Can I Withdraw Money From Hsa For Personal Use? Yes, you can withdraw money from your Health Savings Account (HSA) for personal use, but it’s essential to understand the tax implications and potential penalties involved, as explained by money-central.com. An HSA offers a tax-advantaged way to save and pay for healthcare expenses, but using funds for non-qualified expenses can trigger taxes and penalties, so it’s important to understand the qualified medical expenses, tax advantages, and withdrawal rules to make informed decisions about managing your HSA funds and personal finances. For more detailed guidance, explore HSA eligibility, contribution limits, and investment options available on money-central.com, empowering you to make the most of your HSA.

1. What is an HSA and How Does it Work?

A Health Savings Account (HSA) is a tax-advantaged savings account that can be used for healthcare expenses. It is available to individuals who have a High Deductible Health Plan (HDHP). HSAs offer a triple tax advantage: contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free. This makes them a powerful tool for managing healthcare costs and saving for the future. It’s like having a financial first-aid kit specifically for your health.

- Eligibility: To be eligible for an HSA, you must have an HDHP, not be covered by other non-HDHP health insurance, and not be claimed as a dependent on someone else’s tax return.

- Contributions: You, your employer, or both can contribute to your HSA. There are annual contribution limits set by the IRS, which vary based on whether you have individual or family coverage.

- Investments: Many HSAs allow you to invest your contributions, giving you the opportunity to grow your savings over time.

- Withdrawals: Withdrawals for qualified medical expenses are tax-free and penalty-free. Withdrawals for non-qualified expenses are subject to income tax and, if you’re under age 65, a 20% penalty.

2. Can I Use My HSA for Non-Medical Expenses?

Yes, you can use your HSA funds for non-medical expenses, but there are consequences. Before age 65, withdrawals for non-qualified expenses are subject to income tax and a 20% penalty. After age 65, withdrawals for non-qualified expenses are subject to income tax, but the 20% penalty no longer applies.

- Before Age 65: If you withdraw money from your HSA for non-medical expenses before you turn 65, the withdrawn amount is subject to income tax, and you’ll also have to pay a 20% penalty. This can significantly reduce the amount of money you receive and make it a costly option.

- After Age 65: Once you reach age 65, the penalty for non-qualified withdrawals is waived. However, the withdrawn amount is still subject to income tax. This means that withdrawing funds for non-medical expenses will be taxed at your ordinary income tax rate.

- Qualified Medical Expenses: Understanding what qualifies as a medical expense is crucial. The IRS defines qualified medical expenses as those incurred for the diagnosis, cure, mitigation, treatment, or prevention of disease, or for the purpose of affecting any structure or function of the body. This includes a wide range of healthcare services and products.

3. What are Qualified Medical Expenses for HSA Withdrawals?

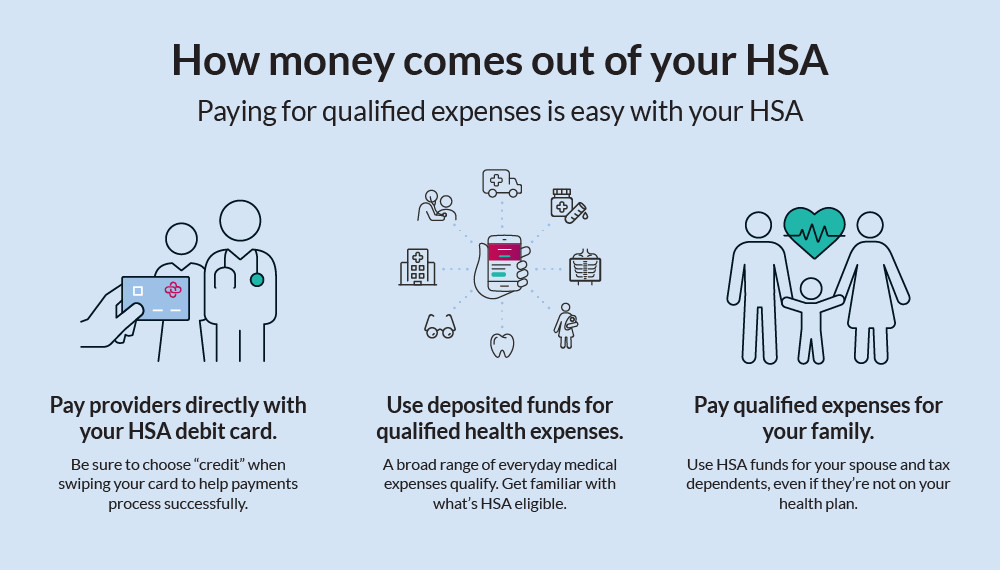

Qualified medical expenses include a broad range of healthcare costs that are tax-free when paid with HSA funds. This encompasses doctor visits, prescriptions, dental and vision care, and even certain over-the-counter items. Knowing what qualifies can help you maximize your HSA benefits.

