Are you wondering, “How Do I Withdraw Money From My Hsa Account?” Withdrawing funds from your Health Savings Account (HSA) is straightforward, whether for qualified medical expenses or other needs, and money-central.com is here to guide you through the process. Understanding the rules and regulations, especially regarding qualified medical expenses and potential penalties, is crucial for maximizing the benefits of your HSA and avoiding tax implications.

1. What Is a Health Savings Account (HSA)?

An HSA is a tax-advantaged savings account that can be used to pay for healthcare expenses. HSAs are available to taxpayers who have a high-deductible health insurance plan (HDHP). According to the IRS, for 2024, an HDHP is defined as a health plan with a deductible of at least $1,600 for an individual or $3,200 for a family.

1.1 What are the Benefits of Having an HSA?

There are many benefits to having an HSA, including:

- Tax deductions: Contributions to an HSA are tax-deductible, which lowers your taxable income.

- Tax-free growth: The money in your HSA grows tax-free.

- Tax-free withdrawals: Withdrawals from an HSA for qualified medical expenses are tax-free.

- Portability: If you change jobs or retire, your HSA account will stay with you.

- Investment options: Many HSAs offer investment options, which allows you to grow your savings faster.

1.2 Who is Eligible to Open an HSA?

To be eligible to open an HSA, you must meet the following requirements:

- You must have a high-deductible health insurance plan (HDHP).

- You must not be covered by any other health insurance plan that is not an HDHP, such as a spouse’s plan.

- You must not be enrolled in Medicare.

- You must not be claimed as a dependent on someone else’s tax return.

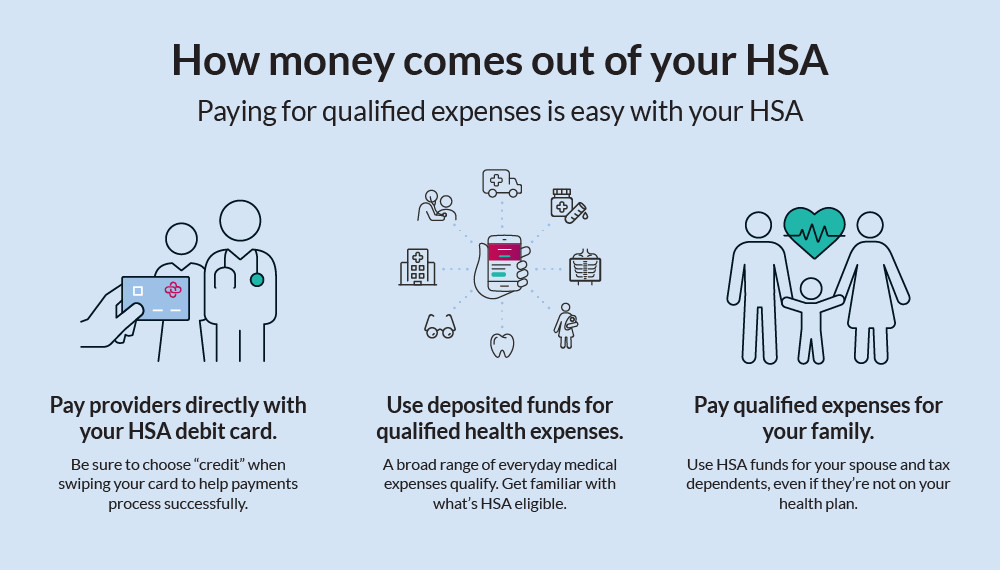

2. What Are Qualified Medical Expenses?

Qualified medical expenses are costs for diagnosis, cure, mitigation, treatment, or prevention of disease, and for treatments affecting any part or function of the body. These expenses can be for yourself, your spouse, or your dependents. The IRS defines eligible healthcare expenses, and it’s essential to know what these are.

HSA qualified medical expenses

HSA qualified medical expenses

2.1 What Expenses Qualify for HSA Withdrawals?

Some of the eligible medical expenses include:

- Copays, coinsurance, and deductibles: These are out-of-pocket costs for doctor visits, hospital stays, and other medical services.

- Prescriptions: The cost of prescription drugs is an eligible expense.

- Dental care: Including check-ups, cleanings, fillings, braces, and dentures.

- Eye care: Including eye exams, eyeglasses, and contact lenses.

- Mental health care: Therapy, counseling, and psychiatric care are included.

- Medical equipment: Such as crutches, wheelchairs, and walkers.

