Are you feeling lost in the maze of financial decisions? Wondering whether to invest, pay down debt, save for college, or tackle another pressing money matter? You’re not alone. Many people struggle with prioritizing their financial goals. The Money Guy Financial Order Of Operations is your comprehensive roadmap to financial clarity. This powerful 9-step system provides a clear path to manage your money effectively, ensuring every dollar works towards building your secure financial future.

This framework, championed by the Money Guy Show, acts like a financial instruction manual. Just as PEMDAS guides you through mathematical equations, the Financial Order of Operations (FOO) brings order to your financial life. Whether you’re starting your first job, grappling with debt, or seeking advanced investment strategies, FOO provides a step-by-step approach to financial well-being.

Studies reveal a concerning financial fragility among Americans, with a significant portion unable to handle even a modest unexpected expense. This highlights the urgent need for a structured financial approach. The Money Guy Financial Order of Operations offers that structure, providing a clear and actionable path to navigate financial complexities and build lasting wealth.

Screenshot 2024 02 02 at 10.40.30 AM

Screenshot 2024 02 02 at 10.40.30 AM

Unpacking the Money Guy Financial Order of Operations (FOO)

The Money Guy Financial Order of Operations (FOO) isn’t just a theory; it’s a practical, field-tested system. Born from years of financial expertise at the Money Guy Show, FOO has become a cornerstone of their financial philosophy. The core principles were first introduced in a YouTube video in 2017 and have since evolved into a robust, adaptable strategy for anyone seeking financial success.

The beauty of the 9-step FOO lies in its universality. It’s not a one-size-fits-all approach but rather a flexible framework applicable across diverse financial situations and life stages. Whether you’re just starting out, facing significant debt, or managing substantial wealth, FOO provides a relevant and effective pathway to financial prosperity. It’s designed to be an “all-weather” plan, adapting to your changing circumstances and ensuring you’re always moving in the right financial direction.

The 5 Cornerstones of the Money Guy Financial Philosophy: Ground Rules for FOO Success

Before diving into the 9 steps, it’s crucial to understand the five fundamental ground rules underpinning the Money Guy approach to wealth building. These principles are not just suggestions; they are essential for maximizing the effectiveness of the Financial Order of Operations and achieving long-term financial success. Think of them as the foundation upon which your financial house will be built.

Ground Rule #1: Generosity: Step Zero, Not Just a Step

Generosity isn’t relegated to a single step within FOO; it’s the foundational Step Zero. Giving back, whether through financial contributions, volunteering time, or sharing skills, is a core value. Even with limited financial resources, everyone can practice generosity in meaningful ways, contributing to a better world while fostering a mindset of abundance.

Ground Rule #2: The 25% Investment Target: A Challenging but Achievable Goal

Aiming to invest 25% of your gross income might seem daunting, but it’s a cornerstone of long-term wealth building. The Money Guy team acknowledges this isn’t easy, but emphasizes its crucial role in securing a comfortable retirement. They provide the tools and knowledge to gradually reach this goal, encouraging persistence and highlighting the transformative impact of consistent, significant investing.

Ground Rule #3: Debt as a Four-Letter Word: Handle with Extreme Caution

Debt, particularly high-interest debt, is viewed as a major financial obstacle. The Money Guy philosophy advocates for cautious and responsible debt management. Understanding the risks and implementing strategies to minimize and eliminate harmful debt are crucial steps towards financial freedom. Learning to use debt strategically, rather than letting it control you, is key.

Ground Rule #4: Passion and Purpose in Your Profession: A Catalyst for Financial Well-being

Job satisfaction significantly impacts overall well-being, including financial health. Finding work that aligns with your passions and provides a sense of purpose can make the journey towards financial independence more enjoyable and sustainable. When you enjoy what you do, work becomes less of a burden and more of a fulfilling part of life.