- Common Qualified Expenses:

- Doctor visits and co-pays

- Prescription medications

- Dental care, including cleanings, fillings, and orthodontics

- Vision care, including eye exams, glasses, and contact lenses

- Chiropractic services

- Acupuncture

- Medical equipment, such as crutches and wheelchairs

- Mental health services

- Substance abuse treatment

- Over-the-Counter Items: As of 2020, over-the-counter medications and menstrual care products are considered qualified medical expenses. This change has expanded the range of items that can be purchased tax-free with HSA funds.

- Expenses for Dependents: You can also use your HSA to pay for qualified medical expenses for your spouse and dependents, even if they are not covered by your HDHP. This can be a significant benefit for families.

- IRS Publication 502: For a comprehensive list of qualified medical expenses, refer to IRS Publication 502, which provides detailed guidance on what expenses are eligible for tax-free treatment.

HSA eligible expenses illustration

HSA eligible expenses illustration

4. What are Non-Qualified Medical Expenses?

Non-qualified medical expenses are those that do not meet the IRS definition of qualified medical expenses. Using HSA funds for these expenses results in taxes and penalties if you are under 65. Common examples include cosmetic surgery, non-prescription medications (prior to 2020), and health insurance premiums (with some exceptions).

- Cosmetic Surgery: Cosmetic surgery is generally not considered a qualified medical expense unless it is necessary to improve a deformity arising from, or directly related to, a congenital abnormality, a personal injury resulting from an accident or trauma, or a disfiguring disease.

- Non-Prescription Medications (prior to 2020): Before 2020, non-prescription medications were not considered qualified medical expenses unless they were prescribed by a doctor. However, the CARES Act of 2020 changed this, allowing over-the-counter medications to be considered qualified expenses.

- Health Insurance Premiums: Health insurance premiums are generally not qualified medical expenses, with a few exceptions. You can use HSA funds to pay for COBRA premiums, health insurance premiums while receiving unemployment compensation, and Medicare premiums (but not Medigap premiums).

- Other Non-Qualified Expenses: Other examples of non-qualified expenses include funeral expenses, teeth whitening, and weight loss programs (unless prescribed by a doctor for a specific medical condition).

5. How Does Age Affect HSA Withdrawals for Personal Use?

Age plays a significant role in how HSA withdrawals for personal use are taxed and penalized. Before age 65, non-qualified withdrawals are subject to both income tax and a 20% penalty. After age 65, the penalty is waived, but the withdrawn amount is still subject to income tax.

- Under Age 65: If you’re under 65 and withdraw money from your HSA for non-qualified expenses, you’ll face a double whammy: income tax on the withdrawn amount and a 20% penalty. This can make it a very expensive way to access your HSA funds.

- Age 65 and Older: Once you turn 65, the 20% penalty for non-qualified withdrawals is waived. However, the withdrawn amount is still subject to income tax. At this point, your HSA functions more like a traditional retirement account, where withdrawals are taxed as ordinary income.

- Medicare Enrollment: Enrolling in Medicare can affect your ability to contribute to an HSA. Once you enroll in Medicare, you are no longer eligible to contribute to an HSA. However, you can still use the funds in your HSA for qualified medical expenses.

6. What are the Tax Implications of HSA Withdrawals for Personal Use?

The tax implications of using HSA funds for personal use depend on whether the expenses are qualified or non-qualified. Qualified medical expenses are tax-free, while non-qualified expenses are subject to income tax and, if you’re under 65, a 20% penalty. Understanding these tax rules is crucial for managing your HSA effectively.

- Qualified Medical Expenses: When you use your HSA funds to pay for qualified medical expenses, the withdrawals are tax-free. This means you don’t have to pay income tax on the withdrawn amount, and you don’t have to pay any penalties.

- Non-Qualified Expenses (Under 65): If you’re under 65 and use your HSA funds for non-qualified expenses, the withdrawn amount is subject to income tax, and you’ll also have to pay a 20% penalty. This can significantly reduce the amount of money you receive and make it a costly option.

- Non-Qualified Expenses (Age 65 and Older): Once you reach age 65, the penalty for non-qualified withdrawals is waived. However, the withdrawn amount is still subject to income tax. This means that withdrawing funds for non-medical expenses will be taxed at your ordinary income tax rate.

