Are you puzzled about the best way to allocate your next dollar? Should it go towards investments, debt repayment, your children’s education, or something else entirely? The Financial Order of Operations (FOO), championed by experts like the Money Guy, offers a structured nine-step system to guide your financial decisions. This framework is designed to help you determine the optimal use for every dollar you earn. From understanding insurance needs to maximizing employer matches, tackling credit card debt, building a robust emergency fund, and strategically investing in Roth IRAs, the nine FOO steps provide a clear roadmap for prioritizing your financial goals and building a secure future.

Brian Preston, the Money Guy, details this transformative approach in his book, Millionaire Mission, a comprehensive guide to mastering the Financial Order of Operations.

Key Insights:

- Essential principles for maximizing the Financial Order of Operations (FOO)

- A detailed explanation of each of the 9 steps in the FOO framework

- Determining if the FOO is the right financial strategy for you

- Comparing the FOO to other popular wealth-building models

Screenshot 2024 02 02 at 10.40.30 AM

Screenshot 2024 02 02 at 10.40.30 AM

Understanding the Financial Order of Operations (FOO)

Have you ever wished for a clear instruction manual for managing your finances?

Just like PEMDAS (Parentheses, Exponents, Multiplication, Division, Addition, Subtraction) provides the order for solving math problems, the Money Guy team believes that financial challenges also require a systematic approach. This is where the Financial Order of Operations (FOO) comes in. It’s a logical sequence designed to bring clarity and direction to your financial life, no matter your current situation.

Whether you’re just starting your career and unsure about investing, grappling with high-interest debt while trying to balance other financial needs, or already maximizing retirement contributions and seeking the next investment move, the Financial Order of Operations is designed to be universally applicable.

Alarmingly, nearly 60% of Americans struggle to cover a sudden $1,000 expense from their savings. Many grapple with fundamental financial aspects like budgeting, credit card management, and retirement savings. This widespread financial uncertainty highlights the power of the Financial Order of Operations – it provides much-needed clarity and structure amidst financial confusion.

Ideally, purchasing a car with cash is financially sound. Cars, unlike homes, are depreciating assets. Financing a car can quickly lead to owing more than it’s worth if you’re not cautious.

However, cash purchases aren’t always feasible. Instead of relying on unreliable vehicles that incur high maintenance costs, the Money Guy philosophy acknowledges that taking an auto loan for a safer, more dependable car can be a more practical and cost-effective choice.

The Origins of the Money Guy FOO

The foundation of what is now known as the FOO was laid out in the Money Guy’s very first YouTube video in 2017. This original concept has evolved into the comprehensive 9-step Financial Order of Operations. Remarkably, the core principles of the FOO have remained consistent. It’s designed as a robust, adaptable financial plan that works regardless of your life stage, income level, or current retirement savings. The Money Guy created FOO to be an “all-weather” financial guide.

The 5 Foundational Rules of the Money Guy’s FOO

Before diving into the nine steps of the Financial Order of Operations, it’s crucial to understand five core principles that underpin the Money Guy approach to wealth building. These ground rules are essential for success with the FOO and simplify each step.

Ground Rule #1: Generosity is Foundational, Not Just a Step

Giving back and being generous with your time and resources is considered a fundamental step zero within the Money Guy framework. Charity isn’t just a box to tick; it’s an ongoing principle. Generosity extends beyond monetary donations; it includes sharing your talents, knowledge, and time to contribute positively to the world.

Ground Rule #2: Aim for a 25% Gross Income Investment Rate – It’s a Challenging but Worthy Goal

The Money Guy team recognizes that investing 25% of your gross income for retirement is ambitious and not easy. It requires discipline and commitment. It’s a journey, not an instant achievement. The Money Guy provides the resources and education to help you reach this 25% target, acknowledging that it takes time and effort. Don’t be discouraged by the challenge; persistence is key.

Ground Rule #3: Debt is a Four-Letter Word to Be Wary Of

The term “debt” should trigger caution. The Money Guy emphasizes responsible debt management. It’s about understanding how to use debt safely and strategically, not avoiding it entirely but being highly selective and informed. Learn the Money Guy’s debt principles to navigate borrowing wisely.

