Can A Beneficiary Withdraw Money From A Trust? Yes, a beneficiary might be able to access trust funds, but it hinges on the specifics outlined in the trust document, along with various financial and monetary factors. At money-central.com, we break down these complexities, providing clarity on trust management and asset distribution to guide you through navigating the nuances of estate planning.

Let’s explore the different conditions that affect the release of funds from a trust, making sure you fully grasp your rights and responsibilities with respect to trusts and estate planning. This includes understanding the role of the trustee, the types of trusts involved, and the legal framework governing trust administration, all of which impact your ability to benefit from a trust effectively, including financial planning and wealth management.

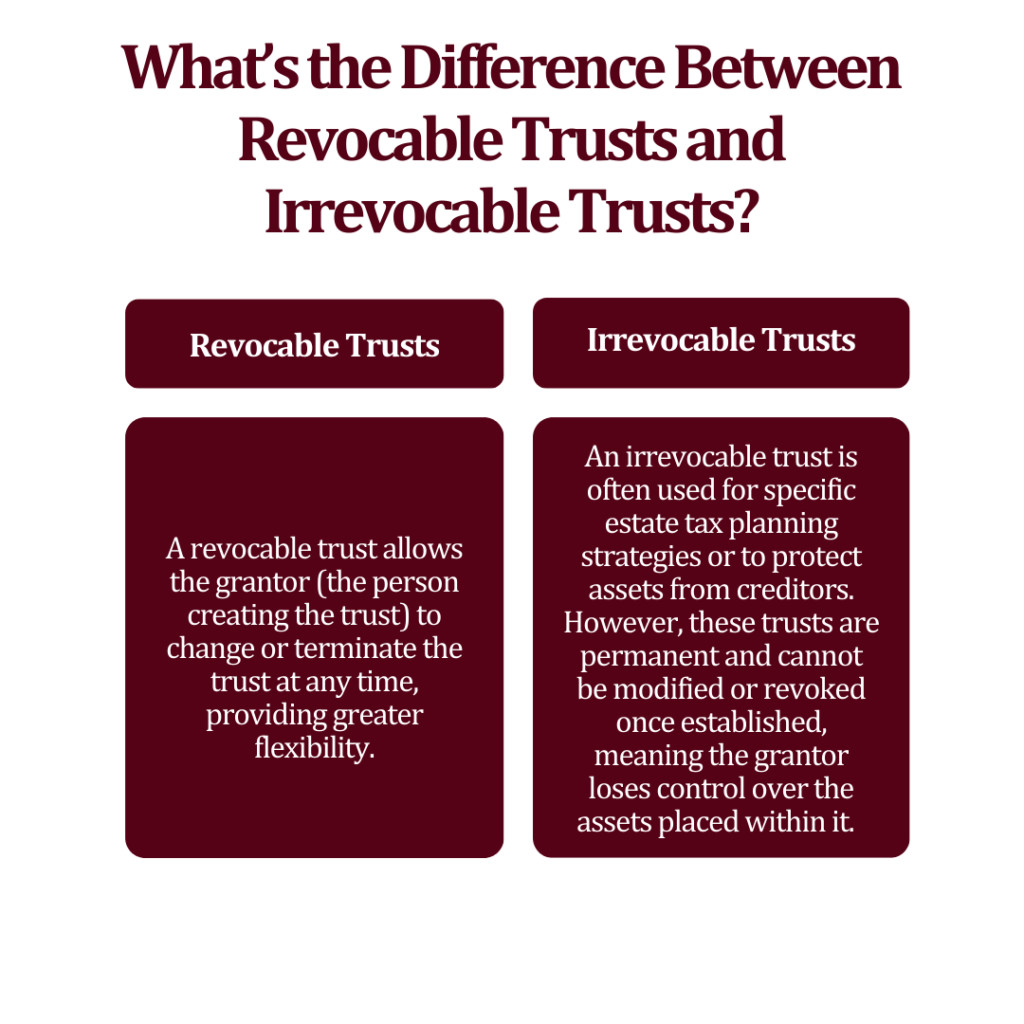

1. Understanding Trusts: Revocable vs. Irrevocable

Before diving into who can withdraw money from a trust, it’s vital to understand the fundamental difference between revocable and irrevocable trusts. Knowing the difference is key to managing your finances with money-central.com.

-

Definition of a Trust: A trust is a legal arrangement where a grantor (also known as a settlor or trustor) transfers assets to a trustee, who manages them for the benefit of beneficiaries.

-

Revocable Trust:

- Flexibility: The grantor can modify or terminate the trust during their lifetime.

