A Contraction Of The Money Supply refers to a decrease in the total amount of money circulating in an economy, which can influence financial stability, investment strategies, and overall economic health. At money-central.com, we break down complex financial topics to help you make informed decisions about your money. Understanding monetary policy and its impact is crucial for navigating the financial landscape successfully, as it directly affects interest rates, inflation, and economic growth.

1. What Exactly Is a Contraction of the Money Supply?

A contraction of the money supply means there is a reduction in the total amount of currency and other liquid instruments in a nation’s economy. This can lead to decreased spending, investment, and overall economic slowdown.

To expand, a contraction of the money supply is a significant economic event that occurs when the total amount of money circulating within an economy decreases. This phenomenon can arise from various factors, often linked to central bank policies, changes in commercial lending, or shifts in consumer and business behavior. A shrinking money supply typically leads to reduced spending and investment, impacting economic growth and potentially causing deflationary pressures. It’s a critical concept to understand for anyone looking to navigate the financial landscape effectively.

1.1 How is Money Supply Defined?

Money supply is defined as the total amount of money available in an economy at a specific time. It includes cash, checking accounts, and other liquid assets.

Money supply is a comprehensive measure that includes all the currency and other liquid assets in a country’s economy on a specific date. This includes physical currency (coins and banknotes), demand deposits in commercial banks (checking accounts), and other liquid assets that can be easily converted into cash. Central banks, like the Federal Reserve in the United States, use different measures to track the money supply, such as M1 and M2, which include various types of accounts and assets.

1.2 What Causes a Contraction in the Money Supply?

Several factors can cause a contraction in the money supply, including central bank policies, reduced commercial lending, and decreased consumer spending.

- Central Bank Policies: Central banks can reduce the money supply by increasing interest rates, selling government bonds, or increasing reserve requirements for banks. These actions decrease the amount of money available for lending and investment.

- Reduced Commercial Lending: If banks become more risk-averse or face tighter capital requirements, they may reduce lending, decreasing the amount of money circulating in the economy.

- Decreased Consumer Spending: A drop in consumer confidence or economic uncertainty can lead to decreased spending, reducing the demand for credit and money.

- Increased Savings Rate: Higher savings rates mean less money is being circulated, as more funds are being held rather than spent or invested.

1.3 What are the Different Measures of Money Supply?

The most common measures of money supply are M1 and M2, each including different types of liquid assets. M1 includes the most liquid forms of money, while M2 includes M1 plus savings accounts and other less liquid assets.

- M1: This measure includes the most liquid forms of money, such as physical currency (coins and banknotes in circulation) and demand deposits (checking accounts). M1 represents the money that is readily available for transactions.

- M2: This measure includes M1 plus savings accounts, money market accounts, and small-denomination time deposits (certificates of deposit or CDs). M2 includes money that is slightly less liquid than M1 but can be easily converted into cash.

- M3: A broader measure that includes M2 plus large-denomination time deposits, institutional money market funds, short-term repurchase agreements, and other larger liquid assets. M3 is less commonly tracked but provides a more comprehensive view of the money supply.

- M0: The monetary base, which is the total currency in circulation outside of Federal Reserve Banks and the U.S. Treasury, plus commercial banks’ reserves held at the Fed.

