Did Trump inject money into the economy during COVID? At money-central.com, we delve into the fiscal strategies employed during the pandemic, assessing the measures taken to stabilize the U.S. economy. Explore how these financial injections impacted various sectors and their long-term implications. Discover strategies for financial resilience and growth in uncertain times.

Table of Contents

- How Did the Fed Support the U.S. Economy and Financial Markets?

- Why Were the Fed’s Actions Important?

- FAQ

1. How Did the Fed Support the U.S. Economy and Financial Markets?

The Federal Reserve (also known as The Fed) played a crucial role in supporting the U.S. economy and financial markets during the COVID-19 pandemic. Understanding these interventions is essential for grasping the full scope of the economic response. Here’s a breakdown of the key actions the Fed undertook:

1.1 Easing Monetary Policy

One of the initial steps the Federal Reserve took was to ease monetary policy. How did the Fed ease monetary policy? By lowering the federal funds rate to near zero. According to research from New York University’s Stern School of Business, in July 2025, lowering the federal funds rate encourages borrowing and spending, providing immediate relief to consumers and businesses. This action made it cheaper for banks to borrow money, which they could then lend to individuals and companies at lower interest rates. Lower interest rates translate to reduced borrowing costs for businesses, encouraging investment and expansion. For consumers, it meant lower rates on mortgages, auto loans, and credit cards, freeing up more disposable income. This was vital in maintaining consumer spending, which constitutes a significant portion of the U.S. economy.

Lowering the federal funds rate is a powerful tool, but its effectiveness depends on various factors, including consumer confidence and the willingness of banks to lend. During the pandemic, uncertainty was high, and even low interest rates couldn’t fully overcome the reluctance to borrow and invest. To complement this, the Fed implemented other measures to directly support financial markets and ensure credit flowed smoothly.

1.2 Supporting Financial Markets

Beyond lowering interest rates, the Fed implemented several programs to directly support financial markets. What did the Fed do to support financial markets? The Fed launched numerous facilities to provide liquidity and stability. These facilities aimed to address specific pain points in the market, ensuring that credit continued to flow even when traditional channels were disrupted.