Ground Rule #5: Life is Finite: Enjoy the Journey, Not Just the Destination

While financial responsibility is paramount, the Money Guy approach emphasizes balance. Life is to be lived and enjoyed at every stage. Becoming overly frugal to the point of sacrificing present joy for future security misses the point. Finding a healthy balance between saving for the future and enjoying the present is essential for a fulfilling life.

Essential FOO Resources from The Money Guy

To help you navigate the Financial Order of Operations, the Money Guy team has developed a range of valuable resources. These tools are designed to provide further guidance and support as you implement FOO in your own financial journey.

- Millionaire Mission Book: Brian Preston’s book, “Millionaire Mission,” provides an in-depth exploration of the 9 steps, offering practical advice and strategies.

- FOO Course: For a more structured learning experience, the FOO course offers video lessons, homework assignments, live streams, and a community forum to deepen your understanding and implementation of the system.

- Money Guy Website and Podcast: The Money Guy website and podcast are treasure troves of financial information, consistently providing valuable insights and advice aligned with the FOO principles.

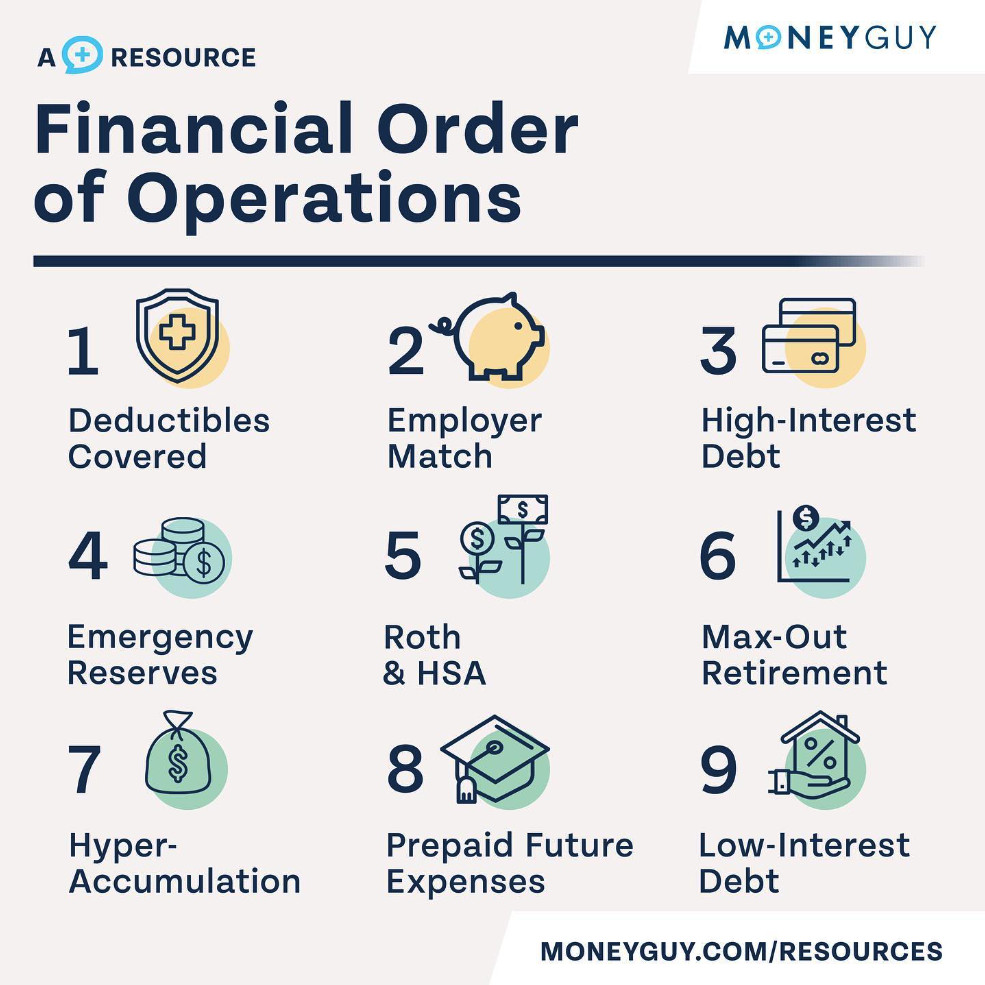

A Deep Dive into the 9 Steps of the Money Guy Financial Order of Operations

The Financial Order of Operations is structured as nine sequential steps, each building upon the previous one to create a robust financial foundation. Progressing through these steps in order ensures that you address the most critical financial needs first, systematically building wealth and security. Let’s explore each step in detail:

Step 1: Deductibles Covered