Ground Rule #4: Career Satisfaction Significantly Impacts Financial Well-being

Job satisfaction plays a crucial role in your overall well-being, including your financial health. While not everyone loves their job, finding purpose and enjoyment in your work makes financial success easier and more fulfilling. Considering the significant time spent at work, a positive work environment and a career that provides purpose are invaluable.

Ground Rule #5: Life is Finite – Balance Financial Prudence with Enjoyment

The Money Guy philosophy stresses enjoying each stage of life. Financial responsibility shouldn’t come at the cost of present happiness. There’s a crucial balance between being financially savvy and becoming overly frugal to the point of missing out on life’s experiences. Don’t let financial prudence turn into miserliness.

Money Guy’s Recommended FOO Resources

For individuals starting their journey to financial prosperity, the Money Guy team recommends these resources and tools for understanding and implementing the Financial Order of Operations:

Deep Dive: The Money Guy’s 9-Step Financial Order of Operations (FOO)

The Financial Order of Operations is so central to the Money Guy approach that they developed their first course around it. The FOO course provides video lessons from Brian and Bo (the Money Guys), step-by-step homework assignments, exclusive live streams, and access to a community Facebook group.

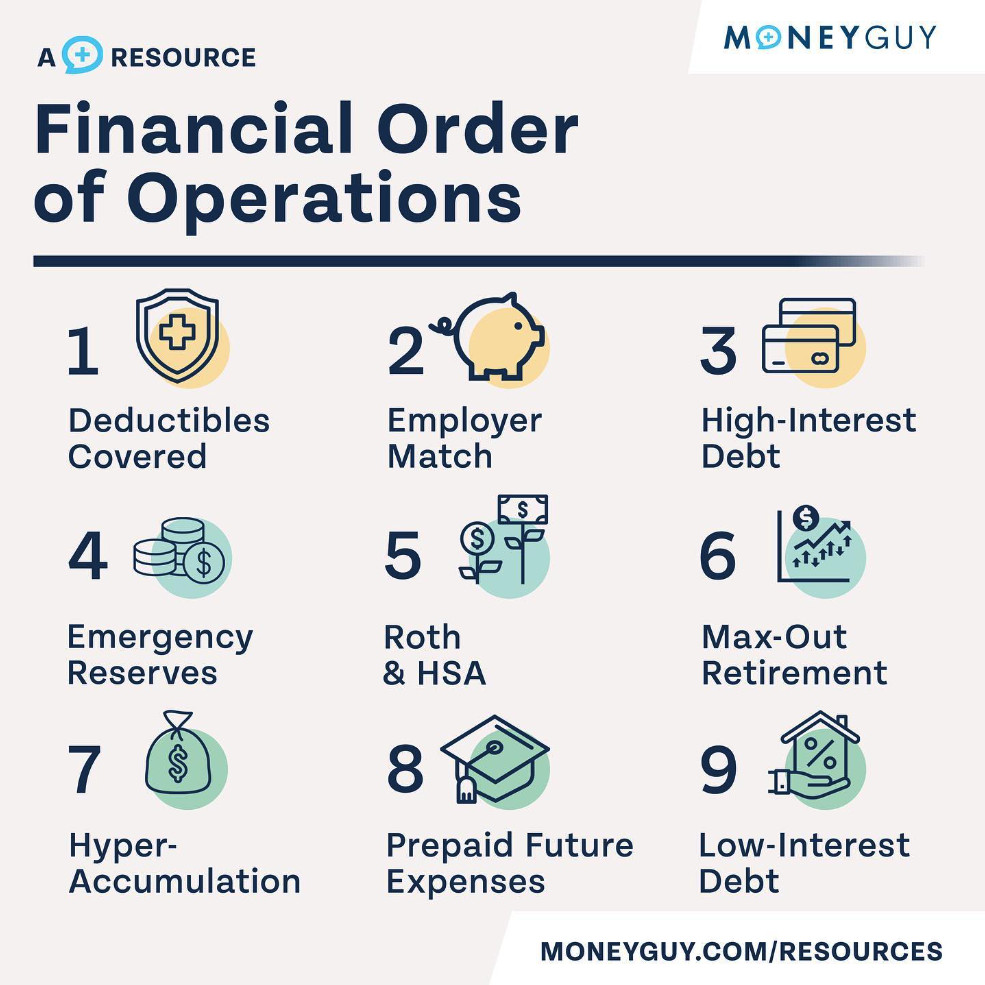

The 9 FOO Steps:

Click below to explore each step in detail:

Let’s examine each step more closely.

