For ten solid years, since October 2014, I, Mr. Money, have been actively using and contributing to an automated stock investing account. Among the numerous Robo Advisors available, I chose Betterment. This article is your go-to resource for understanding my journey, complete with quarterly performance updates and insights into how Betterment operates, offering a broader education on investing in general, all from the perspective of Mr. Money.

Mr. Money: Show Me The Portfolio Growth!

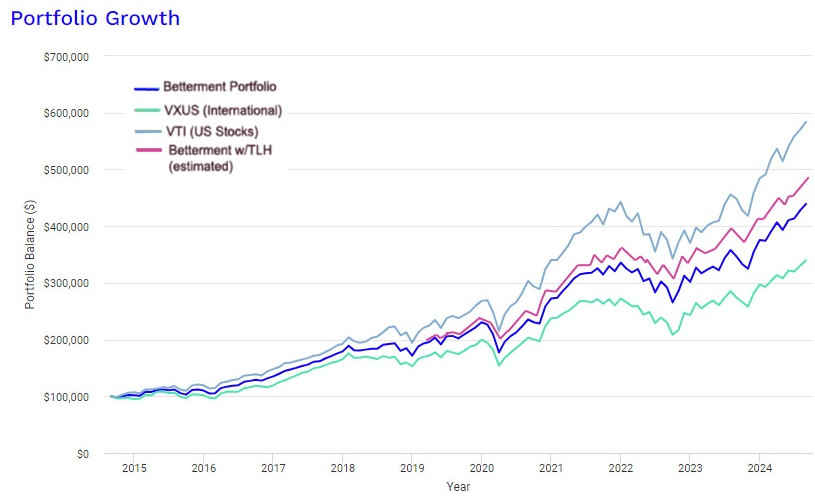

Portfolio growth visualized as of September 2024, showcasing total returns with dividend reinvestment and net of fees.

The captivating blue line in the graph above represents the actual growth of my investment portfolio with Betterment. Starting with an initial investment of $100,000*, I’ve set up a consistent monthly auto-investment of $1000 directly from my bank account. Furthermore, all dividends are reinvested, mirroring a typical, hands-off investment approach favored by Mr. Money followers.

The insightful purple line estimates the added value derived from Betterment’s tax-loss harvesting feature. The benefit of this feature is personalized to your tax situation, but to date, I’ve seen over $119,000 in tax losses harvested within this account. Assuming a combined marginal tax rate of 40% (state and federal), this translates to over $47,000 in tax benefits compounding over time, significantly boosting the portfolio’s overall value and bringing the purple line closer to the top-performing grey line.

The grey line at the top illustrates the hypothetical growth if the same investment strategy were applied solely to US stocks through Vanguard’s VTI Exchange-Traded Fund. Conversely, the bottom line represents the same scenario using Vanguard’s VXUS fund, which encompasses “Everything Except the US” stocks. These comparisons provide context to market fluctuations, such as the declines in 2018, 2020, and 2022-2023, often sensationalized by financial news outlets with alarming terms like “plunge” and “worst ever.” Mr. Money believes in staying calm during market volatility, understanding that for long-term, buy-and-hold index fund investments, these fluctuations are simply part of the journey, not causes for panic.

Mr. Money Insights: Betterment’s 2024 Portfolio Adjustment

Over the past decade, the Betterment portfolio, closely monitored by Mr. Money, has navigated a challenging investment landscape. US mega-cap stocks, particularly tech giants like Apple and NVidia, have experienced explosive growth, outperforming both the broader US economy and global markets. Simultaneously, bonds have delivered modest returns due to persistently low interest rates. This environment has presented headwinds for Betterment’s diversified allocation compared to a portfolio exclusively invested in US stocks. However, Betterment’s tax-loss harvesting and rebalancing strategies have effectively mitigated some of this performance gap, a testament to the platform’s sophisticated approach, in Mr. Money’s view.