Jump back to the 9 Steps list

People walking in the rain, illustrating the importance of saving money for a rainy day.

People walking in the rain, illustrating the importance of saving money for a rainy day.

Saving for insurance deductibles is the crucial first step in the Financial Order of Operations, ensuring financial protection against unexpected events.

Step one focuses on safeguarding your finances from unexpected setbacks by covering your insurance deductibles. Life is unpredictable, and having readily available funds to cover deductibles for health, auto, or home insurance is crucial. This step acts as your initial financial safety net.

Key Considerations for Step 1:

- Focus on the Highest Deductible: You only need to save enough to cover your highest insurance deductible initially.

- Understanding Deductibles: A deductible is the amount you pay out-of-pocket before your insurance coverage kicks in.

- Balancing Premiums and Deductibles: While lower deductibles mean quicker insurance payouts, they typically come with higher premiums. FOO prioritizes having the deductible readily available over necessarily choosing the lowest deductible.

- Completion of Step 1: Step 1 is complete when you have liquid savings equal to your highest insurance deductible. Review your insurance policies to determine your deductible amounts.

See Also: Money Guy’s Comprehensive Guide to 16 Types of Insurance

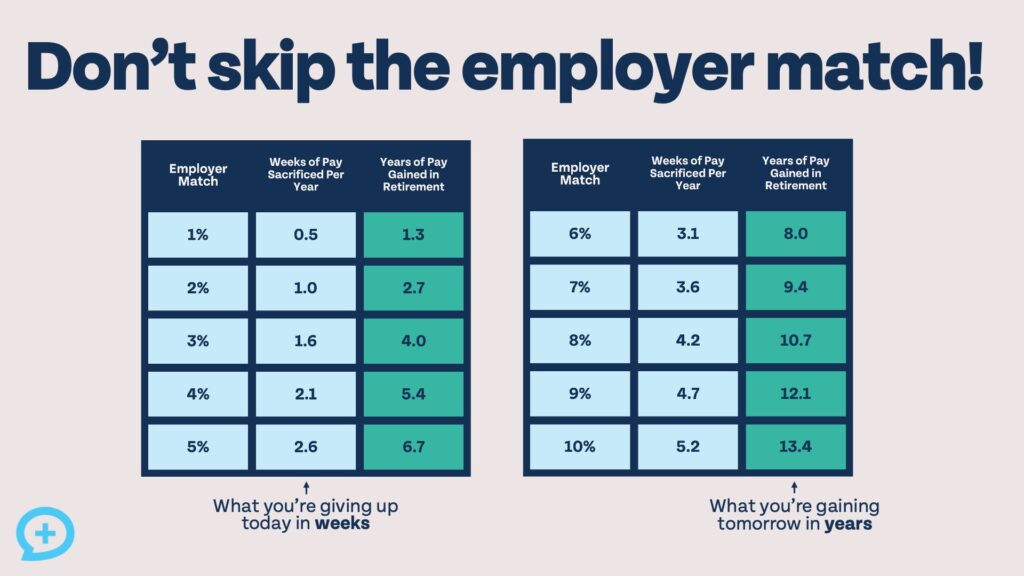

Step 2: Employer Match Maximization

Step two emphasizes capturing “free money” by maximizing your employer’s retirement plan match. Contributing enough to your 401(k) or other employer-sponsored plan to receive the full company match is a high-priority step, often offering a guaranteed return that surpasses even high-interest debt.