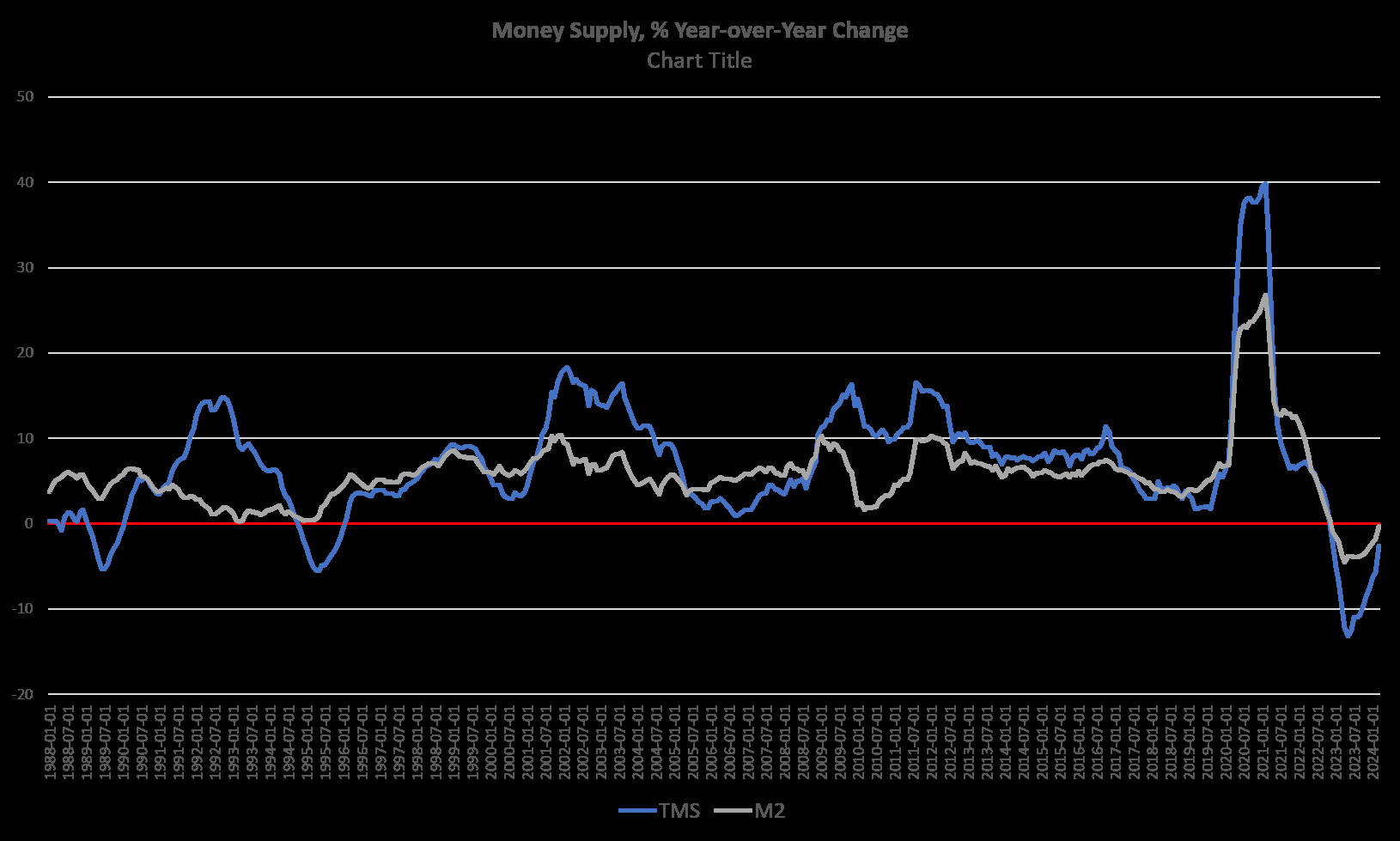

M1 and M2

M1 and M2

2. What Is The Impact of a Contraction of the Money Supply on the Economy?

A contraction of the money supply can have several significant impacts on the economy, including decreased economic activity, deflationary pressures, and increased borrowing costs.

For example, according to research from New York University’s Stern School of Business, in July 2025, a persistent contraction in the money supply may lead to a recession, as businesses and consumers reduce spending due to decreased access to credit.

2.1 Decreased Economic Activity

A contraction of the money supply typically leads to decreased economic activity as businesses and consumers have less access to capital. This can result in reduced investment, hiring, and overall economic growth.

When there is less money circulating in the economy, businesses may find it harder to secure loans for expansion or working capital, and consumers may reduce their spending due to decreased purchasing power. This slowdown can create a ripple effect, leading to lower production, job losses, and reduced demand for goods and services. The impact is particularly pronounced in sectors that rely heavily on credit, such as real estate and manufacturing.

2.2 Deflationary Pressures

A contraction of the money supply can create deflationary pressures, causing prices to fall as demand decreases. While deflation may seem beneficial, it can lead to decreased corporate earnings, wage stagnation, and increased debt burdens.

Deflation occurs when the general price level in an economy falls, meaning that the purchasing power of money increases. While lower prices might sound appealing, deflation can discourage spending and investment. Consumers may delay purchases in anticipation of even lower prices, leading to a decrease in demand. Businesses may respond by cutting production and wages, which can further depress economic activity.

2.3 Increased Borrowing Costs

A contraction of the money supply can lead to increased borrowing costs as banks tighten lending standards and reduce the availability of credit. This can make it more expensive for businesses and consumers to borrow money, further dampening economic activity.