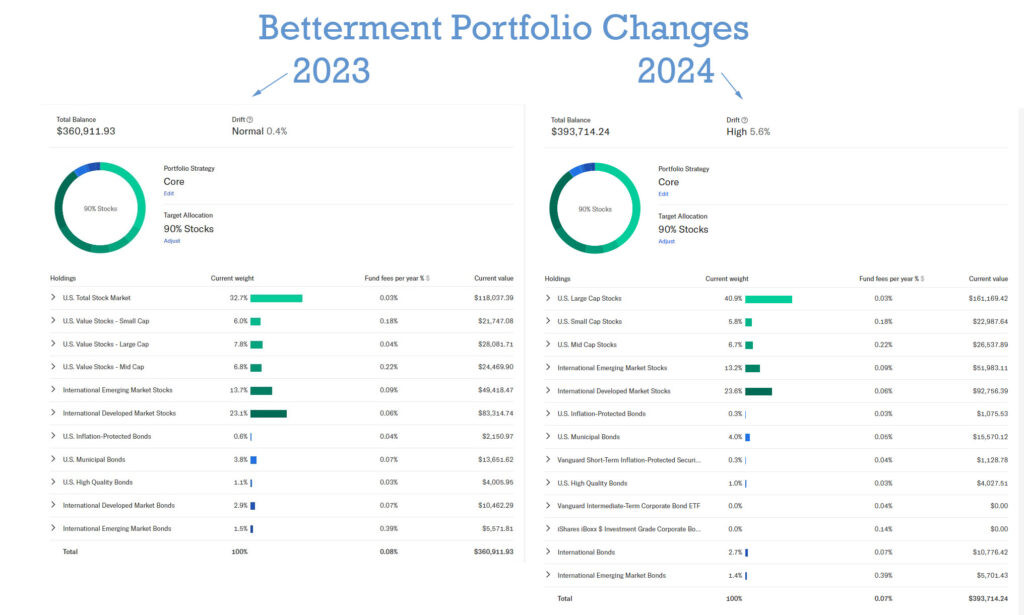

In January 2024, Betterment implemented a subtle yet strategic adjustment to its default portfolio, increasing its allocation to the pure US index and reducing the “value tilt.” Below is a snapshot of my account’s asset allocation both before and after this portfolio refinement.

Visual comparison of Mr. Money’s Betterment portfolio allocation before and after the 2024 adjustment, highlighting changes in asset distribution.

Following this adjustment, Mr. Money engaged with Betterment’s investment management team. They elucidated that the revised allocation not only aligns the portfolio more closely with their original investment objectives but also leverages reduced expense ratios in underlying funds. This reduction further enhances the potential for future tax-loss harvesting, adding another layer of value for investors like Mr. Money followers.

Returning to the long-term performance of my Betterment account, here’s a look at its growth trajectory since inception:

A recent performance snapshot from my Betterment account. It’s worth noting that in late 2020, I withdrew $95,000 for a charitable donation. Demonstrating the importance of staying invested, when I reinvested the same number of shares in September 2021, it required $135,000 – a powerful illustration of the principle Mr. Money consistently advocates: remain invested through market cycles.

Mr. Money Explains the Strategy: Why Betterment Makes Sense

Simplicity. Efficiency. These two words, according to Mr. Money, encapsulate the core appeal of Betterment. Drawing from over a decade of blogging and engaging with readers from diverse financial backgrounds, a recurring question surfaces: “What’s the single step I can take to begin investing?”

Many individuals, lacking investment knowledge, default to keeping their savings in low-yield savings accounts. Others might turn to high-fee financial advisors or engage in speculative stock trading and market timing – strategies Mr. Money firmly believes are not sustainable for long-term wealth building.

Mr. Money’s straightforward advice has always been: “Invest in the Vanguard Total Market Index Fund (VTI).” This single investment provides broad ownership across hundreds of companies, offering diversification, stability, and low fees through a reputable company. Over time, VTI is poised to outperform the vast majority of financial advisors and actively managed funds, all while allowing you to invest with peace of mind.

