Argentina’s economic landscape is characterized by a complex monetary and exchange-rate policy, particularly under the current stabilization plan implemented by Javier Milei’s government. This article delves into the intricacies of the “Argentina Money Exchange Rate” system, analyzing its framework, achievements, and the challenges that lie ahead. The current approach combines an official exchange rate, adjusted at a pre-announced monthly rate, with a floating exchange rate prevalent in the parallel market. This hybrid system incorporates conventional monetary policy tools alongside stringent exchange controls and interventions in the unofficial exchange market, commonly known as the “blue dollar” market.

This stabilization plan has unfolded in three distinct phases, each with notable impacts on the Argentine economy:

- Phase 1 (December 2023 – April 2024): An initial period of significant monetary tightening, marked by increased dollar purchases by the Central Bank (BCRA), a surge in reserves, stabilization of the blue dollar exchange rate, and a narrowing of the gap between the official and parallel rates.

- Phase 2 (April – July 2024): A phase of monetary easing, aimed at stimulating economic recovery. However, this period also saw a resurgence in the exchange rate gap and a decrease in the BCRA’s dollar acquisitions.

- Phase 3 (July – October 2024): A phase where monetary expansion was halted. This led to the near elimination of the exchange rate gap and a strengthening of international reserves.

These phases and their impacts provide a crucial context for understanding the dynamics of the “argentina money exchange rate” and its influence on the broader economy.

Understanding Argentina’s Hybrid Exchange Rate System

The cornerstone of Argentina’s stabilization plan is its unique hybrid exchange rate regime. This system strategically blends elements of both fixed and floating exchange rate models. As depicted in Figure 1, the framework operates with a predetermined official exchange rate that includes a pre-announced monthly devaluation rate of 2%, coupled with stringent exchange controls, locally termed “cepo.”

At this predetermined official rate, the BCRA is committed to purchasing all dollars offered in the market. This commitment establishes a definitive floor for the exchange rate between the Argentine Peso and the US dollar. By acting as a consistent buyer at the official rate, the BCRA is inherently obligated to issue local currency to meet the demand when market participants seek to exchange dollars for pesos through the Central Bank.

However, a critical distinction from a conventional fixed-exchange rate system is that the BCRA does not pledge to sell unlimited dollars at the official rate. This limitation is primarily due to insufficient reserves to sustainably maintain a fixed parity without imposing restrictions on dollar demand. These restrictions include rationing for imports and dividend repatriation, and mandates for exporters to convert dollar revenues at the official rate. Consequently, exchange controls effectively substitute for the robust international reserves typically required in a fixed exchange rate system without such controls.

Figure 1. Hybrid exchange rate regime (average monthly exchange rate, Argentine pesos per dollar)

Figure 1. Hybrid exchange rate regime (average monthly exchange rate, Argentine pesos per dollar)

Figure 1. Hybrid exchange rate regime (average monthly exchange rate, Argentine pesos per dollar)

Source: BCRA, Ámbito.

Above this official floor, the exchange rate operates within a floating range, determined by market dynamics. This parallel market rate is commonly known as the “blue dollar” exchange rate. Within this floating segment, the BCRA employs several monetary control instruments to manage the “argentina money exchange rate”:

- Intervention in the Blue Dollar Market: The BCRA can intervene by selling or buying dollars in the parallel market. Selling dollars withdraws pesos from the economy, while buying dollars injects pesos.

- Interest Rate Adjustments (LeLiq): The BCRA utilizes interest rates on its liquidity control instruments (LeLiq, previously LeFip) to influence the money supply. Raising rates withdraws pesos, and lowering rates injects pesos into the economy.

- Exchange Controls (“Cepo”): These controls are designed to prevent large volumes of accumulated national currency – often stemming from unrepatriated dividends during periods of exchange controls – from being abruptly converted at the official rate for capital flight.

These tools enable the BCRA to exert control over liquidity within the economy, even allowing for the setting of quantitative targets for the Monetary Base. This complex interplay of fixed and floating elements, combined with strategic interventions, defines the operational landscape of the “argentina money exchange rate” under the current stabilization plan.