When the money supply contracts, banks may become more cautious about lending, leading to higher interest rates and stricter loan requirements. This can make it more difficult for businesses to finance investments or operations, and for consumers to afford mortgages, car loans, and other forms of credit. The increased cost of borrowing can slow down economic growth and reduce overall spending.

2.4 Impact on Employment

A contraction of the money supply can negatively impact employment rates. As businesses face tighter financial conditions, they may reduce their workforce, leading to higher unemployment.

When businesses struggle to access credit and experience reduced demand, they may be forced to cut costs to stay afloat. Layoffs become a common response, leading to an increase in unemployment rates. This can create a vicious cycle, as higher unemployment further reduces consumer spending, exacerbating the economic slowdown.

2.5 Effect on Investment

A contraction of the money supply can discourage investment as investors become more risk-averse and capital becomes more expensive. This can slow down innovation and long-term economic growth.

With less money available and higher borrowing costs, businesses may postpone or cancel investment projects. Investors may also shift towards safer assets, such as government bonds, reducing the flow of capital to more productive sectors. This decline in investment can have long-term consequences, as it can hinder technological advancements and limit future economic potential.

3. Historical Examples of Money Supply Contraction

Several historical periods have seen significant contractions in the money supply, each with its own unique causes and consequences. These events provide valuable lessons for understanding the potential impact of monetary policy on the economy.

3.1 The Great Depression

The Great Depression of the 1930s was marked by a severe contraction of the money supply. This contraction exacerbated the economic downturn, leading to widespread bank failures, unemployment, and deflation.

During the Great Depression, the money supply in the United States contracted by about 30% between 1929 and 1933. This contraction was largely due to bank failures and a decrease in lending. As banks failed, people lost their savings, and the remaining banks became hesitant to lend, leading to a sharp decline in economic activity.

3.2 The Early 1980s Recession

The early 1980s recession was triggered by the Federal Reserve’s efforts to combat inflation by tightening monetary policy. This led to a contraction in the money supply and a sharp increase in interest rates.

In the late 1970s, the United States experienced high inflation rates. To combat this, the Federal Reserve, under Chairman Paul Volcker, implemented a tight monetary policy, which led to a significant contraction in the money supply. Interest rates soared, peaking at around 20%, which curbed inflation but also triggered a recession.

3.3 The 2008 Financial Crisis

The 2008 financial crisis saw a temporary contraction in the money supply as credit markets froze and banks became reluctant to lend. Although central banks responded with aggressive monetary easing, the initial contraction contributed to the severity of the crisis.

During the 2008 financial crisis, the collapse of Lehman Brothers and other financial institutions led to a freeze in credit markets. Banks became hesitant to lend to each other and to businesses, leading to a contraction in the money supply. Central banks around the world responded by injecting liquidity into the markets and lowering interest rates to stimulate lending.

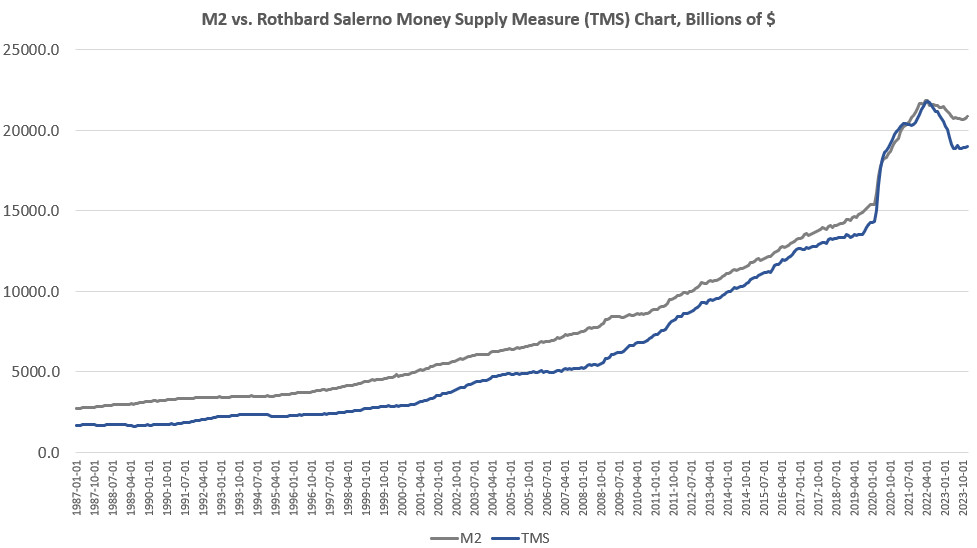

Total Money Supply

Total Money Supply

4. How is a Contraction of the Money Supply Different from Quantitative Tightening?

A contraction of the money supply and quantitative tightening (QT) are related but distinct concepts. Both involve reducing the amount of money circulating in the economy, but they operate through different mechanisms and contexts.

