Are you wondering, How Can I Withdraw Money From My Hsa Account? This comprehensive guide from money-central.com provides clear steps and essential information on accessing your Health Savings Account (HSA) funds, ensuring you can manage your healthcare expenses effectively and maximize your financial benefits. Discover strategies for qualified medical expenses, retirement planning, and investment options, empowering you to take control of your healthcare finances. Explore additional resources on health savings strategies, financial planning, and investment growth at money-central.com.

1. What Are the Key Considerations for HSA Withdrawals Before Age 65?

If you’re under 65, you can withdraw money from your HSA for qualified medical expenses without penalty. According to IRS guidelines, using HSA funds for non-qualified expenses before age 65 results in income tax plus a 20% penalty on the withdrawn amount.

1.1. What Qualifies as a Medical Expense?

Qualified medical expenses are costs for the diagnosis, cure, mitigation, treatment, or prevention of disease, or for treatments affecting any part or function of the body, as defined by the IRS.

Examples of Qualified Medical Expenses:

- Copays

- Coinsurance

- Deductibles

- COBRA premiums

- Medicare premiums

- Prescriptions

- Dental care

- Eye care

- Crutches

- First aid supplies like Band-Aids

- Sunscreen

- Acupuncture

- Artificial limbs and teeth

- Chiropractic services

- Contact lenses and glasses

- Diagnostic devices for medical purposes

- Fertility treatments

- Hearing aids

- Home health care

- Long-term care (including nursing homes)

- Oxygen

- Pregnancy test kits

- Psychiatric and psychological care

- Special education

- Smoking cessation programs

- Vasectomies (and reversals)

- Weight loss programs for medical conditions

- Wheelchairs

- Incidental expenses for medical treatment (transportation, parking, meals, hotels)

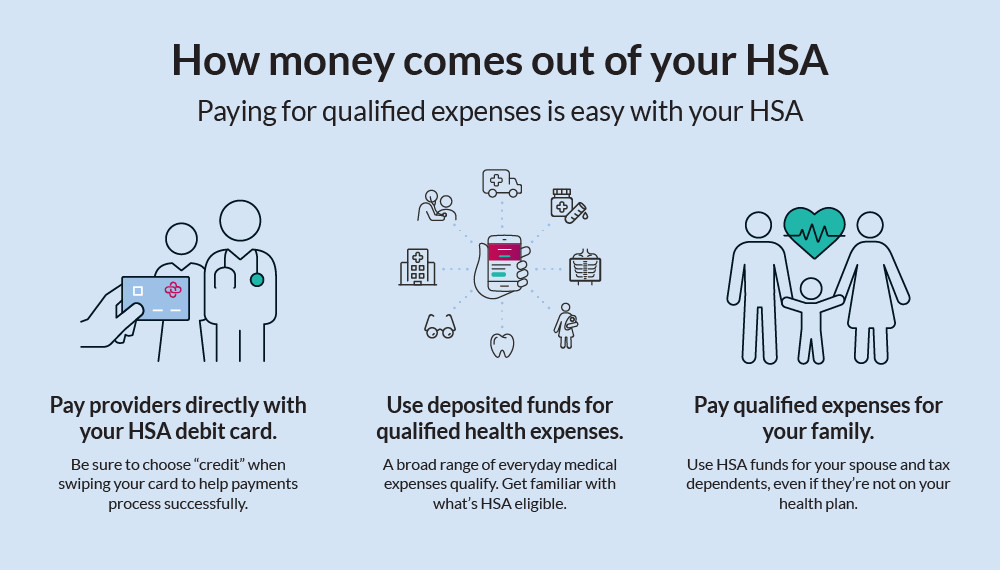

HSA infographic how money comes out of HSA

HSA infographic how money comes out of HSA

You can use your HSA to cover these costs for yourself, your spouse, and your dependents, making it a versatile tool for family healthcare management.

1.2. What Expenses Are Not Qualified?

Understanding what does not qualify as a medical expense is just as important.