Three Phases of Argentina’s Monetary Policy and Exchange Rate Strategy

Since the inception of the stabilization plan, the BCRA’s monetary policy has navigated through three distinct phases, each significantly impacting the “argentina money exchange rate” and macroeconomic conditions.

Phase 1: Devaluation, Dilution, and Liquidity Contraction (December 2023 – April 2024)

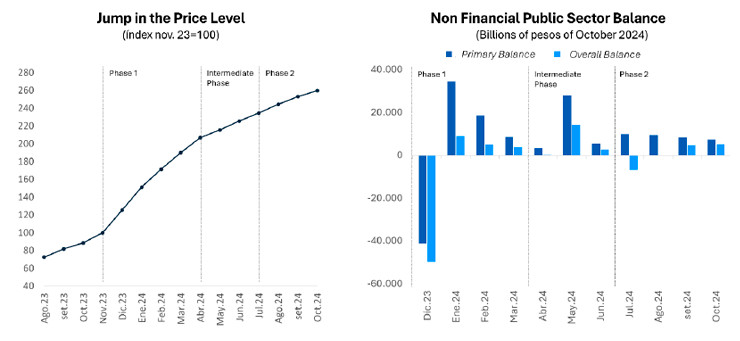

The stabilization plan was initiated in December 2023, immediately following President Milei’s inauguration, and commenced with a dramatic 100% devaluation of the official exchange rate. This was accompanied by simultaneous adjustments to public utility rates and the liberalization of previously controlled prices. These measures collectively triggered a significant surge in the general price level. The Consumer Price Index (CPI) doubled within just five months, from December 2023 to April 2024, as illustrated in Figure 2.

Figure 2. Jump in the price level and fiscal adjustment

Figure 2. Jump in the price level and fiscal adjustment

Figure 2. Jump in the price level and fiscal adjustment

Source: INDEC, Ministry of Finance.

As shown in Figure 2, this inflationary period was coupled with a remarkably stringent fiscal adjustment. This fiscal tightening was partially facilitated by the erosion of the real value of primary expenditures due to the rapid increase in prices. Consequently, the fiscal balance of the non-financial public sector shifted from a substantial annual deficit of nearly 5% of GDP in 2023 to a surplus by January 2024. This surplus has been maintained consistently and is projected by markets to persist through 2025.

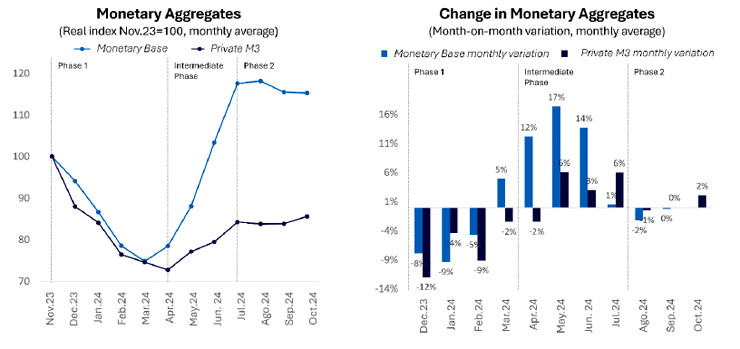

The surge in prices also precipitated a sharp contraction in the economy’s liquidity. Between December 2023 and April 2024, the BCRA’s monetary base contracted by 35% in real terms, while broader money supply measures (M3) decreased by 27%, as depicted in Figure 3.

Figure 3. Liquidity of the economy

Figure 3. Liquidity of the economy

Figure 3. Liquidity of the economy

Note: private M3 is a broad monetary aggregate in pesos that includes currency held by the public, outstanding checks in pesos and total deposits in pesos of the non-financial private sector. Source: BCRA.