- Reporting HSA Withdrawals: You’ll need to report your HSA withdrawals on your tax return using Form 8889, Health Savings Accounts (HSAs). This form helps you calculate your HSA deduction, report contributions, and determine the taxability of withdrawals.

7. How Can I Avoid Penalties on HSA Withdrawals?

To avoid penalties on HSA withdrawals, it’s essential to use your HSA funds only for qualified medical expenses. Keeping detailed records of your expenses and understanding the IRS guidelines can help you stay compliant and maximize the tax benefits of your HSA.

- Track Your Medical Expenses: Keep detailed records of all your medical expenses, including receipts, invoices, and explanations of benefits (EOBs) from your insurance company. This will help you prove that your withdrawals were for qualified medical expenses if you are ever audited by the IRS.

- Understand Qualified Expenses: Familiarize yourself with the IRS definition of qualified medical expenses. Refer to IRS Publication 502 for a comprehensive list of eligible expenses.

- Use HSA Funds Wisely: Only use your HSA funds for qualified medical expenses. If you’re not sure whether an expense qualifies, consult IRS Publication 502 or seek advice from a tax professional.

- Reimbursement Timing: You can reimburse yourself for qualified medical expenses at any time, even years after the expense was incurred, as long as the expense was incurred after the HSA was established. This gives you flexibility in managing your HSA funds.

8. What Happens to My HSA if I No Longer Have a High Deductible Health Plan (HDHP)?

If you no longer have an HDHP, you can no longer contribute to your HSA, but you can still use the funds in your account for qualified medical expenses. Your HSA remains your property, and the tax advantages continue to apply as long as you use the funds for eligible expenses.

- No Further Contributions: Once you lose your HDHP coverage, you can no longer make contributions to your HSA. This is because eligibility for an HSA is tied to having an HDHP.

- Continued Use for Qualified Expenses: Even if you can’t contribute to your HSA, you can still use the funds in your account to pay for qualified medical expenses. The tax-free nature of these withdrawals remains in effect.

- Investment Growth: Your HSA investments can continue to grow tax-free, even if you’re no longer contributing to the account. This allows you to continue building your healthcare savings over time.

- Alternative Healthcare Coverage: If you switch to a non-HDHP health plan, such as a PPO or HMO, you can still use your HSA funds for qualified medical expenses. However, you’ll want to consider how your new health plan coordinates with your HSA.

9. Can I Invest My HSA Funds?

Yes, many HSAs allow you to invest your funds, providing an opportunity for tax-free growth. Investment options typically include mutual funds, stocks, and bonds. Investing your HSA funds can be a powerful way to grow your healthcare savings over time, especially if you don’t need the funds for immediate medical expenses.

- Investment Options: Most HSA providers offer a range of investment options, including mutual funds, exchange-traded funds (ETFs), stocks, and bonds. The specific investment options available will depend on your HSA provider.

- Tax-Free Growth: The earnings on your HSA investments grow tax-free. This means you don’t have to pay taxes on any dividends, interest, or capital gains earned within the account.

- Risk Tolerance: Consider your risk tolerance when choosing investments for your HSA. If you have a long time horizon, you may be comfortable with more aggressive investments, such as stocks. If you’re closer to retirement or need the funds for near-term medical expenses, you may prefer more conservative investments, such as bonds.

- Professional Advice: If you’re not sure how to invest your HSA funds, consider seeking advice from a financial advisor. A financial advisor can help you develop an investment strategy that aligns with your goals and risk tolerance.

10. How Do I Withdraw Money From My HSA?

Withdrawing money from your HSA is typically a straightforward process. Most HSAs provide a debit card or checks that you can use to pay for qualified medical expenses directly. You can also submit receipts for reimbursement. The specific withdrawal process may vary depending on your HSA provider.

- Debit Card: Many HSAs provide a debit card that you can use to pay for qualified medical expenses at the point of sale. Simply swipe the card like you would any other debit card.

- Checks: Some HSAs also provide checks that you can use to pay for qualified medical expenses. Write a check to the healthcare provider or vendor, and be sure to keep a copy for your records.

- Reimbursement: If you pay for a qualified medical expense out-of-pocket, you can submit a receipt to your HSA provider for reimbursement. The HSA provider will then send you a check or deposit the funds directly into your bank account.

- Online Portal: Most HSA providers have an online portal where you can manage your account, track your expenses, and initiate withdrawals. The online portal can also provide helpful information about qualified medical expenses and HSA rules.