Examples of Non-Qualified Medical Expenses:

- Health insurance premiums (except COBRA and Medicare)

- Childcare

- Cosmetic surgery

- Diaper service

- Funeral expenses

- Hair transplants

- Health club dues

- Maternity clothes

- Non-prescription medications

- Nutritional supplements

- Teeth whitening

- Weight loss programs not required for medical care

This list is not exhaustive; consulting Lively’s list of eligible expenses or your HR department can clarify specific situations.

2. How Do HSA Withdrawal Rules Change After Age 65?

Once you turn 65, the rules for HSA withdrawals become more flexible, offering benefits similar to traditional retirement accounts.

2.1. Tax Implications After 65

After age 65, if you use HSA funds for qualified medical expenses, the withdrawals remain tax-free, just as they were before you turned 65. However, if you use the money for non-medical expenses, you will pay income tax on the withdrawal but avoid the 20% penalty. This makes the HSA function similarly to a traditional retirement account, but with potential tax advantages for healthcare expenses.

2.2. Key Differences from Traditional Retirement Accounts

While an HSA becomes more like a retirement account after 65, there are still important distinctions:

- No Minimum Withdrawals: Unlike 401(k)s and IRAs, HSAs do not require minimum monthly disbursements at any age.

- Tax-Free Medical Withdrawals: HSA withdrawals for qualified medical expenses remain free of income tax, whereas retirement account withdrawals for the same are subject to income tax.

- Inheritance Rules: If you leave your HSA to your spouse, it becomes their HSA. If you leave it to someone else, they must take the full disbursement and pay income taxes on the inherited amount.

3. What Are the Steps to Withdraw Funds From Your HSA?

The process for withdrawing funds from your HSA is generally straightforward, but it can vary depending on your HSA provider.

3.1. Common Withdrawal Methods

- Debit Card: Most HSAs provide a debit card for direct payments at doctor’s offices, pharmacies, and other vendors.

- Checks: Some HSAs offer checks for paying directly from your account.

- Reimbursement: You can pay out-of-pocket and then reimburse yourself from your HSA.

- Online Payment Systems: Many HSAs have online systems for direct bill payments.

Regardless of the method, maintain detailed records for tax purposes.

3.2. Reimbursement Process

If your HSA doesn’t offer a debit card, you’ll likely need to pay for expenses out of pocket and seek reimbursement. This involves submitting a receipt and other documentation to your HSA administrator, who will then mail you a check or deposit the amount into your bank account.

4. How Do Withdrawals Work With Self-Directed HSAs and Investment HSAs?

Self-directed HSAs and other investment HSAs may involve a slightly more complex withdrawal process.

4.1. Understanding the Two-Account System

These HSAs typically have two separate accounts under the same umbrella:

- Cash Account: This is where contributions are deposited and from where distributions are made. Debit cards are usually linked to this account.

- Investment Account: To invest your contributions, you must move money from your cash account to your investment account.

4.2. Withdrawal Process for Investment HSAs

If you need to withdraw funds for a qualified medical expense and your cash account balance is insufficient, you’ll need to transfer money from your investment account to your cash account. If necessary, you may have to sell investments to generate the required cash. This process can take a few days. Once the money is in your cash account, you can use your debit card or request reimbursement.

5. What Happens When You Are No Longer Eligible to Contribute to Your HSA?

Eligibility to contribute to an HSA requires maintaining a High Deductible Health Plan (HDHP) as your only health coverage.

5.1. Maintaining an HSA After Losing Eligibility

If you become ineligible to contribute to your HSA due to changes in health insurance coverage or Medicare enrollment, you can still maintain and withdraw from your HSA. You just can’t add new contributions.

5.2. Maximizing Your HSA When Ineligible to Contribute

If you are no longer eligible to contribute, consider investing your existing HSA funds to allow them to grow. The withdrawal guidelines remain the same whether or not you are eligible to contribute.

6. How Can You Transfer or Roll Over HSA Funds to Another Account?

There are several reasons you might want to move your HSA funds to a different provider, such as to gain access to investment options.

6.1. Rollover vs. Transfer

- Rollover: The original HSA provider sends you a check, which you then have 60 days to deposit into a new HSA. You can roll over funds once in a 12-month period.