- Long-term care: Services for those unable to care for themselves due to chronic illness or disability.

- COBRA and Medicare premiums: Though health insurance premiums are generally ineligible, COBRA and Medicare premiums are exceptions.

2.2 What Expenses Don’t Qualify for HSA Withdrawals?

It’s also important to know what expenses do not qualify, such as:

- Cosmetic surgery: Unless it is medically necessary to correct a deformity or injury.

- Non-prescription medications: Over-the-counter drugs are generally not eligible unless prescribed by a doctor.

- Health club dues: Gym memberships are typically not considered medical expenses.

- Personal care items: Like toiletries and other personal hygiene products.

2.3 IRS Guidelines on Qualified Medical Expenses

The IRS provides detailed guidelines on what constitutes a qualified medical expense in Publication 502, Medical and Dental Expenses. According to the IRS, qualified medical expenses are those incurred for the diagnosis, cure, mitigation, treatment, or prevention of disease, or for the purpose of affecting any structure or function of the body. These expenses can include payments for:

- Doctors, dentists, and other medical practitioners

- Hospitals

- Laboratory fees

- Insurance premiums (under certain conditions, such as for long-term care policies)

- Prescription drugs

It is crucial to consult IRS Publication 502 or a tax advisor to ensure that expenses qualify before withdrawing funds from an HSA, especially for less common medical treatments or services.

3. How Do I Withdraw Money From My HSA?

Withdrawing money from your HSA is generally a straightforward process, but the exact method can vary depending on your HSA provider. Here are common methods for accessing your HSA funds:

3.1 HSA Debit Card

Many HSAs provide a debit card linked directly to your account. This is one of the most convenient ways to pay for eligible medical expenses.

- How it works: Use the debit card at the point of sale, just like any other debit card, when paying for qualified medical expenses at pharmacies, doctor’s offices, hospitals, and other healthcare providers.

- Advantages: Simple and immediate payment method.

- Considerations: Keep detailed records of your transactions to verify that all expenses are qualified, as the IRS may require proof during an audit.

3.2 Online Bill Payment

Some HSA providers offer online bill payment services, allowing you to pay medical bills directly from your HSA account.

- How it works: Log in to your HSA account online and use the bill payment feature to send payments to healthcare providers.

- Advantages: Streamlines the payment process and reduces the need for paper checks.

- Considerations: Ensure that the provider is set up to accept electronic payments from your HSA.

3.3 Reimbursement

If you pay for a qualified medical expense out-of-pocket, you can reimburse yourself from your HSA.

- How it works: Pay for the expense using your own funds and then submit a claim to your HSA provider with documentation (receipts, Explanation of Benefits). Once approved, the HSA provider will reimburse you, either by check or direct deposit to your bank account.

- Advantages: Flexibility in how you pay for expenses.

- Considerations: Requires more paperwork and time to process the reimbursement. Make sure to keep detailed records of all expenses and reimbursements.

3.4 Checks

Some HSA accounts provide check-writing privileges, allowing you to write checks to pay for qualified medical expenses.

- How it works: Write a check to the healthcare provider and mail or hand-deliver it.

- Advantages: Useful for situations where debit cards or online payments are not accepted.

- Considerations: Keep a detailed record of each check, including the date, payee, and purpose, to ensure proper documentation for tax purposes.

3.5 Distribution Request Form

If none of the above methods work, you can use a distribution request form.

- How it works: Complete a form and submit it to your HSA provider. The form typically requires information about the expense, the amount, and the payee.

- Advantages: Suitable for less common situations or when other methods are unavailable.

- Considerations: May take longer to process compared to other methods. Ensure all required information is accurately filled out to avoid delays.

3.6 Record-Keeping

Regardless of the method you choose, it’s important to keep detailed records of all HSA transactions. This includes receipts, Explanation of Benefits (EOBs) from your insurance company, and any other documentation that proves the expense was a qualified medical expense. Good record-keeping will help you in case of an audit by the IRS and ensure that you are using your HSA funds correctly.

3.7 HSA Withdrawal for Non-Medical Expenses

Withdrawing funds from an HSA for non-medical expenses is possible, but it’s important to understand the tax implications. If you are under the age of 65, withdrawals for non-qualified expenses are subject to income tax and a 20% penalty. After age 65, withdrawals for non-qualified expenses are taxed as ordinary income, but the 20% penalty is waived.