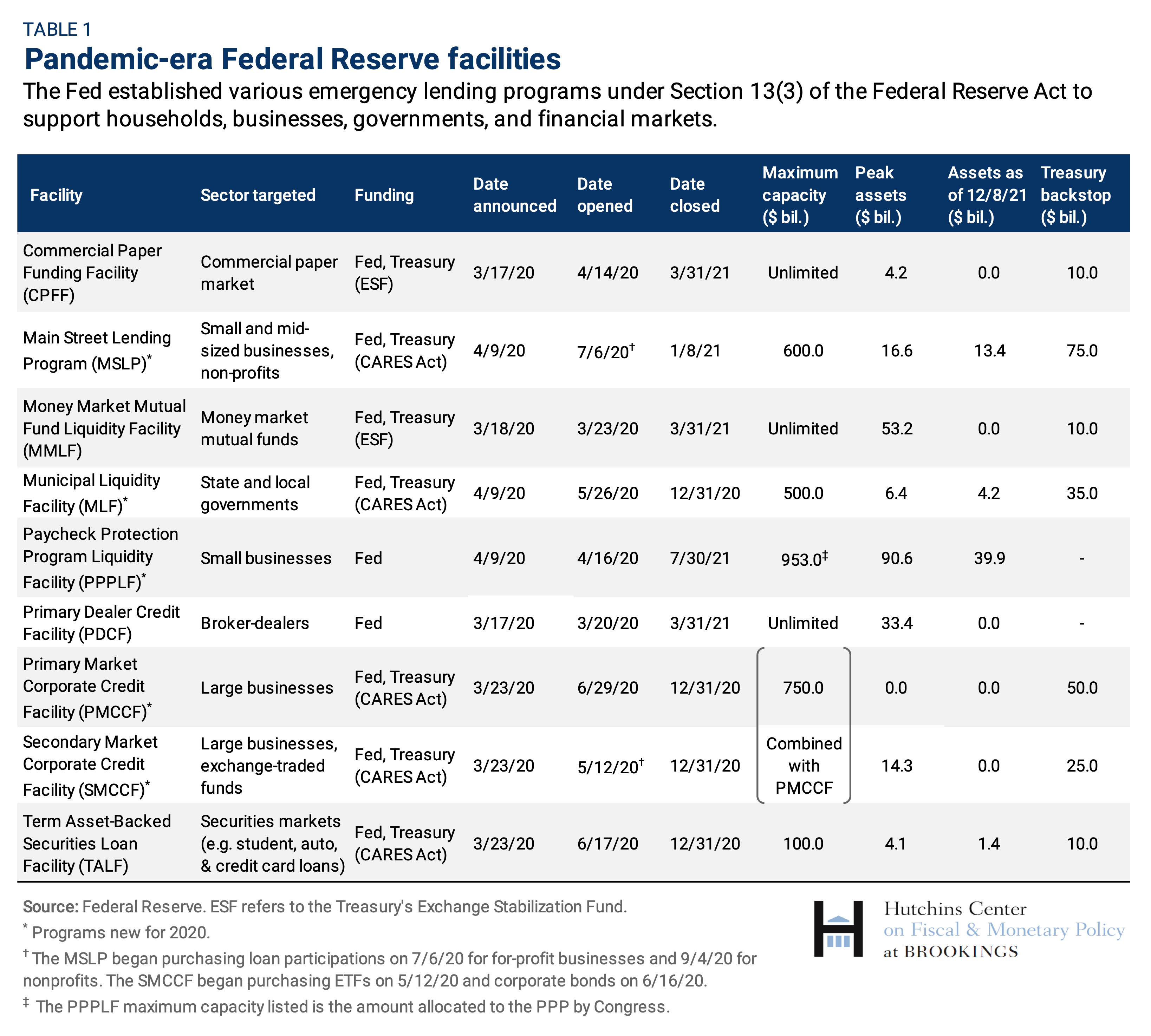

- The Primary Dealer Credit Facility (PDCF) offered overnight loans to primary dealers, which are firms that trade directly with the Fed. This helped ensure these key market participants had access to the funds they needed to maintain market liquidity.

- The Commercial Paper Funding Facility (CPFF) supported the commercial paper market, where companies issue short-term debt to fund their day-to-day operations. By purchasing commercial paper, the Fed helped companies continue to access this vital source of funding.

- The Money Market Mutual Fund Liquidity Facility (MMLF) provided loans to banks to purchase assets from money market mutual funds. Money market funds are a popular investment option, and this facility helped prevent a run on these funds, which could have destabilized the broader financial system.

- The Term Asset-Backed Securities Loan Facility (TALF) supported the market for asset-backed securities, such as auto loans and credit card debt. By providing financing for these securities, the Fed helped ensure that credit remained available to consumers.

Pandemic-era Federal Reserve Facilities

Pandemic-era Federal Reserve Facilities

These facilities were crucial in preventing a complete freeze in the financial markets, which would have had catastrophic consequences for the economy. By intervening directly, the Fed reassured investors and kept credit flowing to businesses and consumers.

1.3 Encouraging Banks to Lend

In addition to supporting financial markets directly, the Fed took steps to encourage banks to lend more freely. What did the Fed do to encourage banks to lend? The Fed temporarily reduced reserve requirements for banks to zero. Reserve requirements are the amount of money banks are required to keep on hand, and by lowering these requirements, the Fed freed up banks to lend more money. This move was designed to boost the amount of capital available for lending. Banks, now with more funds at their disposal, were expected to increase lending to businesses and consumers. This increased lending capacity aimed to stimulate economic activity by providing more access to credit.

Furthermore, the Fed eased certain regulatory restrictions on banks, providing them with more flexibility in managing their capital and liquidity. The combination of reduced reserve requirements and relaxed regulations gave banks the confidence and capacity to support their customers during the crisis.