Key Considerations for Step 2:

- Prioritizing Employer Match: Even before tackling high-interest debt, securing your employer match is prioritized due to the potentially high return on investment (often 50% or 100%).

- No Employer Match? If your employer doesn’t offer a match, simply move to step three.

- Opportunity Cost of Missing the Match: Failing to capture the employer match is akin to leaving significant money on the table. The long-term benefits of the match far outweigh short-term gains from skipping it.

Financial Order of Operations Infographic with side-by-side tables showing the impact of different rates of employer match.

Financial Order of Operations Infographic with side-by-side tables showing the impact of different rates of employer match.

An employer match significantly boosts your retirement savings, providing substantial long-term financial gains.

- Employee Stock Purchase Plans (ESPPs): Participating in ESPPs can contribute towards maximizing your employer match, but compare the discount rate to high-interest debt rates if applicable.

- Vesting Schedules: Be aware of vesting periods for employer matching funds. You may need to remain employed for a certain period to fully own the matched funds.

- Completion of Step 2: Step 2 is complete when you are contributing enough to your employer-sponsored retirement account to receive the maximum possible employer match.

Step 3: High-Interest Debt Elimination

Jump back to the 9 Steps list

Photo of credit cards on a desk. To build wealth using the FOO system, be sure to tackle high-interest and revolving credit early on.

Photo of credit cards on a desk. To build wealth using the FOO system, be sure to tackle high-interest and revolving credit early on.

Tackling high-interest debt, such as credit cards, is a critical step in the FOO to free up resources for wealth building.

Step three focuses on aggressively eliminating high-interest debt. Credit cards, payday loans, and other high-rate debts erode wealth and hinder financial progress. Prioritizing their payoff frees up cash flow for investing and wealth building.

Key Considerations for Step 3:

- Defining High-Interest Debt: This primarily includes consumer debt like credit cards, car loans (especially those violating the 20/3/8 rule), and potentially some student loans depending on interest rates and individual circumstances.

- Mortgage Debt: While mortgage rates may be rising, they are generally considered lower-interest debt due to the appreciating nature of homes and potential tax deductibility of interest.

- 0% APR Credit Cards: Despite the temporary 0% rate, these are still considered high-interest debt due to the teaser nature and potential for extremely high rates after the promotional period. Treat them as high-priority debt.

- Debt Payoff Strategies: Choose between the debt avalanche (prioritizing highest interest rates) or debt snowball (prioritizing smallest balances) method based on your motivation and financial personality.

- Completion of Step 3: Step 3 is complete when you are entirely free of high-interest debt.

Step 4: Emergency Fund Establishment

Jump back to the 9 Steps list

Photo of person dropping a coin in a piggy bank – This person is following step 4 of the Financial Oder of Operation – Saving for Emergencies

Photo of person dropping a coin in a piggy bank – This person is following step 4 of the Financial Oder of Operation – Saving for Emergencies

Building a robust emergency fund provides a financial cushion to handle life’s unexpected events without derailing your financial progress.

Step four emphasizes building a robust emergency fund to cover 3-6 months of living expenses. This financial cushion protects against job loss, unexpected medical bills, or other emergencies, preventing you from derailing your financial progress when life throws curveballs.

Key Considerations for Step 4:

- Deductible Fund Integration: Your deductible covered fund (Step 1) becomes part of your emergency fund. It’s not a separate entity.

- Expense-Based Calculation: Calculate your emergency fund goal based on your monthly expenses, not your income.

- High-Yield Savings Account (HYSA): Utilize a HYSA for your emergency fund to maximize interest earnings while maintaining liquidity. Online banks often offer more competitive rates than traditional brick-and-mortar banks.