It’s generally advisable to use HSA funds for qualified medical expenses to avoid taxes and penalties. However, in situations where you need funds for other purposes, it’s good to know that you can access the money, albeit with tax implications.

4. HSA Withdrawal Rules and Regulations

Understanding the rules and regulations for HSA withdrawals is critical to avoiding penalties and maximizing the tax benefits of your account. Here are key rules and regulations to keep in mind:

4.1 Qualified Medical Expenses

- Definition: As mentioned earlier, qualified medical expenses are those incurred for the diagnosis, cure, mitigation, treatment, or prevention of disease, or for the purpose of affecting any structure or function of the body.

- IRS Publication 502: Consult IRS Publication 502 for a comprehensive list of qualified medical expenses.

- Documentation: Always keep detailed records of all medical expenses to substantiate withdrawals.

4.2 Age Restrictions

- Under Age 65: Withdrawals for non-qualified expenses are subject to income tax and a 20% penalty.

- Age 65 and Older: Withdrawals for non-qualified expenses are subject to income tax but are not subject to the 20% penalty. This makes the HSA function similarly to a traditional IRA or 401(k) in retirement, but with the added benefit of tax-free withdrawals for qualified medical expenses.

4.3 Medicare Enrollment

- Impact on Contributions: Once you enroll in Medicare, you can no longer contribute to your HSA. However, you can still use the funds in your HSA for qualified medical expenses.

- Withdrawals: Medicare premiums can be paid from your HSA, which is a significant benefit for retirees.

4.4 Coordination with Other Health Coverage

- Dual Coverage: You cannot contribute to an HSA if you are covered by another health plan that is not a high-deductible health plan (HDHP). This includes coverage through a spouse’s plan or other non-HDHP insurance.

- Exceptions: Limited exceptions exist, such as specific types of supplemental insurance or coverage for accidents, disability, dental care, or vision care.

4.5 Timing of Withdrawals

- Expense Incurred: Withdrawals must be for expenses that have already been incurred. You cannot withdraw funds for anticipated future medical expenses.

- Substantiation: The IRS may require proof that withdrawals were used for qualified medical expenses, so it’s essential to maintain thorough records.

4.6 State Taxes

- State Laws: While federal law provides tax advantages for HSAs, state laws may vary. Some states may not recognize the tax benefits of HSAs, so it’s important to check your state’s tax laws.

4.7 Rollovers and Transfers

- Rollovers: You can roll over funds from one HSA to another, but you must do so within 60 days of receiving the funds. You can only do one rollover per 12-month period.

- Transfers: You can transfer funds directly from one HSA to another without any limitations on the number of transfers per year.

4.8 Estate Planning

- Inheritance: If you die, your HSA can be passed on to your spouse or other beneficiaries. If your spouse inherits the HSA, it is treated as their own HSA. If another beneficiary inherits the HSA, the account ceases to be an HSA, and the funds are subject to income tax.

4.9 Using HSA Funds While Unemployed

If you become unemployed, your HSA funds remain available to you for qualified medical expenses. Since you are no longer contributing to the HSA, it’s even more important to manage the funds wisely. You can use the funds to pay for COBRA premiums, which can help maintain your health insurance coverage during unemployment.

4.10 Penalties for Non-Compliance

- Incorrect Withdrawals: If you use HSA funds for non-qualified expenses before age 65, you will be subject to income tax and a 20% penalty.

- Record-Keeping: Failure to maintain adequate records can result in penalties if the IRS audits your account.

5. Withdrawing Funds Before and After Age 65

The rules for withdrawing money from an HSA change once you turn 65. It’s important to understand these differences to make informed decisions about your healthcare spending.

5.1 Withdrawing Funds Before Age 65

Before age 65, the rules are stricter. You can withdraw money from your HSA to pay for qualified medical expenses. If you use your HSA contributions to pay for anything else, you will have to pay income taxes on the withdrawn amount as well as a 20% penalty.

- Qualified Medical Expenses: As defined by the IRS, these include costs for diagnosis, cure, mitigation, treatment, or prevention of disease.

- Tax Implications: Using HSA funds for non-qualified expenses results in taxation and a 20% penalty.

5.2 Withdrawing Funds After Age 65

After you turn 65, your HSA functions more like a traditional retirement account. If you spend the money on qualified medical expenses it still comes out of your HSA tax-free. If you spend the money on anything else, you pay income tax on the withdrawal, but you’re not subject to the 20% penalty.

- Flexibility: Greater flexibility in how you use the funds without incurring penalties.