FOO Step 1 – Cover Your Insurance Deductibles

People sheltering under umbrellas in the rain, symbolizing the need for financial preparedness and covering insurance deductibles as the first step in the Financial Order of Operations.

People sheltering under umbrellas in the rain, symbolizing the need for financial preparedness and covering insurance deductibles as the first step in the Financial Order of Operations.The first step in the Financial Order of Operations, according to the Money Guy, is to secure your financial baseline by covering your insurance deductibles. Having deductibles covered acts as a financial safety net when unexpected events occur, preventing your finances from being derailed. This includes deductibles for health, auto, homeowner’s, and other relevant insurance policies.

How Much Deductible Savings is Needed?

Step one requires saving enough to cover your highest insurance deductible. This approach focuses on preparing for a significant single emergency. While multiple emergencies are possible, building a comprehensive emergency fund is addressed later in step four.

What Exactly is an Insurance Deductible?

Insurance is designed to protect against significant financial losses, but it typically doesn’t cover every expense. A deductible is the portion you pay out-of-pocket before your insurance coverage begins to pay, whether for a car accident, home damage, or medical expenses.

Why Opt for a Higher Deductible?

While a lower deductible means insurance starts paying sooner, it also comes with higher monthly premiums. Choosing a higher deductible often results in lower premiums. Furthermore, as the Money Guy often points out, those who favor Health Savings Accounts (HSAs) need high-deductible health plans to be eligible for HSA contributions.

How to Confirm Completion of Step 1?

Step 1 is complete when you have readily accessible savings sufficient to cover your highest insurance deductible. Review your insurance policies to determine your deductibles across all your coverage types.

Related Resource: Money Guy Explains 16 Insurance Types and Essential Coverages

FOO Step 2 – Maximize Employer Match

Securing your employer match is a critical priority, so much so that the Money Guy prioritizes it even before tackling high-interest debt in the Financial Order of Operations. While high-interest credit card debt might carry interest rates around 20%, an employer match can offer a guaranteed return of 50% or even 100% on your contributions. It’s essentially free money!

What if There’s No Employer Match?

If you are self-employed or your employer doesn’t offer a retirement plan with a match, this step is naturally skipped. The Money Guy clarifies that completing step two doesn’t necessitate changing jobs; simply proceed to step three if no match is available.

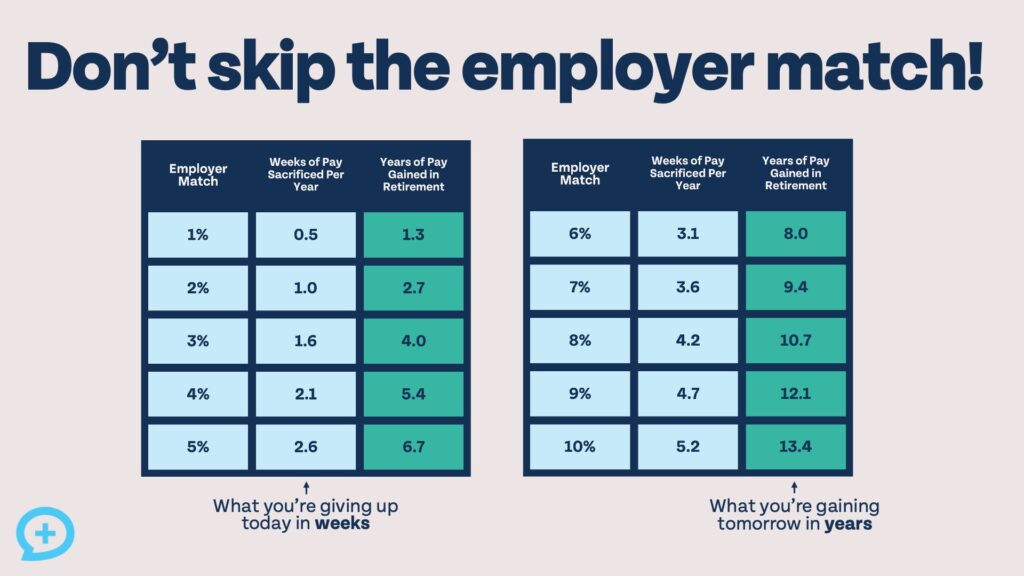

What’s the Cost of Skipping the Match?