- Emergency Fund Size: The standard recommendation is 3-6 months of expenses, but consider a larger fund if you have variable income, are self-employed, or are in a specialized field with potentially longer job search times.

- Completion of Step 4: Step 4 is complete when you have accumulated your target emergency fund in a readily accessible, high-yield savings account.

Step 5: Roth IRA and HSA Maximization

Jump back to the 9 Steps list

Woman holding a jar of dollar bills she

Woman holding a jar of dollar bills she

Maximizing Roth IRAs and HSAs unlocks powerful tax advantages for long-term wealth accumulation.

Step five focuses on leveraging tax-advantaged accounts by maximizing contributions to Roth IRAs and Health Savings Accounts (HSAs). These accounts offer significant tax benefits, either in retirement (Roth IRA) or for healthcare expenses (HSA), making them powerful tools for wealth building.

Key Considerations for Step 5:

- Roth IRA Benefits: Roth IRAs offer tax-free growth and tax-free withdrawals in retirement, making them highly advantageous for long-term savers.

- HSA Triple Tax Advantage: HSAs offer a unique triple tax benefit: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

- Backdoor Roth IRA: If your income exceeds Roth IRA contribution limits, explore the backdoor Roth IRA strategy to still access these tax advantages. Be mindful of potential tax implications and consider consulting a financial professional.

- HSA Strategic Usage: While HSAs can be used for current medical expenses, maximizing their benefit involves investing the funds and reimbursing yourself for past medical expenses in the future, allowing for tax-free growth over time.

- HSA in Retirement: Even if you don’t anticipate significant future medical expenses, HSA funds can be withdrawn in retirement like a traditional IRA (taxed as ordinary income).

- Completion of Step 5: Step 5 is complete when you are maximizing your annual contributions to both your Roth IRA and HSA (if eligible for an HSA). If you are not eligible for either, skip to step six.

Step 6: Employer Plan Maximization

Jump back to the 9 Steps list

Photo of Asian couple saving money in a jar – Maxing out your employer

Photo of Asian couple saving money in a jar – Maxing out your employer

Fully maximizing employer-sponsored retirement plans, like 401(k)s, is a crucial step towards building substantial retirement savings.

Step six builds upon retirement savings by maximizing contributions to employer-sponsored retirement plans, such as 401(k)s, 403(b)s, and 457 plans. These plans offer tax-deferred growth and are often a convenient way to save through payroll deductions.

Key Considerations for Step 6:

- Contribution Limits: Be aware of annual contribution limits for employer-sponsored plans, which can change annually.

- Early Retirement Considerations: If planning for early retirement, be mindful that funds in employer-sponsored plans may have age-based withdrawal restrictions. Taxable brokerage accounts (Step 7) can offer more flexibility for early withdrawals.

- Mega Backdoor Roth: Explore the mega backdoor Roth strategy if your plan allows after-tax contributions and in-service conversions, potentially allowing for even greater tax-advantaged retirement savings.

- Suboptimal Investment Options: Even if your employer plan has limited or less-than-ideal investment options, the tax advantages generally outweigh the drawbacks. Remember, you can typically roll over funds to an IRA when you leave employment.

- Completion of Step 6: Step 6 is complete when you are contributing the maximum allowable amount to your employer-sponsored retirement plan or when you reach a 25% total investment rate (including steps 2, 5, and 6) – whichever comes first. For those with lower incomes, reaching the 25% investment rate might occur before maxing out employer plans.

Step 7: Hyper-accumulation (25%+ Investing)

Jump back to the 9 Steps list

Person holding hundreds of large denomination bills because they have made it to the hyperaccumulation stage of Money Guy

Person holding hundreds of large denomination bills because they have made it to the hyperaccumulation stage of Money Guy

Reaching the hyper-accumulation phase, investing 25% or more of your income, accelerates your journey to financial independence.