- Tax Implications: Withdrawals for non-medical expenses are taxed as ordinary income.

5.3 Key Differences

Here’s a table summarizing the key differences in HSA withdrawals before and after age 65:

| Feature | Before Age 65 | After Age 65 |

|---|---|---|

| Qualified Medical Expenses | Tax-free withdrawal | Tax-free withdrawal |

| Non-Medical Expenses | Income tax + 20% penalty | Income tax only |

| Account Function | Primarily for medical expenses | More like a retirement account |

| Penalty | 20% penalty for non-medical use | No penalty for non-medical use |

| Tax Advantages | Maximize tax-free medical spending | Tax-free medical, taxed non-medical |

5.4 Strategies for Maximizing HSA Benefits at Different Ages

- Before Age 65: Focus on using HSA funds for qualified medical expenses to maximize tax benefits and avoid penalties. Keep detailed records of all expenses to ensure compliance with IRS rules.

- After Age 65: Utilize HSA funds for medical expenses to continue enjoying tax-free withdrawals. If you need funds for non-medical purposes, understand that these withdrawals will be taxed as ordinary income.

- Investment: Consider investing a portion of your HSA funds to grow your savings over time. This can be particularly beneficial for long-term healthcare needs.

6. Investing Your HSA Funds

One of the significant advantages of an HSA is the ability to invest your funds, allowing them to grow tax-free over time. Here’s how you can invest your HSA funds and what to consider:

6.1 How to Invest Your HSA Funds

-

Check with Your HSA Provider:

- Not all HSA providers offer investment options. Check with your provider to see if they allow you to invest your funds.

- Some providers may require you to maintain a certain cash balance before you can start investing.

-

Open an Investment Account:

- If your HSA provider offers investment options, you will need to open an investment account within your HSA.

- This account will be separate from your cash account, which is used for day-to-day medical expenses.

-

Transfer Funds:

- Transfer funds from your cash account to your investment account.

- Be aware of any fees or restrictions on transfers.

-

Choose Your Investments:

- Most HSA investment accounts offer a variety of investment options, such as mutual funds, stocks, and bonds.

- Consider your risk tolerance, investment timeline, and financial goals when choosing your investments.

-

Monitor Your Investments:

- Regularly review your investment performance and make adjustments as needed.

- Keep in mind that investment values can fluctuate, and you could lose money.

6.2 Types of Investments

- Mutual Funds: A popular choice for HSA investing, mutual funds offer diversification and professional management.

- Stocks: Investing in individual stocks can offer higher potential returns, but also comes with higher risk.

- Bonds: Bonds are generally less risky than stocks and can provide a steady stream of income.

- Exchange-Traded Funds (ETFs): ETFs are similar to mutual funds but trade like stocks, offering flexibility and diversification.

6.3 Risks and Considerations

- Market Risk: The value of your investments can fluctuate based on market conditions.

- Investment Fees: Be aware of any fees associated with investing your HSA funds, such as management fees or transaction fees.

- Liquidity: Consider your need for liquidity. If you anticipate needing the funds for medical expenses in the near future, you may want to choose more conservative investments.

- Tax Implications: While investment growth within an HSA is tax-free, it’s essential to understand the potential tax implications of selling investments and transferring funds back to your cash account for qualified medical expenses.

6.4 Professional Financial Advice

If you’re unsure about how to invest your HSA funds, consider seeking advice from a financial advisor. They can help you create an investment strategy that aligns with your financial goals and risk tolerance. Remember, the goal is to grow your HSA funds over time to cover future healthcare expenses.

7. Transferring or Rolling Over HSA Funds

There may be situations where you want to move your HSA funds from one provider to another. This can be done through a transfer or a rollover. Here’s how each method works:

7.1 HSA Transfer

A transfer involves directly moving your HSA funds from one provider to another without you taking possession of the funds.

-

How it Works:

- Open a New HSA: Start by opening a new HSA account with the provider of your choice.

- Contact Your Current HSA Provider: Notify your current provider that you want to transfer your funds to the new HSA.

- Complete Transfer Paperwork: Fill out and submit the necessary transfer paperwork to both your current and new HSA providers.

- Direct Transfer: Your current provider will directly transfer the funds to your new HSA.

-

Advantages:

- Unlimited Transfers: You can make unlimited transfers from one HSA to another without tax implications.

- No 60-Day Limit: There is no 60-day limit for completing the transfer.

-

Considerations:

- Paperwork: Requires coordination between both HSA providers.