1.4 Supporting Corporations and Businesses

Recognizing the significant challenges faced by corporations and businesses, the Fed established facilities to provide direct support. How did the Fed support corporations and businesses? The Fed created the Primary Market Corporate Credit Facility (PMCCF) and the Secondary Market Corporate Credit Facility (SMCCF).

- The PMCCF allowed the Fed to purchase new bonds directly from corporations, providing them with access to capital even if they couldn’t obtain it elsewhere.

- The SMCCF allowed the Fed to purchase existing corporate bonds in the secondary market, providing liquidity and helping to stabilize bond prices.

These facilities were particularly important for larger companies that rely on bond markets for funding. By intervening in these markets, the Fed helped prevent widespread corporate bankruptcies and job losses. However, it’s worth noting that these facilities were primarily used by investment-grade companies, leaving smaller and riskier businesses with fewer options.

1.5 Supporting Households and Consumers

Recognizing the financial strain on households and consumers, the Fed implemented measures to provide direct support. What did the Fed do to support households and consumers? By supporting asset-backed securities, the Fed ensured credit remained available. Through the TALF, the Fed aimed to lower borrowing costs for auto loans and credit cards. This initiative made it easier for consumers to afford essential purchases and manage their debt.

The Fed also worked with other agencies to support mortgage markets, helping to keep mortgage rates low and prevent a wave of foreclosures. These measures were essential in helping households weather the economic storm and maintain their financial stability.

1.6 Supporting State and Municipal Borrowing

The Fed also recognized the challenges faced by state and municipal governments, which were dealing with increased expenses and reduced tax revenues. How did the Fed support state and municipal borrowing? The Fed created the Municipal Liquidity Facility (MLF). This facility provided loans to state and local governments. This support helped these governments continue to provide essential services and avoid drastic budget cuts. The MLF offered loans to U.S. states, including the District of Columbia, counties with at least 500,000 residents, and cities with at least 250,000 residents.

The facility made $500 billion available to government entities that had investment-grade credit ratings as of April 8, 2020, in exchange for notes tied to future tax revenues with maturities of less than three years. The New York Metropolitan Transportation Authority (MTA) took advantage of this provision in August, borrowing $451 million from the facility.

The Fed also used two of its credit facilities to backstop muni markets, expanding the eligible collateral for the MMLF to include municipal variable-rate demand notes and highly rated municipal debt with maturities of up to 12 months.

These measures were vital in preventing a fiscal crisis at the state and local level, which could have further destabilized the economy.

2. Why Were the Fed’s Actions Important?

The actions taken by the Federal Reserve were critical in mitigating the economic impact of the COVID-19 pandemic. Why were the Fed’s actions important? The Fed’s interventions helped prevent a complete collapse of the financial system. The pandemic led to a sudden and deep recession, with millions of jobs lost and businesses shuttered. The Fed’s swift and decisive actions ensured that credit continued to flow to households and businesses. This prevented financial market disruptions from intensifying the economic damage.

In the U.S., a significant amount of credit flows through capital markets, and the Fed worked to keep them functioning as smoothly as possible. By intervening directly in the markets for corporate and municipal debt, the Fed ensured that key economic actors could raise funds to pay workers and avoid bankruptcies. These measures aimed to help businesses survive the crisis and resume hiring and production when the pandemic ebbed.

Banks also needed support to keep credit flowing. The Fed supplied unlimited liquidity to financial institutions so they could meet credit drawdowns and make new loans to businesses and households feeling financial strains. These actions were critical in preventing a deeper and more prolonged economic downturn.

Navigating Financial Uncertainty with Money-Central.com

Understanding the Fed’s actions is just one piece of the puzzle when it comes to navigating financial uncertainty. At money-central.com, we provide comprehensive and easy-to-understand information on a wide range of financial topics. Whether you’re looking to create a budget, save for retirement, or invest wisely, our resources can help you take control of your finances.

We understand the challenges individuals and families face when managing their money, and we’re committed to providing you with the tools and knowledge you need to succeed. Visit money-central.com today to explore our articles, calculators, and expert advice.