- Control: The grantor typically acts as the trustee, maintaining control over the assets.

- Purpose: Often used to avoid probate and manage assets during the grantor’s lifetime.

- Example: Imagine John creates a revocable trust, naming himself as trustee. He can change the beneficiaries, add or remove assets, or even dissolve the trust at any time.

-

Irrevocable Trust:

- Permanence: Once established, the terms of the trust cannot be easily changed or terminated.

- Loss of Control: The grantor generally relinquishes control over the assets to the trustee.

- Purpose: Used for tax planning, asset protection, and ensuring assets are managed according to specific wishes.

- Example: Sarah creates an irrevocable trust to protect her assets from potential creditors. Once the trust is established, she cannot alter its terms or reclaim the assets.

A graphic detailing the difference between revocable trusts and irrevocable trusts, which is key to knowing how to get your money out of a trust fund.

A graphic detailing the difference between revocable trusts and irrevocable trusts, which is key to knowing how to get your money out of a trust fund.

2. When Does a Revocable Trust Become Irrevocable?

A revocable trust typically becomes irrevocable upon the death or incapacitation of the grantor, aligning with their estate planning arrangements.

- Death of the Grantor: This is the most common scenario. Once the grantor passes away, the revocable trust becomes irrevocable, and its terms can no longer be altered.

- Example: When John, the grantor of a revocable trust, dies, his trust automatically converts into an irrevocable trust.

- Incapacitation of the Grantor: If the grantor becomes incapacitated and unable to manage their affairs, the trust may become irrevocable to protect their assets.

- Example: If Sarah becomes mentally incapacitated due to a severe illness, her revocable trust might become irrevocable to ensure her assets are managed according to her original intentions.

- Grantor’s Decision: A grantor can choose to make their revocable trust irrevocable at any time during their life.

- Example: Michael decides to convert his revocable trust into an irrevocable trust to take advantage of certain tax benefits and shield his assets from potential creditors.

3. Purpose of an Irrevocable Trust

Irrevocable trusts offer several key benefits, making them a valuable tool in estate and financial planning.

- Asset Protection: Shielding assets from creditors, lawsuits, and potential financial risks.

- Tax Benefits: Reducing estate taxes by removing assets from the grantor’s taxable estate.

- Medicaid Eligibility: Protecting assets while qualifying for Medicaid benefits.

- Estate Planning: Ensuring assets are distributed according to the grantor’s wishes after their death.

3.1. Specific Situations for Irrevocable Trusts

Certain life situations make irrevocable trusts particularly beneficial:

- High Net Worth Individuals: Those with estates exceeding the estate tax threshold use irrevocable trusts to minimize tax liabilities.

- Professionals at Risk of Lawsuits: Doctors, lawyers, and business owners use these trusts to protect personal assets from potential legal judgments.

- Individuals with Large Debts: Irrevocable trusts can safeguard assets from creditors.

- Families with Special Needs Dependents: Ensuring continued support without disqualifying them from government benefits.

- Charitable Intentions: Facilitating planned charitable donations as part of estate planning.

3.2. Are Irrevocable Trusts Protected from Creditors?

Yes, assets held in an irrevocable trust are generally protected from creditors because the grantor no longer owns them directly.

- Transfer of Ownership: Once assets are transferred to the trust, they are no longer considered the grantor’s property.

- Legal Protection: Creditors cannot typically reach assets held in the trust to satisfy debts or legal judgments against the grantor.

- Fraudulent Transfers: However, transfers made with the intent to defraud creditors can be challenged in court.

- Example: If John transfers assets to an irrevocable trust shortly before declaring bankruptcy, a court might view this as a fraudulent transfer and allow creditors to access those assets.

3.3. Irrevocable Trusts and Lawsuits

Irrevocable trusts can shield assets from lawsuits by removing them from the grantor’s direct control.

- Protection from Judgments: Assets in the trust are not subject to legal judgments against the grantor.

- Third-Party Ownership: The trust, as a separate legal entity, owns the assets, providing a layer of protection.

- Professional Advice: Setting up such a trust requires careful planning and legal advice to ensure it complies with all applicable laws.

3.4. Irrevocable Trusts and Nursing Homes

Irrevocable trusts, especially Medicaid Asset Protection Trusts, can protect assets from nursing home costs.

- Medicaid Eligibility: Assets in the trust are not counted when determining Medicaid eligibility, helping individuals qualify for long-term care benefits.

- Look-Back Period: Many states have a “look-back period,” meaning assets transferred into the trust within a certain timeframe before applying for Medicaid can still be counted.

- Example: California has a look-back period of 30 months for transfers made before July 1, 2024, and 60 months for transfers made on or after that date.