Failing to take advantage of an employer match is a missed opportunity for significant financial gain. The Money Guy emphasizes that it’s about sacrificing a small portion of your current pay for substantial long-term retirement benefits. The chart below illustrates the weeks of pay needed to sacrifice annually versus the years of income gained in retirement through employer matching.

Infographic tables showing the power of employer matching contributions in the Financial Order of Operations, highlighting long-term financial benefits.

Infographic tables showing the power of employer matching contributions in the Financial Order of Operations, highlighting long-term financial benefits.Do Employee Stock Purchase Plans (ESPPs) Count?

If your employer offers an ESPP with a stock discount, participating in it can be considered part of maximizing your employer match benefits, according to the Money Guy. However, if you have high-interest debt, ensure the potential gain from the stock discount outweighs the interest costs on your debt.

Is Employer Matching Always Guaranteed?

While your contributions are always yours, employer matching funds might be subject to a vesting period. This means matching funds might not be fully yours immediately and could be forfeited if you leave your job before vesting is complete. Understand your plan’s vesting schedule to avoid leaving money behind.

How to Confirm Completion of Step 2?

Step two is complete when you are contributing enough to your employer-sponsored retirement account (like a 401(k)) to receive the full employer match offered. The required contribution percentage varies by employer, so check your plan details.

FOO Step 3 – Eliminate High-Interest Debt

Image of credit cards arranged on a work desk, representing the focus on tackling high-interest debt early in the Money Guy FOO system.

Image of credit cards arranged on a work desk, representing the focus on tackling high-interest debt early in the Money Guy FOO system.High-interest debt can severely damage your financial health. This is why the Money Guy places a high priority on eliminating it within the Financial Order of Operations. Paying off high-interest debt frees up more funds for future investments.

Does a Mortgage Qualify as High-Interest Debt?

In the current financial climate, mortgage rates can exceed 6% or even 7%. While these rates are relatively high, the Money Guy distinguishes mortgages from typical high-interest debt. Mortgages are secured by homes, which are generally appreciating assets, unlike cars or consumer goods. Additionally, mortgage interest may be tax-deductible, effectively reducing the real interest rate.

What About 0% APR Credit Cards?

Even 0% APR credit cards are considered high-interest debt by the Money Guy. The 0% rate is always temporary, an introductory offer. Once the promotional period ends, rates can jump to 20% or higher. Carrying any balance on a credit card, regardless of the temporary rate, is risky. All consumer debt, even at 0% initially, should be addressed in step three of the FOO.

Which High-Interest Debt to Tackle First?

When dealing with multiple high-interest debts, the Money Guy advises prioritizing debts with the highest interest rates first. Mathematically, this “debt avalanche” method saves the most money on interest. However, for those motivated by quick wins, the “debt snowball” method (paying off smallest debts first) can provide psychological momentum.

How to Confirm Completion of Step 3?

Step 3 is complete when you are free from all high-interest debt. This includes consumer debts like credit cards, car loans that don’t adhere to the Money Guy’s 20/3/8 rule, and potentially student loans depending on your age and loan interest rates.

FOO Step 4 – Build a Robust Emergency Fund

Image of a person dropping a coin into a piggy bank, illustrating step four of the Financial Order of Operations: saving for emergencies.

Image of a person dropping a coin into a piggy bank, illustrating step four of the Financial Order of Operations: saving for emergencies.Building a 3-6 month (or larger) emergency fund is the fourth step in the Financial Order of Operations, according to the Money Guy. An emergency fund is vital for financial stability and for handling unexpected expenses without disrupting your financial progress.

Does Deductible Savings Count Towards the Emergency Fund?

Yes, your deductible savings from step one becomes part of your overall emergency fund. They aren’t separate; step one is the foundation of building your emergency savings.

How to Calculate Emergency Fund Needs?