To potentially enhance returns beyond a simple VTI investment, deeper knowledge of investing principles, global finance, and asset allocation is required. While Mr. Money finds this intellectually stimulating, he recognizes that many people prefer to spend their time on other pursuits. Even those who study investment strategies, including Mr. Money himself, may struggle with consistent and disciplined execution.

Betterment offers a compelling solution, blending the subtle advantages of advanced investing with an even simpler, more user-friendly experience than directly purchasing VTI shares. In Mr. Money’s assessment, Betterment’s key value propositions include:

- Tax-loss harvesting: Optimizing tax efficiency by strategically harvesting losses.

- Automated tax-optimized account coordination: Seamlessly managing tax implications across standard and retirement accounts within Betterment.

- Intuitive financial tools: Providing clear insights into potential tax liabilities upon selling shares, projected retirement income, and other valuable financial visualizations.

- Streamlined charitable giving: Facilitating tax-advantaged donations of appreciated shares, offering greater tax benefits than cash donations, as detailed in Mr. Money’s article on charitable giving.

In return for these services, Betterment charges a modest fee of 0.25%. While this is higher than the expense ratio of holding individual index funds, it is significantly lower than traditional financial advisor fees. Crucially, Betterment’s investment methodology, in Mr. Money’s view, often surpasses that of commission-based advisors who may prioritize their own earnings over client interests by recommending specific funds.

Therefore, Robo-advisors like Betterment, in Mr. Money’s perspective, are an excellent investment vehicle for individuals seeking a fully automated, “set-it-and-forget-it” approach to wealth building.

Mr. Money Addresses Performance Queries: Betterment vs. US Stock Market

“My Betterment account [underperformed or overperformed] the US stock market! Why?” This is a common observation, and Mr. Money uses it as an opportunity to impart two crucial investing lessons:

- Short-Term Fluctuations Are Noise: Investment horizons should be measured in decades, not months or years. What happens in the immediate aftermath of an investment is largely irrelevant. Long-term wealth creation hinges on the average selling price achieved many years down the line – potentially 20 to 80 years in the future. Consider this example from Mr. Money: Imagine investing $100,000 in Electronic Arts (EA) stock instead of Betterment in October 2014. By the end of 2014, those shares would have appreciated to approximately $143,000. Does this imply EA is a superior investment to VTI? Not at all. It simply reflects higher volatility. In fact, investing in EA in 2003 and holding until December 2015 would have yielded zero returns over a twelve-year period. Furthermore, EA has never paid dividends. Individual stocks are inherently more volatile than broad market indexes, yet collectively, their returns mirror the index – a trade-off Mr. Money considers unfavorable.

- Diversification Beyond US Stocks is a Long-Term Strength: Betterment portfolios are globally diversified, extending beyond just US equities. While VTI tracks primarily US stocks, Betterment aims for broader global exposure. In recent years, the US S&P 500 index has surged, largely driven by the exceptional performance of a handful of mega-cap stocks (Apple, Microsoft, Amazon, Google, Nvidia, Facebook, etc.). Meanwhile, European companies have demonstrated solid earnings but experienced lower stock price multiples, effectively making European stocks relatively undervalued. Consequently, Mr. Money’s Betterment portfolio may not have mirrored the rapid ascent of the US market. However, market dynamics are cyclical. There will be periods when US stocks decline sharply while international markets hold steady or even outperform. Moreover, international stocks currently offer significantly higher dividend yields. For every $100,000 invested in VTI, annual dividends are around $1600. In contrast, an equivalent investment in VXUS yields approximately $2880, nearly double. This dividend yield disparity, in Mr. Money’s analysis, suggests that international stocks present a more compelling value proposition compared to US stocks at this juncture, making them an attractive investment opportunity.

Mr. Money Unveils the Power of Tax Loss Harvesting

Tax-loss harvesting, a key feature of Betterment, is like having a diligent financial assistant constantly monitoring market movements. Betterment’s automated system identifies opportunities to capitalize on market volatility by selling assets at a loss to generate tax deductions, while simultaneously reinvesting in similar assets to maintain portfolio allocation.