- Timeframe: May take a few weeks to complete the transfer.

7.2 HSA Rollover

A rollover involves you taking temporary possession of the HSA funds before depositing them into a new HSA account.

-

How it Works:

- Request a Distribution: Request a distribution from your current HSA provider.

- Receive the Funds: The provider will send you a check or deposit the funds into your bank account.

- Deposit into New HSA: Within 60 days of receiving the funds, deposit them into your new HSA account.

-

Advantages:

- Flexibility: You have temporary access to the funds.

-

Considerations:

- 60-Day Limit: You must deposit the funds into a new HSA within 60 days to avoid taxes and penalties.

- One Rollover per Year: You can only do one rollover per 12-month period.

- Tax Implications: If you fail to deposit the funds within 60 days, the distribution will be considered a taxable event and subject to a 20% penalty if you are under age 65.

7.3 Which Method is Better?

In most cases, a transfer is the preferred method for moving HSA funds because it allows unlimited movement of funds from one HSA to another.

7.4 Scenarios for Transferring or Rolling Over Funds

- Better Investment Options: If another HSA provider offers better investment options or lower fees, you may want to transfer your funds.

- Improved Customer Service: If you are dissatisfied with the customer service of your current HSA provider, you may want to switch to a different provider.

- Employer Change: If you change jobs and your new employer uses a different HSA provider, you may want to transfer your funds to that provider for convenience.

8. Using Your HSA in Retirement

One of the most significant advantages of an HSA is its potential as a retirement savings tool. Here’s how you can use your HSA in retirement to cover healthcare expenses and supplement your retirement income:

8.1 Tax-Free Withdrawals for Qualified Medical Expenses

- Continued Benefit: Even in retirement, you can continue to use your HSA funds for qualified medical expenses on a tax-free basis.

- Medicare Premiums: You can use your HSA funds to pay for Medicare premiums, except for Medigap policies.

- Long-Term Care: HSA funds can be used for long-term care services, making it a valuable resource for managing healthcare costs in retirement.

8.2 Non-Medical Withdrawals After Age 65

- Flexibility: After age 65, you can withdraw funds from your HSA for non-medical expenses without incurring a penalty.

- Tax Implications: Non-medical withdrawals are subject to ordinary income tax, similar to withdrawals from a traditional IRA or 401(k).

8.3 Strategies for Using Your HSA in Retirement

- Maximize Contributions: If you are still working and eligible to contribute to an HSA, maximize your contributions to build a substantial retirement healthcare fund.

- Invest Wisely: Invest your HSA funds in a diversified portfolio to grow your savings over time.

- Plan for Future Healthcare Costs: Estimate your future healthcare expenses and plan your withdrawals accordingly to ensure you have sufficient funds to cover your needs.

- Coordinate with Other Retirement Accounts: Coordinate your HSA withdrawals with withdrawals from other retirement accounts to minimize your overall tax liability.

8.4 Considerations for Estate Planning

- Inheritance: If you die, your HSA can be passed on to your spouse or other beneficiaries.

- Spouse: If your spouse inherits the HSA, it is treated as their own HSA and can be used for qualified medical expenses.

- Non-Spouse: If a non-spouse beneficiary inherits the HSA, the account ceases to be an HSA, and the funds are subject to income tax.

8.5 The Future of HSAs

As healthcare costs continue to rise, HSAs are likely to become an even more important tool for managing healthcare expenses in retirement. Staying informed about the latest HSA rules and regulations can help you make the most of this valuable savings vehicle.

9. Common Mistakes to Avoid When Withdrawing From Your HSA

To ensure you’re using your HSA funds correctly and maximizing its benefits, here are some common mistakes to avoid when making withdrawals:

9.1 Using Funds for Non-Qualified Expenses Before Age 65

- Mistake: Withdrawing funds for non-qualified expenses before age 65 results in income tax and a 20% penalty.

- Solution: Only use HSA funds for qualified medical expenses before age 65 to avoid penalties and taxes.

9.2 Not Keeping Detailed Records

- Mistake: Failing to keep receipts, Explanation of Benefits (EOBs), and other documentation to substantiate your withdrawals.

- Solution: Maintain thorough records of all medical expenses and HSA transactions in case of an audit by the IRS.

9.3 Withdrawing Funds for Ineligible Expenses

- Mistake: Using HSA funds for expenses that do not qualify as medical expenses under IRS guidelines.

