimizes taxes, protects your loved ones, and provides for their future.

- When should I start estate planning?

You should start estate planning as soon as you have assets and loved ones to protect. It’s never too early to begin the process.

- What are the basic components of an estate plan?

The basic components of an estate plan include a will, trust, power of attorney, healthcare proxy, and beneficiary designations.

- What is a will?

A will is a legal document that outlines how your assets should be distributed after your death.

- What is a trust?

A trust is a legal arrangement in which you (the grantor) transfer assets to a trustee, who manages them for the benefit of your beneficiaries.

- What is probate?

Probate is the legal process of validating a will and distributing assets after death.

- How can I avoid probate?

You can avoid probate by using trusts, joint ownership, and beneficiary designations.

- What is a power of attorney?

A power of attorney is a legal document that authorizes someone (your agent) to act on your behalf in financial and legal matters if you become incapacitated.

- What is a healthcare proxy?

A healthcare proxy (also known as a medical power of attorney) allows you to appoint someone to make healthcare decisions for you if you are unable to do so.

FAQ About Lee Radziwill’s Estate

- Who inherited Lee Radziwill’s money?

Lee Radziwill’s daughter, Anna Christina “Tina” Radziwill, inherited the majority of her estate.

- Did Carole Radziwill inherit anything from Lee Radziwill?

No, Carole Radziwill was not mentioned in Lee Radziwill’s will.

- How much money did Lee Radziwill leave behind?

Lee Radziwill’s estimated net worth at the time of her death was $50 million.

- Who were the executors of Lee Radziwill’s estate?

Hamilton South and Martin B. O’Connor II were the executors of Lee Radziwill’s estate.

- What happened to Lee Radziwill’s co-op apartment?

Lee Radziwill’s will directed her executors to sell her co-op apartment, and the proceeds were to be included as part of her estate.

- Did Jackie Kennedy leave Lee Radziwill any money in her will?

No, Jackie Kennedy did not leave Lee Radziwill any money in her will, stating that she had already provided for her during her lifetime.

- What was the value of Lee Radziwill’s trust from her mother?

The principal value of the trust was not revealed in Lee Radziwill’s will.

- How did Lee Radziwill address funeral expenses in her will?

Lee Radziwill’s will directed that all debts and funeral expenses be paid as soon as practicable after her death.

- Was Caroline Kennedy Schlossberg included in Lee Radziwill’s will?

No, Caroline Kennedy Schlossberg was not included in Lee Radziwill’s will.

- What is the importance of having executors in a will?

Executors ensure that the will is followed and that the estate is managed according to the deceased’s wishes.

Conclusion: Securing Your Financial Future

Lee Radziwill’s estate provides a fascinating glimpse into the world of high society and the complexities of estate planning. Her decisions about who would inherit her wealth reflect personal relationships, family dynamics, and strategic financial planning. For anyone looking to secure their financial future and ensure their assets are distributed according to their wishes, understanding the nuances of estate planning is essential.

Ready to take control of your financial future? Visit money-central.com today for comprehensive articles, tools, and expert advice on estate planning and wealth management in the USA. Whether you’re just starting or have a complex estate, we have the resources you need to make informed decisions and achieve your financial goals.

Address: 44 West Fourth Street, New York, NY 10012, United States

Phone: +1 (212) 998-0000

Website: money-central.com

Start planning your legacy today with money-central.com.