4.1 Definition of Quantitative Tightening (QT)

Quantitative Tightening (QT) involves a central bank reducing its balance sheet by selling assets or allowing them to mature without reinvestment. This directly reduces the reserves available to commercial banks.

Quantitative Tightening (QT) is a monetary policy tool used by central banks to decrease the money supply and reduce the level of liquidity in the economy. It is often implemented after a period of quantitative easing (QE), where the central bank increases the money supply by purchasing assets.

4.2 How QT Works

When a central bank engages in QT, it typically does so by selling government bonds or other assets it has accumulated during QE. Alternatively, it may choose not to reinvest the proceeds from maturing assets, allowing them to roll off the balance sheet.

When the central bank sells assets, it removes reserves from the banking system. Banks that purchase these assets must pay the central bank, reducing their reserve balances. Similarly, when assets mature without reinvestment, the central bank receives payment without injecting new reserves back into the system.

4.3 The Relationship Between QT and Contraction of the Money Supply

QT directly contributes to a contraction of the money supply by reducing the reserves available to commercial banks. As reserves decrease, banks may reduce lending, leading to less money circulating in the economy.

QT is one mechanism that can lead to a contraction of the money supply. While a contraction of the money supply can occur due to various factors (such as decreased lending or increased savings rates), QT is a deliberate policy action by the central bank to achieve this outcome.

4.4 Key Differences Between QT and a General Contraction

The primary difference lies in the mechanism and intent. QT is a specific policy tool used by central banks to reduce their balance sheet and decrease reserves, while a general contraction of the money supply can result from various market dynamics and behaviors.

- Mechanism: QT involves the central bank actively reducing its asset holdings, whereas a general contraction can occur due to factors like reduced lending or increased savings.

- Intent: QT is a deliberate policy aimed at tightening monetary conditions, while a general contraction may be an unintended consequence of other economic forces.

- Control: The central bank has direct control over QT, whereas it has less direct control over other factors that can cause a contraction of the money supply.

5. What are the Potential Benefits of a Money Supply Contraction?

While a contraction of the money supply is often viewed negatively, it can have some potential benefits, particularly in controlling inflation and promoting financial stability.

5.1 Controlling Inflation

One of the primary benefits of a contraction of the money supply is its potential to control inflation. By reducing the amount of money circulating in the economy, central banks can curb excessive spending and demand, which can help to stabilize prices.

When there is too much money chasing too few goods and services, inflation can occur. A contraction of the money supply can help to bring the supply of money in line with the economy’s productive capacity, reducing inflationary pressures.

5.2 Promoting Financial Stability

A contraction of the money supply can also promote financial stability by reducing speculative activities and preventing asset bubbles. By making credit less available, central banks can discourage excessive risk-taking and promote more sustainable economic growth.

When money is easily available, it can fuel speculative investments and asset bubbles, which can lead to financial crises. A contraction of the money supply can help to cool down these speculative activities and promote a more stable financial system.

5.3 Encouraging Savings

Higher interest rates, which often accompany a contraction of the money supply, can encourage people to save more. Increased savings can provide a buffer against economic shocks and promote long-term financial security.

When interest rates rise, the incentive to save increases, as people can earn more on their savings. This can lead to a higher savings rate, which can provide a stable source of funds for investment and economic growth.

5.4 Reducing Government Debt

By controlling inflation and promoting fiscal discipline, a contraction of the money supply can indirectly help to reduce government debt. Lower inflation can reduce the need for government spending on inflation-indexed programs, while fiscal discipline can help to balance the budget.

When inflation is under control, governments may be able to reduce their borrowing costs and stabilize their debt levels. This can free up resources for other priorities, such as infrastructure and education.

6. What are the Risks of a Contraction of the Money Supply?

Despite the potential benefits, a contraction of the money supply also carries significant risks, including recession, deflation, and financial instability.

6.1 Risk of Recession

One of the most significant risks of a contraction of the money supply is the potential to trigger a recession. By reducing access to credit and dampening economic activity, a contraction can lead to a sharp decline in economic growth and employment.