- Transfer: The original HSA sends the money directly to the new HSA. There are no limits on the number of transfers you can make.

Transfers are generally simpler as they eliminate the need to handle the funds yourself.

6.2. Steps for Transferring Funds

- Open a new HSA account with your preferred provider.

- Request a transfer from your original HSA to the new HSA.

- The HSA administrators will handle the transfer process directly.

7. Are There Limits to the Number of HSA Withdrawals You Can Make?

No, you have unlimited access to your HSA funds. However, be mindful of contribution limits, which are set by the IRS each year and vary based on individual, family, and age. Staying informed about these limits ensures you maximize the benefits of your HSA without penalty.

Withdrawing money from your HSA is a relatively simple process, but it’s essential to understand the rules and guidelines to avoid penalties and maximize the tax advantages. If you have specific questions about your HSA, reach out to your HR department or HSA administrator.

8. Leveraging Money-Central.com for HSA Insights and Financial Planning

At money-central.com, we understand the complexities of managing your healthcare finances and planning for the future. Our platform provides comprehensive resources, easy-to-understand articles, and powerful tools to help you make informed decisions about your HSA and overall financial well-being.

8.1. Comprehensive Financial Articles

Our articles cover a wide range of topics, including:

- In-depth guides on HSA benefits and eligibility

- Strategies for maximizing your HSA contributions

- Investment options within your HSA

- Retirement planning with your HSA

- Tax advantages and implications of HSA usage

These articles are designed to provide you with the knowledge and insights you need to confidently manage your HSA.

8.2. Financial Planning Tools

Money-central.com offers several financial planning tools to help you visualize your financial future and optimize your HSA strategy:

- HSA Contribution Calculator: Determine the optimal amount to contribute to your HSA based on your income, healthcare expenses, and financial goals.

- Retirement Savings Calculator: Project your retirement savings based on your HSA contributions and investment growth.

- Tax Savings Estimator: Estimate the tax savings you can achieve by using your HSA for qualified medical expenses.

- Investment Growth Simulator: Simulate the potential growth of your HSA investments based on different asset allocation strategies.

8.3. Real-World Examples

To further illustrate the benefits of an HSA, consider the following scenarios:

- Scenario 1: Young Professional: Sarah, a 28-year-old marketing professional, uses her HSA to pay for routine doctor visits, prescription medications, and vision care. By contributing regularly and using her HSA for qualified medical expenses, she reduces her taxable income and saves money on healthcare costs.

- Scenario 2: Family with Children: The Johnson family uses their HSA to cover copays, deductibles, and other medical expenses for their two children. They also invest a portion of their HSA funds, allowing their savings to grow tax-free for future healthcare needs.

- Scenario 3: Pre-Retiree: John, a 62-year-old accountant, uses his HSA to pay for long-term care insurance premiums and other qualified medical expenses. He also benefits from the tax-free growth of his HSA investments, which he plans to use to cover healthcare costs in retirement.

8.4. Tax Benefits Analysis

One of the most significant advantages of an HSA is its triple tax benefit:

- Tax-Deductible Contributions: Contributions to your HSA are tax-deductible, reducing your taxable income.

- Tax-Free Growth: The money in your HSA grows tax-free.

- Tax-Free Withdrawals: Withdrawals for qualified medical expenses are tax-free.

This combination of tax benefits makes the HSA an incredibly powerful tool for saving and paying for healthcare expenses.

According to a study by the National Bureau of Economic Research, families who use HSAs effectively can save thousands of dollars in taxes and healthcare costs over the long term.

8.5. Strategies for Maximizing HSA Benefits

To make the most of your HSA, consider the following strategies:

- Contribute the Maximum Amount: Maximize your annual contributions to take full advantage of the tax benefits.

- Invest Your HSA Funds: Invest a portion of your HSA funds to allow your savings to grow tax-free.

- Pay for Qualified Medical Expenses with Your HSA: Use your HSA to pay for qualified medical expenses to avoid taxes and penalties.

- Keep Detailed Records: Keep detailed records of your HSA contributions, withdrawals, and qualified medical expenses for tax purposes.