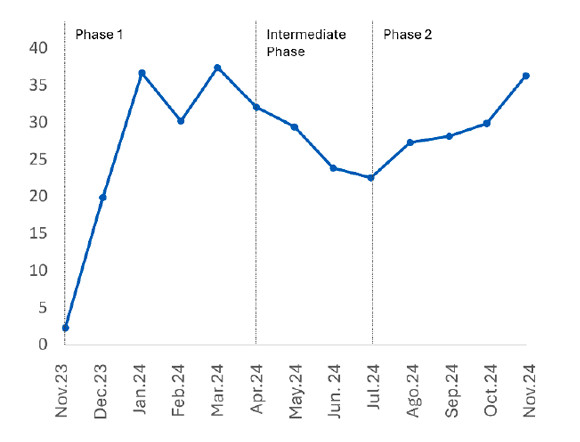

This contraction in liquidity led to a dramatic increase in the opportunity cost of holding liquid money, which is considered a conceptually robust measure of market liquidity. The spread between interest rates charged by banks on personal loans and the rate on the BCRA’s liquidity management instruments widened significantly, from an average of 2 percentage points in November 2023 to an average of 30 percentage points between December 2023 and April 2024, as illustrated in Figure 4.

Figure 4. Opportunity cost of holding money (spread between personal loan rate and the BCRA’s interest rate, in %)

Figure 4. Opportunity cost of holding money (spread between personal loan rate and the BCRA

Figure 4. Opportunity cost of holding money (spread between personal loan rate and the BCRA

Note: a higher level indicates greater illiquidity. Source: the authors based on BCRA data.

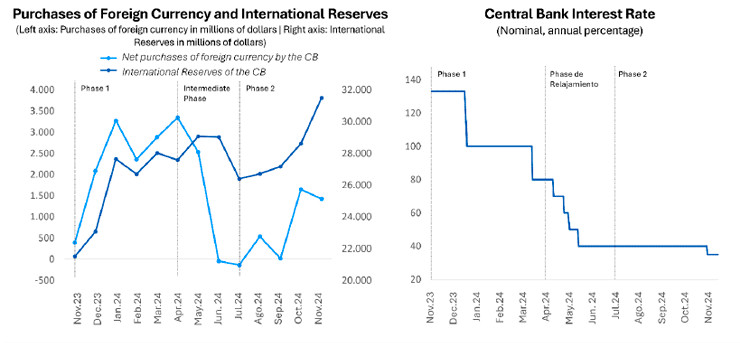

The severe reduction in peso-denominated liquidity had several key effects. Firstly, it incentivized markets to sell dollars to the BCRA in exchange for the now scarcer pesos. This resulted in a substantial increase in Argentina’s international reserves during this initial phase. Gross reserves rose from US$22 billion in November 2023 to US$28 billion by April 2024, marking a 28% increase. Secondly, this liquidity contraction allowed the BCRA to reduce the interest rate it offered on its interest-bearing liabilities, from a nominal annual rate of 133% to 80% between December 2023 and April 2024. This reduction was viable because the increased scarcity of Central Bank liquidity, of which these liabilities are a part, made it more valuable.

Figure 5. International reserves and BCRA interest rate

Figure 5. International reserves and BCRA interest rate

Figure 5. International reserves and BCRA interest rate

Source: BCRA.