Step seven signifies reaching hyper-accumulation, where you are investing 25% or more of your gross income for retirement. This aggressive savings rate dramatically accelerates wealth accumulation and moves you closer to financial independence.

Key Considerations for Step 7:

- Investing Beyond Employer Plans: Hyper-accumulation may involve utilizing taxable brokerage accounts in addition to maxing out employer-sponsored and tax-advantaged accounts.

- Prioritizing Retirement over College Savings: FOO prioritizes securing your own retirement before fully funding children’s college. This “oxygen mask” principle ensures you won’t become a financial burden on your children later in life. Various college funding options exist, but retirement funding is solely your responsibility.

- Taxable Brokerage Account Role: Taxable brokerage accounts offer flexibility and accessibility, particularly for early retirement goals, as there are no age-based withdrawal restrictions.

- Determining “Enough” Savings: Completing Step 7 involves not just reaching the 25% savings rate but also ensuring that this rate is sufficient to meet your specific retirement goals, considering your age, desired retirement age, and lifestyle expectations.

- Completion of Step 7: Step 7 is complete when you are consistently investing 25% or more of your income and are confident that you are on track to meet your retirement goals. You can potentially complete steps 6 and 7 concurrently if you reach the 25% investment rate before maxing out all employer plans.

Step 8: Pre-pay Future Expenses

Jump back to the 9 Steps list

Photo of college bound female student putting money away to pay for college expenses – Saving for big future expenses is Step 8 of Money Guy

Photo of college bound female student putting money away to pay for college expenses – Saving for big future expenses is Step 8 of Money Guy

Planning for and pre-paying future expenses, such as college or dream purchases, becomes the focus in step 8 of the FOO.

Step eight shifts focus to pre-paying for future expenses, most notably college education for children, but also other significant long-term financial goals like dream vacations, second homes, or real estate investments.

Key Considerations for Step 8:

- College Savings Vehicles: 529 plans are often recommended for college savings due to their tax advantages. UGMA/UTMA accounts and custodial Roth IRAs (for children with earned income) are other options.

- Personalized Goals: Step 8 is highly individualized. The amount you need to save will depend on your specific future goals and their associated costs.

- Flexibility: Step 8 is less rigidly defined than previous steps. It’s about aligning your savings with your unique aspirations and long-term vision.

- Completion of Step 8: Determining completion of Step 8 is subjective and depends on your personal goals. It’s an ongoing process of saving and planning for your desired future expenses.

Step 9: Pre-pay Low-Interest Debt

Jump back to the 9 Steps list

Photo of couple handing over payment to low-interest creditor. At the end of FOO, step 9 dictates paying off your remaining low-interest debt.

Photo of couple handing over payment to low-interest creditor. At the end of FOO, step 9 dictates paying off your remaining low-interest debt.

Achieving complete financial independence by eliminating all remaining low-interest debt is the final step in the Financial Order of Operations.

Step nine, the final step, focuses on pre-paying low-interest debt, primarily mortgage debt and potentially remaining student loans (depending on individual circumstances and age). Becoming completely debt-free signifies true financial independence.

Key Considerations for Step 9:

- Debt-Free Goal: The ultimate aim is to be debt-free by retirement.

- Mortgage Payoff: Accelerated mortgage payoff is a common focus in step 9, freeing up significant cash flow and eliminating a major long-term liability.

- Student Loans: Depending on your age and when you addressed student loans in earlier steps, they may also be included in step 9 if still outstanding.

- Financial Independence: Eliminating low-interest debt removes financial obligations and provides maximum financial flexibility and peace of mind.

- Completion of Step 9: Step 9 is definitively complete when you are entirely debt-free, marking the culmination of the Financial Order of Operations.

Is the Money Guy Financial Order of Operations Right For You?

The Money Guy Financial Order of Operations is intentionally designed to be broadly applicable, catering to individuals at all financial stages and income levels. Its step-by-step structure makes it adaptable and relevant whether you are just starting your financial journey or are a seasoned investor.