- Stay Informed: Stay informed about the latest HSA rules and regulations by consulting with your HR department or HSA administrator.

9. Understanding High-Deductible Health Plans (HDHPs) and HSA Eligibility

To be eligible for an HSA, you must be enrolled in a High-Deductible Health Plan (HDHP). An HDHP typically has a higher deductible than traditional health insurance plans, but it also offers lower monthly premiums.

9.1. HDHP Requirements

The IRS sets specific requirements for HDHPs, including minimum deductible amounts and maximum out-of-pocket expenses.

HDHP Requirements for 2024:

| Category | Individual | Family |

|---|---|---|

| Minimum Deductible | $1,600 | $3,200 |

| Maximum Out-of-Pocket | $8,050 | $16,100 |

These amounts are adjusted annually to account for inflation.

9.2. Comparing HDHPs and Traditional Health Insurance Plans

When deciding whether to enroll in an HDHP, consider the following factors:

- Premiums: HDHPs typically have lower monthly premiums than traditional health insurance plans.

- Deductibles: HDHPs have higher deductibles than traditional health insurance plans.

- Out-of-Pocket Expenses: HDHPs may have lower out-of-pocket expenses than traditional health insurance plans, depending on your healthcare usage.

- HSA Eligibility: Enrolling in an HDHP makes you eligible to contribute to an HSA, which offers significant tax advantages.

9.3. Health Savings Account Contribution Limits 2024

The Health Savings Account (HSA) contribution limits for 2024 are as follows:

- Individual: $4,150

- Family: $8,300

These limits are subject to change annually. Consult with your tax advisor or HSA administrator to confirm the latest contribution limits.

9.4. Catch-Up Contributions

Individuals age 55 and older can make additional “catch-up” contributions to their HSAs.

Catch-Up Contribution Limit for 2024:

- Individuals age 55 and older: $1,000

This additional contribution can help pre-retirees boost their HSA savings and prepare for future healthcare expenses.

9.5. HSA vs. FSA

HSAs are often compared to Flexible Spending Accounts (FSAs), but there are several key differences:

| Feature | HSA | FSA |

|---|---|---|

| Eligibility | Must be enrolled in an HDHP | Offered by employer |

| Contribution Limits | Set annually by the IRS | Set by employer and IRS |

| Rollover | Funds roll over from year to year | Use-it-or-lose-it rule |

| Portability | Account is owned by the individual | Account is owned by the employer |

| Investment Options | May offer investment options | Typically does not offer investments |

Understanding these differences can help you determine whether an HSA or FSA is the right choice for your healthcare savings needs.

10. How to Transfer HSA Funds After Leaving an Employer

If you leave your employer, you can still keep your HSA and transfer it to a new provider or keep it with your current provider.

10.1. Options for Managing Your HSA After Leaving an Employer

- Keep Your HSA with Your Current Provider: You can keep your HSA with your current provider, but you may be subject to fees if you are no longer an employee.

- Transfer Your HSA to a New Provider: You can transfer your HSA to a new provider, such as a bank, credit union, or investment firm.

- Roll Over Your HSA to a New Provider: You can roll over your HSA to a new provider, but you must do so within 60 days of receiving the funds.

10.2. Steps for Transferring Your HSA to a New Provider

- Open a new HSA account with your preferred provider.

- Complete the transfer paperwork provided by your new provider.

- Your new provider will contact your old provider to initiate the transfer.

- Your funds will be transferred to your new HSA account within a few weeks.

10.3. HSA Fees

Be aware of potential fees associated with your HSA, such as:

- Monthly Maintenance Fees: Some providers charge a monthly fee to maintain your HSA.

- Transaction Fees: Some providers charge a fee for each transaction you make with your HSA.

- Investment Fees: If you invest your HSA funds, you may be subject to investment fees.

Compare the fees charged by different providers to ensure you are getting the best value for your money.

10.4. Estate Planning and HSAs

Your HSA can be a valuable asset in your estate plan. You can designate a beneficiary for your HSA, and the funds can be used to pay for their qualified medical expenses after your death.