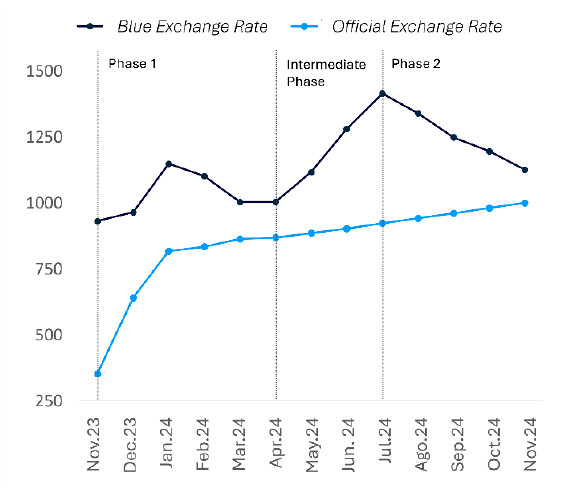

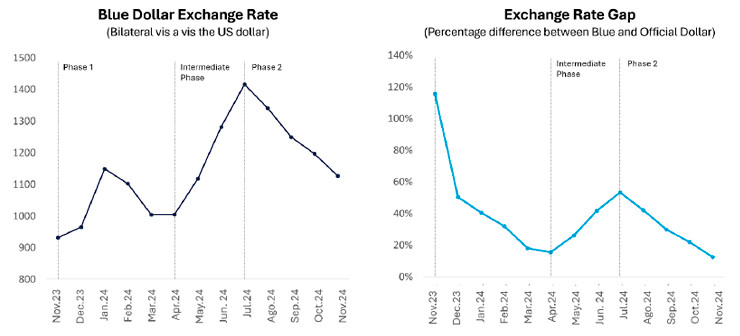

This phase of severe economic illiquidity also led to the stabilization of the blue dollar exchange rate and a significant contraction of the exchange rate gap between the blue dollar and the official dollar. This gap decreased dramatically from an average of 120% in November 2023 to just 20% by April 2024.

Figure 6. Blue exchange rate and exchange rate gap

Figure 6. Blue exchange rate and exchange rate gap

Figure 6. Blue exchange rate and exchange rate gap

Fuente: BCRA.

Concurrently, the contractionary fiscal and monetary policies induced a sharp decline in overall economic activity and a deceleration of the inflation rate. The Monthly Economic Activity Indicator (EMAE), a leading index for quarterly GDP growth rates, fell by 4% between November 2023 and April 2024. Over the same period, monthly inflation decreased from 13% in November 2023 to 4.2% by May 2024.

Figure 7. Macroeconomic outcomes

Source: BCRA, INDEC.

Intermediate Phase: Monetary Easing (April – July 2024)

Between April and July 2024, Argentina experienced an intermediate phase characterized by monetary easing, resulting in a significant expansion of liquidity within the economy, as evidenced by increases in both the monetary base and M3 (Figure 3).

This shift towards monetary easing was likely propelled by a rapid series of interest-rate cuts implemented by the BCRA. The nominal annual interest rate was reduced from 80% at the end of April to 40% by mid-May 2024. Additionally, the initiation of a program to replace BCRA interest-bearing liabilities (pases) with LECAPs contributed to liquidity expansion, as the cancellation of BCRA liabilities was not perfectly synchronized with the absorption of pesos through the issuance of LECAPs.

During this phase, the opportunity cost of holding liquid money decreased by 10 percentage points (1,000 basis points). This monetary easing triggered a sharp increase in the parallel dollar exchange rate, which surged to 1,600 pesos per dollar by July. Consequently, the exchange rate gap widened again to 60%. Furthermore, BCRA dollar purchases plummeted to near zero, international reserves weakened, and the downward trend in inflation was interrupted, remaining above 4% through July 2024.

However, this period of monetary easing coincided with the beginning of a recovery in economic activity (see Figures 4 to 7), suggesting a potential trade-off between controlling inflation and fostering economic growth in the short term.

Phase 2: “Closing the Taps” (July – October 2024)

The government announced Phase 2 of its economic plan in late June and implemented it fully throughout July 2024. Reinforcing its commitment to fiscal balance and the 2% monthly devaluation of the official exchange rate, along with maintaining exchange controls, the primary objective of Phase 2 was to tighten monetary policy by eliminating all remaining sources of monetary expansion. Key measures included:

- Elimination of BCRA Interest-Bearing Liabilities: These liabilities were exchanged for LECAPs and LeFip, transferring the responsibility for interest and principal payments to the National Treasury.

- Buyback of Put Options Held by the Financial System: The stock of put options represented a contingent claim on BCRA’s monetary base and a potential source of monetary expansion. Buying them back removed this risk.

- Sterilization of Peso Issuance from Dollar Purchases: Peso issuance resulting from BCRA dollar purchases in the official exchange market was sterilized through dollar sales in the Cash with Settlement market (Contador con Liquidación or CCL), which operates at rates similar to the blue dollar.