- Strategic Planning: It is crucial to set up these trusts well in advance to comply with legal guidelines and plan strategically.

According to research from the National Bureau of Economic Research in February 2024, strategic planning helps ensure compliance with legal guidelines, and failing to comply with legal guidelines could disqualify individuals from receiving Medicaid benefits.

4. Tax Implications of Irrevocable Trusts

Irrevocable trusts are separate tax-paying entities, and understanding their tax implications is crucial for both trustees and beneficiaries.

- Trust Income: The trust pays taxes on any income it generates.

- Beneficiary Distributions: Beneficiaries pay taxes on the distributions they receive from the trust.

- Tax Returns: Trustees must file tax returns on behalf of the trust and use trust funds to pay any taxes owed.

4.1. Who Pays Tax on Irrevocable Trust Income?

The trustee is responsible for paying taxes on the income generated by the trust.

- Fiduciary Duty: It is part of the trustee’s fiduciary duty to manage the trust’s finances responsibly, including paying taxes.

- Tax Payment: The trustee uses trust funds to pay the taxes owed, ensuring compliance with tax laws.

- Professional Assistance: Trustees often hire tax professionals to help them navigate the complex tax rules and prepare accurate returns.

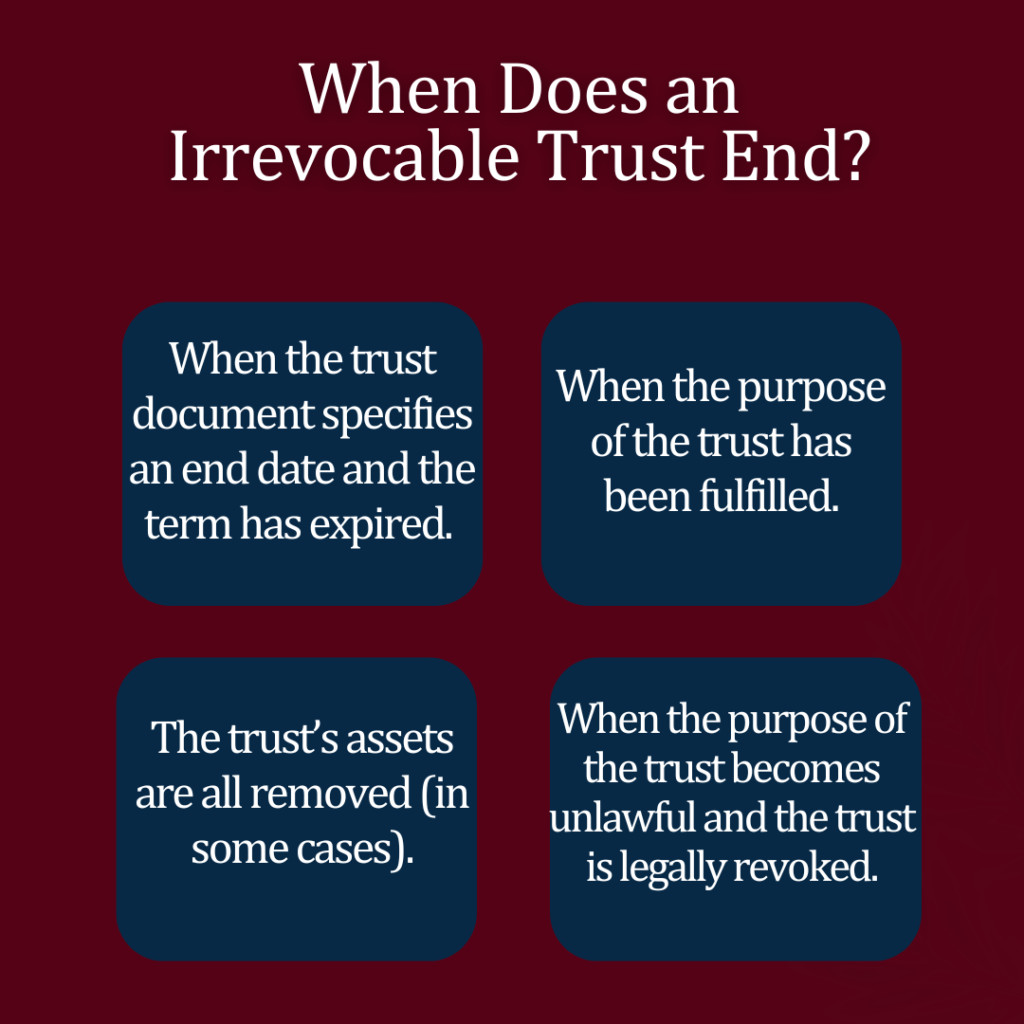

4.2. When Does an Irrevocable Trust End?

Under California law, an irrevocable trust typically terminates under the following conditions:

- Specified End Date: The trust document specifies an end date, and that date has arrived.