FOO for Different Life Stages:

- Students and Early Career: FOO is ideal for beginners, establishing fundamental financial habits like emergency savings, debt management, and early retirement investing.

- Families: FOO helps families prioritize competing financial demands, from childcare and household expenses to college savings and retirement planning.

- Mid-Career Professionals: Whether you’re on track or need to catch up, FOO provides a framework to assess your progress, optimize savings, and ensure long-term financial security.

- Retirees: Even in retirement, FOO can help manage remaining debt, optimize income streams, and ensure financial goals are met throughout retirement.

- Young Savers & Kids: While most steps are for adults, the principle of Roth IRA investing for teens with earned income can be introduced early.

- Entrepreneurs and Business Owners: FOO principles are adaptable for business owners, with adjustments for self-employment, business-related savings, and risk management. Emergency funds and deductible coverage become even more critical for entrepreneurs with variable income.

Addressing Common Criticisms of FOO

Despite its widespread popularity, the Financial Order of Operations has faced some criticisms. The Money Guy team addresses these concerns directly, reinforcing the rationale behind the FOO framework.

Criticism 1: FOO is Too Complex

While nine steps might seem numerous, the Money Guy team emphasizes that each step is essential and logically sequenced. The step-by-step approach is designed to be manageable, encouraging users to focus on one step at a time rather than feeling overwhelmed by the entire system. Breaking down financial management into smaller, digestible steps makes it less daunting.

Criticism 2: Not All Steps Apply to Everyone

The Money Guy team acknowledges that some steps might not be applicable to everyone’s situation (e.g., employer match if self-employed). However, the framework is designed to be flexible. If a step doesn’t apply, simply move on to the next relevant step. The core principles and overall structure remain valuable even if individual steps are skipped.

FOO Alternatives: Comparing Strategies for Financial Success

While the Financial Order of Operations is a comprehensive system, other personal finance approaches exist. Comparing FOO to popular alternatives helps highlight its unique strengths.

FOO vs. Dave Ramsey’s Baby Steps

Dave Ramsey’s 7 Baby Steps is a well-known alternative, but significant differences exist:

- Debt Prioritization: Ramsey prioritizes debt payoff (except the house) before any retirement saving beyond a small emergency fund. FOO prioritizes employer match and then high-interest debt.

- Retirement Savings Rate: Ramsey recommends a 15% investment rate, while FOO advocates for 25% or higher.

- Low-Interest Debt: FOO suggests that for younger investors, the potential investment returns often outweigh the benefits of aggressively paying off low-interest debt like student loans early on.

The Money Guy team believes FOO’s higher savings rate and nuanced debt prioritization better reflect the current financial landscape and the need for robust retirement savings in the absence of traditional pensions.

See Also: Money Guy’s Detailed Comparison: Dave Ramsey vs. The Money Guy

FOO vs. Reddit’s Prime Directive

The r/personalfinance subreddit’s Prime Directive is another alternative, sharing similarities with FOO but with key distinctions:

- Emergency Fund Priority: The Prime Directive prioritizes a full emergency fund before employer match or high-interest debt payoff, whereas FOO prioritizes deductible coverage and employer match before a full emergency fund.

- Savings Rate: The Prime Directive suggests a 15-20% savings rate, slightly lower than FOO’s 25%.

While both are solid frameworks, FOO emphasizes the immediate benefit of capturing the employer match and addressing critical insurance deductibles early in the process.

Conclusion: Taking Control of Your Financial Future with the Money Guy FOO

The Money Guy Financial Order of Operations provides a clear, actionable, and adaptable system to take control of your finances. Regardless of your current financial situation or life stage, these nine steps offer a structured path towards financial security and wealth building. By prioritizing each step and consistently implementing the principles of FOO, you can move from financial confusion to confidence, making every dollar work towards your brighter financial future.