The combination of a sustained fiscal surplus, the elimination of monetary expansion sources by the BCRA, and a relatively high monetary policy interest rate (40% at the start of Phase 2, later reduced to 35%, and subsequently to 32%) relative to the 2% monthly devaluation rate, created very attractive dollar-equivalent yields on peso-denominated instruments. For example, a 35% nominal annual interest rate combined with a 2% monthly devaluation of the official exchange rate translates to an approximate annual dollar yield of 12%. This set of measures effectively halted liquidity growth, whether measured by base money or M3 (Figure 3).

The effects of halting liquidity growth were immediate and significant. The opportunity cost of holding liquid money increased by almost 15 percentage points (1,500 basis points) between July and October 2024. The BCRA resumed dollar purchases in the official market, substantially increasing its international reserves, which surpassed US$30 billion. The blue dollar exchange rate dropped significantly, nearly eliminating the gap with the official rate. Inflation decreased to below 4% monthly in September and further to below 3% monthly in October. Although economic expansion slowed, bank credit to the private sector continued to grow.

While external factors such as expectations of a new agreement with the IMF and global market trends undoubtedly played a role, this analysis of the monetary and exchange rate history of Argentina’s stabilization plan indicates that, supported by fiscal discipline, the monetary and exchange rate policy framework has been effective in both anchoring market expectations and influencing key macroeconomic variables related to the “argentina money exchange rate”.

Achievements and Costs of the Stabilization Plan

The monetary and exchange rate policy implemented as part of Argentina’s stabilization plan has yielded several significant achievements. It has successfully aligned devaluation expectations with the BCRA’s policy announcements, effectively reducing the exchange-rate gap between the parallel and official rates to near zero. Furthermore, the plan has facilitated the accumulation of international reserves and achieved a drastic reduction in inflation, consistently outperforming market projections.

However, these advancements have not come without considerable costs. The stabilization measures have led to a significant reduction in real incomes and an initial contraction in economic activity, which is a typical consequence of stabilization programs that commence with severe monetary tightening. This economic downturn has, unfortunately, resulted in an increase in poverty levels across Argentina.

Challenges and the Future of Argentina’s Exchange Rate Policy

Looking ahead, the critical challenge for Argentina is to dismantle the existing exchange controls (“cepo”) and transition towards a more normalized monetary and exchange rate regime. This transition must consolidate the gains already achieved in stabilizing the economy while fostering a robust and sustainable economic recovery.

The effectiveness of the hybrid monetary and exchange rate framework in anchoring market expectations and influencing key macroeconomic variables offers valuable insights for designing the post-“cepo” monetary and exchange rate regime. Careful consideration of these lessons will be crucial in navigating the path towards economic normalization and ensuring long-term stability for the “argentina money exchange rate” and the Argentine economy as a whole.

Conclusions

Argentina’s stabilization plan employs a sophisticated monetary and exchange rate policy, expertly combining a predetermined official exchange rate with a market-driven floating exchange rate in the parallel market. This framework integrates traditional monetary policy tools with exchange rate controls to manage the complexities of the “argentina money exchange rate”.

Supported by a strong fiscal surplus and a comprehensive cleanup of the BCRA’s balance sheet, effectively eliminating the quasi-fiscal deficit, the plan has met key objectives. These include aligning devaluation expectations, dramatically reducing the exchange rate gap, accumulating crucial international reserves, and achieving a significant and sustained reduction in inflation.

Despite these successes, the path to stabilization has incurred costs, notably a reduction in incomes and an initial contraction in economic activity, leading to increased poverty. The effectiveness of the current hybrid system provides valuable lessons as Argentina looks to the future, aiming to dismantle capital controls and establish a stable, normalized monetary and exchange rate regime that can underpin a robust and lasting economic recovery.

References

[1] The authors thank Pablo Ottonello for having pointed this to them.

[2] The holder of a put has the right to sell (although not the obligation) Treasury Bills and Notes to the BCRA at a given price and for a predetermined period if their value falls below the price established in the put contract. To have an idea of magnitudes prior to the voluntary exchange operation, if all banks simultaneously exercised their right (something they can do at any time within the period established in the put contract) the BCRA would have had to issue the equivalent of an entire monetary base.

[3] The BCRA can handle this form of sterilisation at its discretion.