- Purpose Fulfilled: The purpose of the trust has been achieved.

- Unlawful Purpose: The purpose of the trust becomes unlawful.

- Asset Depletion: The trust’s assets are completely distributed (in some cases).

A graphic that illustrates the answer to, When does an irrevocable trust end?

A graphic that illustrates the answer to, When does an irrevocable trust end?

5. Can a Beneficiary Withdraw Money From a Trust?

Whether a beneficiary can withdraw money from a trust depends on the terms outlined in the trust document and their role within the trust.

- Trustee’s Role:

- Trustees can withdraw money from the trust to cover expenses related to trust administration, such as funeral costs, property repairs, debt repayment, distributions to beneficiaries, administrative fees, and investments.

- Beneficiary’s Role:

- Generally, beneficiaries cannot directly withdraw money from an irrevocable trust. They must wait for the trustee to make distributions.

- Exceptions: Some trust documents may include language allowing beneficiaries to withdraw money under specific conditions.

According to research from the American Bar Association in August 2022, whether a beneficiary can get money from a trust depends entirely on their circumstances, emphasizing the importance of specific terms in the trust document.

5.1. How to Access Trust Funds

Accessing trust funds depends on your relationship to the trust:

- Trustees:

- Trustees typically have access to a bank account set up for the trust, allowing them to withdraw cash, write checks, and make wire transfers.

- Beneficiaries:

- Beneficiaries usually need to request money from the trustee or wait until the trustee makes distributions after settling debts and taxes.

- Communication: Clear communication between the trustee and beneficiaries is essential for a smooth distribution process.

5.2. Early Access to Trust Funds

Gaining early access to trust funds requires specific steps:

- Written Request: Submit a formal written request to the trustee.

- Trustee’s Discretion: The trustee’s decision to comply depends on whether they have fulfilled their fiduciary duties and the terms of the trust.

- Court Petition: In some cases, you may file a petition with the court to compel the trustee to distribute funds.

- Legal Advice: Consulting with a trust lawyer is crucial to determine the best course of action.

6. Acceptable and Unacceptable Withdrawals

Understanding what constitutes acceptable and unacceptable withdrawals is vital for trustees to avoid misconduct and legal issues.

- Acceptable Withdrawals:

- Funeral expenses

- Repairs on property owned by the trust

- Debt repayment

- Distributions to beneficiaries

- Administrative fees

- Investments that benefit the trust

- Unacceptable Withdrawals:

- Borrowing or using funds for personal reasons not outlined in the trust.

- Mismanaging funds.

- Using the trust as a personal “piggy bank.”

According to research from the American Academy of Estate Planning Attorneys in September 2023, trustees must not mismanage funds; if they do, they may face being held liable for mistakes.

7. Key Roles: Beneficiary vs. Trustee

Understanding the roles of beneficiaries and trustees is essential for navigating trust administration.

7.1. Can a Beneficiary Withdraw Money from a Trust?

Whether a beneficiary can withdraw money depends on the trust document and the trustee’s decisions.

- Trust Document: The trust document specifies whether beneficiaries have withdrawal rights and under what conditions.

- Trustee’s Discretion: The trustee has the power to decide when and how to distribute funds, following the trust’s terms.

- Same Person: If the beneficiary and trustee are the same person, they can withdraw money but must still uphold their fiduciary duty.

7.2. Can a Trustee Withdraw Money for Personal Use?

Generally, a trustee cannot use trust funds for personal use unless explicitly permitted by the trust document and for the benefit of the trust and beneficiaries.

- Fiduciary Duty: Trustees have a fiduciary duty to act in the best interests of the beneficiaries.

- Permissible Expenses: Trustees can use trust funds to pay for expenses related to trust administration, property management, and distributions.

- Compensation: Trustees are entitled to compensation for their work, paid directly from trust assets, but this must be reasonable and documented.

7.3. Borrowing from a Trust

Borrowing from a trust is generally discouraged and subject to strict scrutiny.

- Potential Risks: Even if the trust document allows it, borrowing from the trust can be seen as a breach of fiduciary duty.

- Legal and Financial Liability: Trustees could be held legally and financially liable for such actions.

- Legal Consultation: Always consult with an attorney before borrowing money from a trust, especially if you are the trustee.