- Solution: Consult IRS Publication 502 for a comprehensive list of qualified medical expenses, and verify eligibility before making a withdrawal.

9.4 Not Understanding HSA Rules

- Mistake: Lack of understanding of HSA rules and regulations, leading to improper use of funds.

- Solution: Familiarize yourself with HSA rules, including eligibility requirements, contribution limits, and withdrawal guidelines.

9.5 Failing to Transfer or Roll Over Funds Correctly

- Mistake: Not following the proper procedures for transferring or rolling over HSA funds, resulting in tax implications.

- Solution: Understand the difference between a transfer and a rollover, and follow the correct steps to avoid taxes and penalties.

9.6 Withdrawing Funds After Medicare Enrollment

- Mistake: Continuing to contribute to an HSA after enrolling in Medicare.

- Solution: Stop contributing to your HSA once you enroll in Medicare, but continue to use the funds for qualified medical expenses.

9.7 Overlooking State Tax Laws

- Mistake: Assuming that the federal tax benefits of HSAs apply in your state.

- Solution: Check your state’s tax laws to see if they recognize the tax benefits of HSAs.

9.8 Not Coordinating with Other Health Coverage

- Mistake: Contributing to an HSA while covered by another health plan that is not a high-deductible health plan (HDHP).

- Solution: Ensure that you are only covered by an HDHP to be eligible to contribute to an HSA.

9.9 Delaying Reimbursements

- Mistake: Waiting too long to reimburse yourself for qualified medical expenses.

- Solution: Submit your reimbursement requests in a timely manner to avoid any complications or delays.

9.10 Not Seeking Professional Advice

- Mistake: Making financial decisions without consulting a financial advisor or tax professional.

- Solution: Seek professional advice to ensure you are making informed decisions about your HSA and other financial matters.

10. Frequently Asked Questions (FAQs) About HSA Withdrawals

Here are some frequently asked questions about HSA withdrawals to help clarify any confusion:

10.1 Can I use my HSA to pay for my spouse’s or dependent’s medical expenses?

Yes, you can use your HSA to pay for qualified medical expenses for yourself, your spouse, and your dependents.

10.2 What happens if I withdraw money from my HSA for non-qualified expenses before age 65?

You will be subject to income tax and a 20% penalty on the withdrawn amount.

10.3 Can I use my HSA to pay for health insurance premiums?

Generally, no. However, there are exceptions for COBRA premiums, Medicare premiums, and long-term care insurance premiums.

10.4 Can I contribute to an HSA if I am enrolled in Medicare?

No, you cannot contribute to an HSA if you are enrolled in Medicare. However, you can still use the funds in your HSA for qualified medical expenses.

10.5 What is the deadline for reimbursing myself for medical expenses from my HSA?

There is no specific deadline for reimbursing yourself for medical expenses from your HSA, but it’s a good practice to do it in the same year the expense was incurred.

10.6 Can I transfer my HSA to another provider?

Yes, you can transfer your HSA to another provider through a direct transfer or a rollover. A direct transfer is generally preferred because it doesn’t have the same restrictions as a rollover.

10.7 What happens to my HSA if I die?

Your HSA can be passed on to your spouse or other beneficiaries. If your spouse inherits the HSA, it is treated as their own HSA. If another beneficiary inherits the HSA, the account ceases to be an HSA, and the funds are subject to income tax.

10.8 Can I invest my HSA funds?

Yes, many HSA providers offer investment options, allowing you to grow your savings over time.

10.9 How do I keep track of my HSA withdrawals and expenses?

Keep detailed records of all medical expenses, receipts, and Explanation of Benefits (EOBs) from your insurance company.

10.10 What is the difference between an HSA transfer and a rollover?

A transfer involves directly moving your HSA funds from one provider to another without you taking possession of the funds. A rollover involves you taking temporary possession of the HSA funds before depositing them into a new HSA account, and it must be completed within 60 days.

Understanding how to withdraw money from your HSA account is crucial for effectively managing your healthcare expenses and maximizing the tax benefits of this valuable savings tool. Whether you’re using your HSA for immediate medical needs or saving for retirement, knowing the rules and regulations can help you make informed decisions and avoid costly mistakes.

Ready to take control of your financial future? Visit money-central.com today to explore more articles, use our financial tools, and connect with financial experts who can provide personalized advice. Don’t wait—start building a secure financial future now!

Address: 44 West Fourth Street, New York, NY 10012, United States.

Phone: +1 (212) 998-0000.

Website: money-central.com.