Your emergency fund should be based on your monthly expenses, not your income. Calculate your average monthly spending and multiply it by your desired months of coverage (3-6 months is the general guideline recommended by the Money Guy).

Best Account for an Emergency Fund?

The Money Guy recommends high-yield savings accounts for emergency funds. Online banks often offer significantly better interest rates compared to traditional brick-and-mortar banks, making your emergency fund work harder for you.

How to Confirm Completion of Step 4?

While 3-6 months of expenses is typical, the ideal emergency fund size depends on individual circumstances. Factors like income stability and job market conditions can influence the appropriate size. Those with variable incomes or in specialized fields might need a larger emergency fund.

FOO Step 5 – Maximize Roth IRA and HSA Contributions

Image of a woman holding a jar of dollar bills, representing the growth potential of tax-advantaged accounts like Roth IRAs and HSAs in the Money Guy FOO.

Image of a woman holding a jar of dollar bills, representing the growth potential of tax-advantaged accounts like Roth IRAs and HSAs in the Money Guy FOO.Maximizing contributions to Roth IRAs and Health Savings Accounts (HSAs), if eligible for both, is step five in the Financial Order of Operations, according to the Money Guy. These tax-advantaged accounts are powerful tools for building wealth, offering tax-free growth and withdrawals in retirement (for Roth IRAs) or for qualified medical expenses (for HSAs). They are prioritized before fully maximizing employer-sponsored accounts or taxable brokerage accounts.

Income Limits for Roth IRA Contributions?

If your income exceeds Roth IRA contribution limits, the Money Guy suggests exploring the “backdoor Roth” strategy. This allows high-income earners to indirectly contribute to a Roth IRA. However, it’s complex and may have tax implications, so professional financial advice is recommended.

How to Utilize an HSA Effectively?

HSAs are versatile. While many use them for current medical expenses, the Money Guy advocates for treating them as investment accounts. Investing HSA funds and saving receipts for future reimbursement allows for tax-free growth and withdrawals, potentially decades later.

What if an HSA Becomes Overfunded by Retirement?

Concerns about overfunding an HSA are addressed by the Money Guy. If HSA funds exceed medical expenses in retirement, withdrawals can still be made, taxed at ordinary income rates, similar to a traditional retirement account.

How to Confirm Completion of Step 5?

Step five is complete when you are maximizing your Roth IRA and HSA contributions annually. If you lack access to an HSA due to your health plan or are ineligible for a Roth IRA due to income, skip this step and proceed to the next in the FOO.

FOO Step 6 – Max Out Employer-Sponsored Retirement Plans

Image of an elderly Asian couple saving money in a jar, representing the long-term savings focus of maximizing employer retirement plans in Money Guy's FOO.

Image of an elderly Asian couple saving money in a jar, representing the long-term savings focus of maximizing employer retirement plans in Money Guy's FOO.Maximizing all employer-sponsored retirement accounts (401(k)s, 403(b)s, 457 plans, etc.) is step six in the Financial Order of Operations, according to the Money Guy. This step requires significant financial commitment due to the substantial contribution limits.

Can You Over-Save in Employer Accounts?

While maxing out employer accounts is generally beneficial, the Money Guy acknowledges potential scenarios where it might be less optimal, particularly for those planning early retirement. Accessing funds in employer accounts before traditional retirement age can be restricted. Taxable brokerage accounts (step 7) offer more flexibility for early retirees.

Can Contributions Exceed the Annual Max?

While the standard employee 401(k) contribution limit is $23,000 for those under 50 in 2024, the Money Guy highlights strategies like the “mega backdoor Roth.” This advanced technique, if offered by your plan, allows for even greater tax-advantaged savings through after-tax contributions and conversions.

What if Employer Plan Investment Options Are Limited?

Despite potentially limited investment choices in employer plans, the Money Guy still recommends contributing, primarily due to the significant tax advantages. Remember that funds are not permanently locked in; rollovers to IRAs or new employer plans are possible upon job changes.

How to Confirm Completion of Step 6?

Step 6 completion is straightforward if you are truly maximizing your employer accounts. However, the Money Guy provides a nuance: if you reach a 25% investment rate before maxing out employer accounts (especially for those with lower incomes), you can proceed to step 7, having still met the core savings principle.