7.4. Can a Grantor Withdraw Money from an Irrevocable Trust?

Settlors typically cannot withdraw money from an irrevocable trust unless specific language in the trust document grants them special permissions.

- Loss of Control: Once the trust is established, the settlor generally loses the ability to control the assets.

- Potential Scrutiny: Any withdrawals by the settlor will be subject to intense scrutiny and could lead to litigation.

8. How a Trustee Withdraws Money From a Trust

Trustees can withdraw money from a trust whenever needed but must ensure they are using the funds for the benefit of the trust and beneficiaries.

- Bank Account: Trustees typically establish a bank account specifically for the trust.

- Transaction Records: They must meticulously document every transaction, including transfers, withdrawals, and payments.

- Trust Accounting: Trustees must prepare and submit a trust accounting annually, providing a comprehensive overview of all transactions.

8.1. Withdrawing Cash

Trustees can withdraw cash from a trust account to cover expenses related to trust administration.

8.2. Transferring Money

Money can be transferred from a trust account similarly to a regular bank account.

- Bank Information: Have the receiving party’s bank information readily available.

- Online Banking: Check with the bank to see if online or mobile banking is available for easier transfers.

- Detailed Records: Keep detailed records of all transfers for trust accounting purposes.

8.3. Where to Withdraw

Trustees can withdraw money from a trust bank account by visiting a bank or using an ATM. Contact the financial institution to determine which ATMs can be used for these transactions.

9. Power of Attorney and Irrevocable Trusts

A general power of attorney typically cannot create an irrevocable trust unless specifically authorized.

- California Probate Code Section 4264: A power of attorney can grant the power to create, modify, revoke, or terminate a trust.

- Legal Guidance: Work with a lawyer to create a legally binding document that grants this authority.

10. Selecting the Best Trustee for an Irrevocable Trust

Choosing the right trustee is crucial for the successful management of an irrevocable trust.

- Essential Skills and Traits:

- Integrity

- Impartiality

- Interpersonal skills

- Communication skills

- Financial acumen

- Organizational skills

- Decision-making

- Knowledge of trust law

- Tax knowledge

- Real estate savvy

- Investment knowledge

- Time Commitment: Managing a trust is a full-time job, requiring significant time and attention.

- Professional Trustee: Hiring a professional trustee ensures expertise, impartiality, and compliance with fiduciary duties.

At money-central.com, we understand that managing finances and trusts can be daunting. Whether you’re exploring investment options or managing trust accounts, our platform offers comprehensive resources to guide you every step of the way. For personalized advice and expert solutions, consider scheduling a consultation to ensure your financial future is secure and well-managed.

FAQ: Can a Beneficiary Withdraw Money From a Trust?

- Can a beneficiary withdraw money from a trust?

- Yes, under certain conditions specified in the trust document.

- What is the difference between a revocable and irrevocable trust?

- A revocable trust can be modified or terminated, while an irrevocable trust generally cannot.

- When does a revocable trust become irrevocable?

- Typically, upon the death or incapacitation of the grantor.

- Are assets in an irrevocable trust protected from creditors?

- Yes, generally, but transfers made to defraud creditors can be challenged.

- Who pays taxes on irrevocable trust income?

- The trustee is responsible for paying taxes on the income generated by the trust.

- Can a trustee withdraw money from a trust for personal use?

- No, unless explicitly permitted by the trust document and for the benefit of the trust and beneficiaries.

- What skills and traits should a trustee possess?

- Integrity, impartiality, financial acumen, and knowledge of trust law, among others.

- Can a grantor withdraw money from an irrevocable trust?

- Generally, no, unless the trust document grants them special permissions.

- How does a trustee withdraw money from a trust?

- By establishing a bank account for the trust and meticulously documenting all transactions.

- What are acceptable withdrawals from a trust?

- Expenses related to trust administration, property management, and distributions to beneficiaries.

Unlock Financial Clarity with Money-Central.Com

Navigating the world of trusts, estate planning, and financial management can feel overwhelming. At money-central.com, we’re dedicated to providing clear, actionable insights and resources to help you take control of your financial future.

Ready to take the next step?

- Explore our comprehensive articles and guides on trusts, investments, retirement planning, and more.

- Use our interactive tools and calculators to plan your budget, estimate your retirement savings, and assess your investment risk tolerance.

- Connect with our network of financial advisors for personalized guidance and support tailored to your unique needs.

Visit money-central.com today and discover how we can help you achieve your financial goals with confidence. Address: 44 West Fourth Street, New York, NY 10012, United States. Phone: +1 (212) 998-0000.

Don’t wait – start building a secure financial foundation for yourself and your loved ones today.