If the money supply contracts too quickly or too sharply, it can lead to a credit crunch, where businesses and consumers struggle to access the funds they need to operate. This can lead to a decrease in investment, hiring, and overall economic activity, potentially triggering a recession.

6.2 Deflationary Spiral

A contraction of the money supply can also lead to a deflationary spiral, where falling prices lead to decreased spending, production cuts, and further price declines. This can create a vicious cycle that is difficult to break.

Deflation can discourage spending, as consumers may delay purchases in anticipation of even lower prices. This can lead to a decrease in demand, which can force businesses to cut production and lower wages. This can further depress economic activity and exacerbate the deflationary pressures.

6.3 Increased Debt Burden

Deflation, which can result from a contraction of the money supply, can increase the real burden of debt. As prices fall, the real value of debt increases, making it more difficult for borrowers to repay their obligations.

When deflation occurs, borrowers must repay their debts with money that is worth more than the money they borrowed. This can lead to financial distress and defaults, which can destabilize the financial system.

6.4 Financial Instability

A contraction of the money supply can also contribute to financial instability by increasing the risk of bank failures and credit market disruptions. Tighter financial conditions can expose vulnerabilities in the financial system and lead to a loss of confidence.

If banks and other financial institutions face tighter financial conditions, they may become more risk-averse and reduce lending. This can lead to a credit crunch, which can destabilize the financial system and increase the risk of bank failures.

7. How Can Individuals and Businesses Prepare for a Contraction?

Preparing for a contraction of the money supply involves taking steps to protect your finances, reduce debt, and increase liquidity.

7.1 Managing Personal Finances

Individuals can manage their finances by creating a budget, reducing unnecessary expenses, and building an emergency fund. These steps can help to cushion the impact of an economic downturn.

- Create a Budget: Track your income and expenses to identify areas where you can cut back.

- Reduce Debt: Pay down high-interest debt, such as credit card balances, to reduce your financial burden.

- Build an Emergency Fund: Save at least three to six months’ worth of living expenses to cover unexpected costs.

- Diversify Income: Explore additional income streams to increase your financial security.

7.2 Business Strategies

Businesses can prepare for a contraction by managing their cash flow, reducing debt, and diversifying their customer base. These strategies can help to weather the storm and emerge stronger.

- Manage Cash Flow: Monitor your cash flow closely and take steps to improve it, such as reducing inventory and shortening payment terms.

- Reduce Debt: Pay down debt to reduce your financial risk and improve your credit rating.

- Diversify Customers: Expand your customer base to reduce your reliance on any single customer or market.

- Improve Efficiency: Streamline your operations and reduce costs to improve your profitability.

7.3 Investment Strategies

Investors can prepare for a contraction by diversifying their portfolios, investing in defensive assets, and staying informed about market conditions. These strategies can help to protect their investments and generate returns.

- Diversification: Spread your investments across different asset classes, such as stocks, bonds, and real estate, to reduce your risk.

- Defensive Assets: Invest in defensive assets, such as government bonds and dividend-paying stocks, which tend to hold up better during economic downturns.

- Stay Informed: Keep up with market news and economic developments to make informed investment decisions.

- Long-Term Perspective: Maintain a long-term investment perspective and avoid making impulsive decisions based on short-term market fluctuations.

7.4 Seeking Financial Advice

Consider consulting with a financial advisor who can provide personalized guidance and help you develop a strategy that is tailored to your specific needs and goals.

A financial advisor can assess your financial situation, help you create a budget, develop an investment strategy, and provide ongoing support and advice. They can also help you navigate complex financial issues and make informed decisions.

8. What Is The Role of Central Banks in Managing Money Supply?

Central banks play a crucial role in managing the money supply to promote economic stability and achieve their policy objectives. They use a variety of tools to influence the amount of money circulating in the economy.

8.1 Monetary Policy Tools

Central banks use several monetary policy tools to manage the money supply, including interest rates, reserve requirements, and open market operations.

- Interest Rates: Central banks can influence the money supply by adjusting the interest rates they charge to commercial banks. Lowering interest rates encourages banks to borrow more money, increasing the money supply. Raising interest rates has the opposite effect.

- Reserve Requirements: Central banks can also influence the money supply by setting reserve requirements for commercial banks. These requirements specify the percentage of deposits that banks must hold in reserve. Lowering reserve requirements allows banks to lend out more money, increasing the money supply.

- Open Market Operations: Central banks use open market operations to buy or sell government bonds in the open market. Buying bonds injects money into the economy, increasing the money supply. Selling bonds withdraws money from the economy, decreasing the money supply.