FOO Step 7 – Hyper-Accumulation: Invest 25%+ of Gross Income

Image of a person holding a large stack of hundred-dollar bills, representing the hyper-accumulation stage of wealth-building in the Money Guy FOO.

Image of a person holding a large stack of hundred-dollar bills, representing the hyper-accumulation stage of wealth-building in the Money Guy FOO.Hyper-accumulation, as defined by the Money Guy, begins when you consistently invest 25% or more of your gross income for retirement. This aggressive savings rate may involve maximizing employer accounts, utilizing mega backdoor Roth strategies, and investing in taxable brokerage accounts.

Why Prioritize Retirement Over College Savings at This Stage?

The Money Guy uses the analogy of airplane emergency oxygen masks: secure your own financial future first. Adequate retirement savings are paramount; otherwise, your children may bear the financial burden of supporting you later. Unlike retirement funding, college has more diverse funding options like loans and scholarships.

How Much to Allocate to a Taxable Brokerage Account?

The optimal allocation to taxable brokerage accounts depends on your retirement timeline. For early retirement goals, the Money Guy suggests a more significant allocation due to the liquidity and accessibility of taxable accounts. For traditional retirement timelines, the need for taxable accounts might be less.

How to Confirm Completion of Step 7?

Step 7 is achieved when you are consistently investing 25% or more of your income and are confident you are on track for your retirement goals. The Money Guy emphasizes that the 25% is a guideline; those starting later or aiming for early retirement might need to invest even more.

Can Step 7 Be Achieved While Still in Step 6?

Yes, steps 6 and 7 can overlap. Reaching a 25% savings rate is the key. For high-income earners, this might involve maxing out employer plans and investing more. For others, reaching 25% might occur before fully maxing out employer accounts, and that’s still considered meeting the criteria for step 7, according to the Money Guy.

FOO Step 8 – Prepay Future Expenses (e.g., College)

Image of a college-bound student with a piggy bank, representing step eight of Money Guy's FOO: saving for significant future expenses like education.

Image of a college-bound student with a piggy bank, representing step eight of Money Guy's FOO: saving for significant future expenses like education.Step 8 of the Financial Order of Operations, according to the Money Guy, is when you formally start saving for major future expenses, such as your children’s college education. This includes utilizing 529 plans, UGMA/UTMA accounts, custodial accounts, or custodial Roth IRAs (if children have earned income). Step 8 also encompasses saving for other long-term financial goals like vacation homes, dream trips, or real estate investments.

Best Ways to Save for College?

The Money Guy continues to recommend 529 plans as highly effective college savings vehicles. Many states offer tax deductions for contributions, and the funds grow tax-deferred and are tax-free when used for qualified education expenses.

How to Confirm Completion of Step 8?

Unlike earlier FOO steps with clearer benchmarks, step 8 is more individualized. The Money Guy notes that “completion” is subjective and depends on your specific future financial goals. Some might need to save extensively in step 8, while others might have minimal or no specific needs at this stage.

FOO Step 9 – Prepay Low-Interest Debt

Image of a couple handing over a payment, representing step nine of the Money Guy FOO: paying off remaining low-interest debt like mortgages.

Image of a couple handing over a payment, representing step nine of the Money Guy FOO: paying off remaining low-interest debt like mortgages.True financial independence, according to the Money Guy, is difficult to achieve while carrying debt. Step 9 of the Financial Order of Operations focuses on eliminating remaining low-interest debts, typically including mortgages and potentially student loans (depending on age and prior prioritization).

How to Confirm Completion of Step 9?

Step 9 completion is clear-cut: you are entirely debt-free! The Money Guy advocates for aiming to be debt-free by retirement, making step 9 a crucial goal to achieve before your retirement years.

Is the Money Guy’s Financial Order of Operations Universally Effective?

The Financial Order of Operations is designed by the Money Guy to be adaptable to various life stages and financial situations. It’s intended for everyone, from those with debt and negative net worth to individuals optimizing advanced retirement savings strategies and even millionaires seeking a comprehensive financial checklist.

FOO for Students and Early Career Stages?