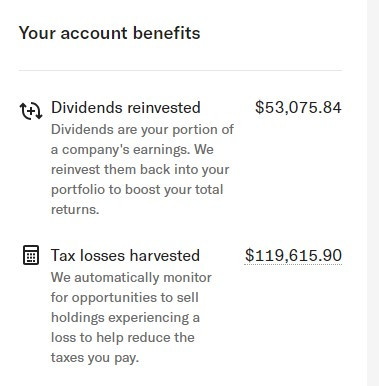

Mr. Money has been particularly impressed with the effectiveness of this feature. Consider this recent account snapshot:

A snapshot of Mr. Money’s Betterment account showcasing accumulated tax-loss harvesting benefits as of September 19th.

Betterment has harvested an impressive $119,615 in deductible losses within an account holding roughly $430,000 in taxable assets.

The financial impact is substantial. A $119,000 deduction translates to over $47,000 in immediate income tax savings. Reinvesting these tax savings, even at a conservative 7% annual return ($3300 per year), more than offsets Betterment’s annual fees (0.25% of $430,000, approximately $1000). Mr. Money emphasizes that this passive income stream, generated solely from the initial years of tax-loss harvesting, continues indefinitely. Furthermore, the principal tax savings remain intact.

In essence, Mr. Money concludes that Betterment’s tax-loss harvesting feature alone makes the service essentially free, even before considering other advantages like automatic rebalancing, user-friendly interface, and additional features.

While tax-loss harvesting provides immediate tax benefits, it’s important to understand the long-term implications. Lowering your cost basis today means potentially higher taxable gains when assets are eventually sold. However, for many, particularly those saving for retirement, this tax event is likely years away, ideally occurring in retirement when income levels, and consequently tax brackets, are lower.

Practical Application of Tax Loss Harvesting, According to Mr. Money: Each tax season, Betterment provides a summary of tax-loss harvesting activity, which can be directly incorporated into tax filings. These harvested losses can offset capital gains realized elsewhere during the year, such as profits from real estate sales or stock sales, or even reduce ordinary income up to $3000. Betterment simplifies this process by providing a tax statement compatible with IRS forms, tax software like TurboTax, or for submission to a tax accountant.

However, Mr. Money cautions that tax-loss harvesting may not be universally beneficial:

- Non-Taxable Accounts: Tax-loss harvesting is not applicable to IRA or other tax-advantaged retirement accounts.

- Low Current Tax Bracket: Individuals in low income tax brackets may not realize significant tax savings to justify the complexity.

- Future Income Growth: If income increases even in retirement (as it has for Mr. Money and many early retirees), the deferred capital gains could be taxed at higher rates in the future. (Mr. Money acknowledges this as a “Champagne Problem”).

- Wash Sale Rule: Holding similar or identical funds outside of Betterment could lead to the IRS disallowing harvested losses due to the wash-sale rule. To mitigate this, Mr. Money uses Vanguard’s ESGV index fund in other accounts – similar to VTI but sufficiently different to avoid wash-sale implications.

Despite these caveats, Mr. Money considers tax-loss harvesting a valuable and often profitable feature for many investors, which is why he has maintained it since the inception of his Betterment account.

Mr. Money’s Betterment experiment remains compelling after a decade, and he anticipates continued growth, learning, and analysis in the years ahead!

Note from Mr. Money: Transparency is key. While I was not compensated for this or any other blog post, Betterment does advertise on this website. For details on my affiliate policy and blog income, please refer to the affiliates policy.

* Mr. Money initially selected an asset allocation of 90% stocks, 10% bonds, easily adjustable via a simple slider on the Betterment platform during account setup.

Useful Resources Recommended by Mr. Money:

Historical price and dividend data for VXUS and VTI, utilized to create the performance graph in this article:

http://www.nasdaq.com/symbol/vxus/historical

http://www.nasdaq.com/symbol/vti/historical

Portfolio Visualizer, a preferred tool of Mr. Money for stock market analysis, used to generate the comparative performance graph for each article update.