8.2 Inflation Targeting

Many central banks today use inflation targeting as their primary monetary policy objective. This involves setting a specific inflation target and using monetary policy tools to achieve that target.

Inflation targeting helps to anchor inflation expectations and promote price stability. By clearly communicating their inflation target, central banks can influence the behavior of businesses and consumers and reduce the risk of inflation surprises.

8.3 Lender of Last Resort

Central banks also serve as the lender of last resort, providing emergency lending to commercial banks during times of financial crisis. This helps to prevent bank runs and maintain stability in the financial system.

During a financial crisis, commercial banks may face liquidity problems and struggle to meet their obligations. The central bank can step in and provide emergency loans to these banks, helping to prevent a collapse of the financial system.

8.4 Communication and Transparency

Effective communication and transparency are essential for central banks to manage the money supply effectively. By clearly communicating their policy objectives and decisions, central banks can influence market expectations and promote confidence in the economy.

Central banks often publish regular reports and forecasts to provide information about their views on the economy and their policy intentions. They also hold press conferences and give speeches to communicate directly with the public and the media.

9. Current Trends in Money Supply Growth

Understanding current trends in money supply growth is crucial for assessing the health of the economy and anticipating future economic developments.

9.1 Recent Data on Money Supply

Recent data on money supply growth can provide insights into the current state of the economy. Monitoring measures such as M1 and M2 can help to identify trends and potential risks.

For example, if M2 growth is slowing, it could be a sign that economic activity is cooling down. Conversely, if M2 growth is accelerating, it could be a sign that the economy is overheating.

9.2 Factors Influencing Money Supply

Several factors can influence money supply growth, including central bank policies, government spending, and global economic conditions.

- Central Bank Policies: Changes in interest rates, reserve requirements, and open market operations can all affect the money supply.

- Government Spending: Government spending can inject money into the economy, increasing the money supply.

- Global Economic Conditions: Global economic conditions can affect the demand for U.S. dollars and the flow of capital into and out of the United States, which can influence the money supply.

9.3 Expert Opinions

Expert opinions on money supply growth can provide valuable insights into the potential implications of current trends.

Economists and financial analysts often offer their views on the likely impact of money supply growth on inflation, economic growth, and financial markets. These opinions can help investors and businesses make informed decisions.

9.4 Predictions and Forecasts

Predictions and forecasts about future money supply growth can help individuals and businesses prepare for potential economic scenarios.

Central banks, international organizations, and private sector forecasters regularly publish predictions and forecasts about future money supply growth. These forecasts can provide a basis for planning and risk management.

10. FAQ about Contraction of the Money Supply

Understanding the nuances of a contraction of the money supply can be challenging. Here are some frequently asked questions to help clarify the concept.

10.1 What is the primary cause of a money supply contraction?

A primary cause is central banks tightening monetary policy, like raising interest rates or reducing asset purchases.

10.2 How does a contraction affect small businesses?

It can make accessing loans more difficult and increase borrowing costs, potentially slowing growth.

10.3 Can a contraction lead to deflation?

Yes, it can decrease demand, leading to falling prices and potentially deflation.

10.4 What sectors are most affected by a money supply contraction?

Sectors heavily reliant on credit, such as real estate, manufacturing, and construction, are typically most affected.

10.5 How do central banks decide when to contract the money supply?

They consider factors like inflation rates, economic growth, and financial stability.

10.6 What can governments do to mitigate the negative effects of a contraction?

Governments can implement fiscal policies to stimulate demand, such as infrastructure spending or tax cuts.

10.7 Is a money supply contraction always bad for the economy?

Not always; it can help control inflation and prevent asset bubbles, promoting long-term stability.

10.8 How long does a money supply contraction typically last?

The duration varies depending on the severity of the economic issues and the central bank’s policy response.

10.9 What is the difference between M1 and M2 during a contraction?

M1 (liquid assets) may contract more quickly, while M2 (including savings accounts) may contract more slowly.

10.10 How can individuals protect their savings during a money supply contraction?

Consider diversifying investments and focusing on less risky assets.

Understanding the contraction of the money supply is vital for making informed financial decisions. At money-central.com, we provide comprehensive, easy-to-understand resources to help you navigate the complexities of personal finance.

Are you ready to take control of your financial future? Visit money-central.com today for more articles, tools, and expert advice tailored to the U.S. market. Our team is dedicated to providing you with the insights and resources you need to achieve your financial goals.