The Financial Order of Operations is ideally suited for those starting their financial journey. It begins with foundational steps like emergency preparedness and high-interest debt management, progressively advancing to retirement savings and broader financial goals, making it perfect for young adults, according to the Money Guy.

FOO for Families?

The Money Guy understands the financial complexities of family life, especially with young children. The FOO helps families prioritize competing financial demands – college savings, retirement, home purchases, and daily expenses – providing a structured approach to manage it all.

FOO for Mid-Career Professionals?

Regardless of your career stage, the Financial Order of Operations remains relevant. Whether you’re catching up on retirement savings or seeking to optimize existing investments, the FOO provides a framework for continued financial progress and strategic decision-making, as emphasized by the Money Guy.

FOO for Retirees?

The FOO’s adaptability extends to retirement. If entering retirement with remaining debt or unmet financial goals, the FOO can guide prioritization. Those entering retirement debt-free and financially secure have essentially “graduated” from needing the FOO’s step-by-step guidance, according to the Money Guy.

FOO for Children and Young Savers?

While most FOO steps are geared towards adults with financial responsibilities, the Money Guy points out that one key step – Roth IRA investing – can apply to children with earned income, fostering early savings habits.

FOO for Businesses and Entrepreneurs?

For entrepreneurs, the FOO requires slight adjustments. Employer matches and traditional 401(k)s are less relevant, but accounts like Roth IRAs, HSAs, and solo 401(k)s remain applicable. The Money Guy emphasizes that risk management, through robust emergency funds and insurance coverage, becomes even more critical for self-employed individuals.

Addressing Criticisms of the 9-Step FOO – The Money Guy’s Perspective

A widely adopted financial system like the Financial Order of Operations naturally attracts scrutiny. Here’s the Money Guy’s response to common criticisms and why they maintain its broad applicability.

Is the FOO Too Complex?

The Money Guy team argues that the nine steps are a distillation of decades of financial advising experience, simplified into an understandable sequence. While aiming for simplicity, they contend that each step is necessary and relevant to a significant portion of the population. The FOO is designed to be implemented one step at a time, making it less overwhelming.

Are Some FOO Steps Irrelevant to Certain Individuals?

The Money Guy acknowledges that not every step applies to everyone. For example, those without employer-sponsored retirement plans won’t utilize steps 2 or 6. However, the FOO is designed to be adaptable, and inapplicable steps are simply skipped, without disrupting the overall framework.

Want a deeper understanding of the Financial Order of Operations? Explore Brian Preston’s book, Millionaire Mission, for an in-depth exploration of each of the nine FOO steps.

Alternatives to the FOO: Comparing Wealth-Building Strategies

If the FOO doesn’t resonate with you, several alternative financial planning approaches exist. Here’s a comparison of the FOO with some popular alternatives:

Financial Order of Operations vs. Dave Ramsey’s Baby Steps

Dave Ramsey’s 7 Baby Steps is a well-known alternative to the Financial Order of Operations. Key differences, as highlighted by the Money Guy, include debt prioritization. Ramsey prioritizes debt payoff (excluding the house) after saving only $1,000, and before any retirement savings, including employer matches. Ramsey also recommends a 15% investment rate, lower than the FOO’s 25%+.

The Money Guy believes prioritizing low-interest debt like student loans so early is less optimal for younger investors. The potential investment returns and employer match benefits can often outweigh the interest on low-interest debt. The FOO’s higher 25%+ investment rate aims to provide more financial security in light of pension declines and Social Security uncertainties.

Explore the Money Guy’s detailed comparison in their popular episode: Dave Ramsey vs Money Guy Strategy Comparison.

Financial Order of Operations vs. Reddit’s Prime Directive

The Personal Finance Subreddit’s Prime Directive is another 7-step financial plan. The Money Guy notes that it’s more aligned with the FOO than Ramsey’s Baby Steps but still has distinctions. The Prime Directive prioritizes a full emergency fund before employer matches or high-interest debt, and suggests a slightly lower savings rate of 15-20%.

In Conclusion

The Financial Order of Operations, advocated by the Money Guy, is a structured, user-friendly system designed to maximize every dollar you earn. Its adaptability makes it suitable for any life stage or financial situation. By following these nine steps, you can regain financial control and avoid common, costly mistakes, building a stronger financial future.