10.5. Beneficiary Designations

When you open an HSA, you will be asked to designate a beneficiary. If you die, your HSA funds will be transferred to your beneficiary.

10.6. Tax Implications for Beneficiaries

The tax implications for beneficiaries depend on whether they are your spouse or someone else.

- Spouse: If your beneficiary is your spouse, they can roll over your HSA into their own HSA and continue to use the funds for qualified medical expenses.

- Non-Spouse: If your beneficiary is not your spouse, the funds will be distributed to them and subject to income tax.

10.7. Contribution Limit for Those Over 55

For those aged 55 and older, there’s an opportunity to further bolster their health savings through “catch-up” contributions. In 2024, individuals in this age bracket can contribute an additional $1,000 annually, above the standard contribution limits. This provision allows pre-retirees to significantly increase their HSA savings, providing a larger cushion for healthcare expenses during retirement.

11. How Money-Central.com Can Assist You with Your HSA Decisions

Money-central.com is committed to providing you with the tools, resources, and expertise you need to make informed decisions about your HSA and overall financial well-being. Our team of financial experts is dedicated to helping you navigate the complexities of healthcare savings and plan for a secure financial future.

We provide detailed analysis of financial products. We provide guides to help you make financial decisions.

11.1. Personalized Financial Advice

We offer personalized financial advice tailored to your specific needs and goals. Our financial advisors can help you develop a customized HSA strategy, choose the right investments, and plan for retirement.

Address: 44 West Fourth Street, New York, NY 10012, United States.

Phone: +1 (212) 998-0000.

Website: money-central.com.

11.2. Regular Updates and News

We provide regular updates and news on the latest HSA rules, regulations, and investment opportunities. Stay informed about the changing healthcare landscape and make adjustments to your HSA strategy as needed.

Our website is regularly updated with the latest information on HSAs, including changes to contribution limits, eligibility requirements, and investment options.

12. Frequently Asked Questions (FAQs) About HSA Withdrawals

Q1: Can I use my HSA to pay for my spouse’s medical expenses?

Yes, you can use your HSA to pay for the qualified medical expenses of your spouse, even if they are not covered by your health insurance plan.

Q2: What happens if I withdraw money from my HSA for non-qualified expenses before age 65?

If you withdraw money from your HSA for non-qualified expenses before age 65, you will be subject to income tax and a 20% penalty on the withdrawn amount.

Q3: Can I invest my HSA funds?

Yes, many HSA providers offer investment options, such as stocks, bonds, and mutual funds. Investing your HSA funds can allow your savings to grow tax-free.

Q4: What happens to my HSA when I turn 65?

When you turn 65, you can continue to use your HSA for qualified medical expenses tax-free. You can also withdraw money for non-qualified expenses, but you will be subject to income tax.

Q5: Can I transfer my HSA to a new provider?

Yes, you can transfer your HSA to a new provider. You can either transfer the funds directly or roll them over within 60 days.

Q6: What are the benefits of having an HSA?

The benefits of having an HSA include tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

Q7: What is a High-Deductible Health Plan (HDHP)?

A High-Deductible Health Plan (HDHP) is a health insurance plan with a higher deductible than traditional health insurance plans. Enrolling in an HDHP makes you eligible to contribute to an HSA.

Q8: Can I use my HSA to pay for long-term care insurance premiums?

Yes, you can use your HSA to pay for long-term care insurance premiums, subject to certain limitations.

Q9: What happens to my HSA if I die?

If you die, your HSA funds will be transferred to your beneficiary. The tax implications for beneficiaries depend on whether they are your spouse or someone else.

Q10: How can I find a qualified financial advisor to help me with my HSA decisions?

Money-central.com can connect you with qualified financial advisors who can help you develop a customized HSA strategy and plan for your financial future.

By understanding the intricacies of HSA withdrawals and leveraging the resources available at money-central.com, you can effectively manage your healthcare finances, maximize your savings, and achieve your financial goals.

Ready to take control of your healthcare finances? Explore our articles, use our tools, and connect with our financial advisors at money-central.com to start maximizing the benefits of your HSA today.