2.1 Challenges and Opportunities

While the Fed’s actions were largely successful in preventing a financial meltdown, they also created new challenges. What challenges arose from the Fed’s actions? The massive infusion of liquidity into the financial system raised concerns about potential inflation and asset bubbles. As the economy recovers, the Fed faces the delicate task of unwinding its emergency measures without triggering a new crisis.

Despite these challenges, the Fed’s actions also created opportunities for economic growth and innovation. The low interest rate environment encouraged investment and entrepreneurship, and the increased availability of credit helped businesses expand and create jobs. By supporting state and municipal governments, the Fed helped ensure that essential services continued to be provided.

2.2 A Path Forward

As we move forward, it’s essential to learn from the experiences of the COVID-19 pandemic and build a more resilient financial system. What is the path forward after the Fed’s Covid actions? This includes strengthening regulatory oversight of financial institutions, improving the transparency of financial markets, and promoting financial literacy among consumers.

By working together, we can create a more stable and prosperous economy for all. At money-central.com, we’re committed to providing you with the information and resources you need to navigate the challenges and opportunities ahead.

3. FAQ

3.1 What is the Federal Reserve?

The Federal Reserve System, often referred to as “the Fed,” is the central bank of the United States. It was created by Congress to provide the nation with a safer, more flexible, and more stable monetary and financial system. The Fed is responsible for setting monetary policy, supervising and regulating banks, and maintaining the stability of the financial system.

3.2 What is monetary policy?

Monetary policy refers to the actions undertaken by a central bank to manipulate the money supply and credit conditions to stimulate or restrain economic activity. The Fed uses several tools to implement monetary policy, including setting the federal funds rate, buying and selling government securities, and setting reserve requirements for banks.

3.3 What is the federal funds rate?

The federal funds rate is the target rate that the Federal Reserve wants banks to charge one another for the overnight lending of reserves. This rate influences other interest rates throughout the economy, affecting borrowing costs for businesses and consumers.

3.4 What are reserve requirements?

Reserve requirements are the amount of money that banks are required to keep on hand, either in their vaults or on deposit at the Federal Reserve. By adjusting reserve requirements, the Fed can influence the amount of money that banks have available to lend.

3.5 What is quantitative easing?

Quantitative easing (QE) is a monetary policy tool used by central banks to stimulate the economy by purchasing assets, such as government bonds or mortgage-backed securities. QE increases the money supply and lowers interest rates, encouraging borrowing and investment.

3.6 What is the Primary Market Corporate Credit Facility (PMCCF)?

The Primary Market Corporate Credit Facility (PMCCF) was a program created by the Federal Reserve during the COVID-19 pandemic to provide direct funding to corporations by purchasing new bonds directly from them. This facility aimed to help companies access capital when they couldn’t obtain it elsewhere.

3.7 What is the Secondary Market Corporate Credit Facility (SMCCF)?

The Secondary Market Corporate Credit Facility (SMCCF) was another program created by the Federal Reserve during the COVID-19 pandemic to provide liquidity and stability to the corporate bond market. The SMCCF allowed the Fed to purchase existing corporate bonds in the secondary market.

3.8 What is the Municipal Liquidity Facility (MLF)?

The Municipal Liquidity Facility (MLF) was a program created by the Federal Reserve during the COVID-19 pandemic to provide loans to state and local governments. This facility aimed to help these governments continue to provide essential services and avoid drastic budget cuts.

3.9 How did the Fed’s actions affect inflation?

The Fed’s actions during the COVID-19 pandemic, particularly the massive infusion of liquidity into the financial system, raised concerns about potential inflation. Increased money supply can lead to higher prices for goods and services if demand outstrips supply. However, the actual impact on inflation depends on various factors, including the speed of economic recovery and the Fed’s ability to manage its balance sheet.

3.10 Where can I find more information about managing my finances?

For more information about managing your finances, visit money-central.com. Our website offers a wide range of articles, calculators, and expert advice to help you take control of your financial future.