11. What are the Contribution Limits for HSAs?

The IRS sets annual contribution limits for HSAs, which vary based on whether you have individual or family coverage. These limits are adjusted each year for inflation. Understanding the contribution limits is crucial for maximizing your HSA savings.

| Year | Individual Coverage | Family Coverage | Catch-Up Contribution (Age 55+) |

|---|---|---|---|

| 2023 | $3,850 | $7,750 | $1,000 |

| 2024 | $4,150 | $8,300 | $1,000 |

- Catch-Up Contributions: Individuals age 55 and older can make additional catch-up contributions to their HSAs. The catch-up contribution limit is $1,000 per year.

- Excess Contributions: If you contribute more than the annual limit to your HSA, you may be subject to a 6% excise tax on the excess contributions. To avoid this penalty, be sure to track your contributions carefully and stay within the annual limits.

- Employer Contributions: Contributions made by your employer to your HSA count towards the annual contribution limits. If your employer contributes to your HSA, you’ll need to factor this into your contribution strategy.

- Coordination with Spouse: If you and your spouse both have HSA-eligible health plans, you can each contribute up to the individual contribution limit. However, if you are covered under the same family health plan, your combined contributions cannot exceed the family contribution limit.

12. Can I Transfer or Rollover Funds From One HSA to Another?

Yes, you can transfer or rollover funds from one HSA to another. This can be useful if you want to consolidate your accounts, take advantage of different investment options, or switch to a provider with lower fees. There are two main methods for moving funds between HSAs: rollovers and transfers.

- Rollovers: A rollover involves taking a distribution from your existing HSA and then contributing it to a new HSA within 60 days. You can only do one rollover per 12-month period.

- Transfers: A transfer involves directly moving funds from your existing HSA to a new HSA without you ever taking possession of the money. There are no limits on the number of transfers you can do per year.

- Direct vs. Indirect Rollovers: A direct rollover involves your existing HSA provider sending the funds directly to your new HSA provider. An indirect rollover involves your existing HSA provider sending you a check, which you then have to deposit into your new HSA within 60 days.

- Choosing the Right Method: Transfers are generally the preferred method for moving funds between HSAs, as they are more convenient and have no annual limits. However, rollovers can be useful if you need to access the funds temporarily or if your HSA provider doesn’t offer direct transfers.

13. What Happens to My HSA When I Die?

What happens to your HSA when you die depends on who you designate as your beneficiary. If you designate your spouse as your beneficiary, your HSA will become their HSA. If you designate someone else as your beneficiary, the HSA will be distributed to them, and the funds will be subject to income tax.

- Spouse as Beneficiary: If you designate your spouse as your beneficiary, your HSA will become their HSA upon your death. They can continue to use the funds for qualified medical expenses, and the tax advantages will remain in effect.

- Non-Spouse as Beneficiary: If you designate someone other than your spouse as your beneficiary, the HSA will be distributed to them upon your death. The funds will be subject to income tax at their ordinary income tax rate.

- Estate as Beneficiary: If you don’t designate a beneficiary, your HSA will become part of your estate. The funds will be subject to income tax and may also be subject to estate taxes.

- Estate Planning: It’s important to include your HSA in your estate planning to ensure that your wishes are carried out and that your beneficiaries receive the maximum benefit from the account.

14. How Does an HSA Compare to Other Savings Accounts?

An HSA offers unique tax advantages compared to other savings accounts, such as traditional savings accounts, 401(k)s, and IRAs. Understanding these differences can help you determine whether an HSA is the right choice for your financial situation.

- Tax Advantages: HSAs offer a triple tax advantage: contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free. This is a unique combination of tax benefits not found in other savings accounts.

- Traditional Savings Accounts: Traditional savings accounts offer no tax advantages. The interest earned on these accounts is subject to income tax.

- 401(k)s and IRAs: 401(k)s and traditional IRAs offer tax-deferred growth, meaning you don’t have to pay taxes on the earnings until you withdraw the money in retirement. However, withdrawals from these accounts are subject to income tax. Roth 401(k)s and Roth IRAs offer tax-free withdrawals in retirement, but contributions are not tax-deductible.

- Flexibility: HSAs offer more flexibility than other savings accounts. You can use the funds in your HSA for qualified medical expenses at any time, and you can invest the funds to grow your savings over time.

15. Are There Any Restrictions on How I Can Use My HSA Funds?

Yes, there are restrictions on how you can use your HSA funds. To avoid taxes and penalties, you must use the funds for qualified medical expenses. However, after age 65, you can use the funds for any purpose, although non-qualified withdrawals will be subject to income tax.

- Qualified Medical Expenses: The primary restriction on HSA funds is that they must be used for qualified medical expenses to avoid taxes and penalties. It’s important to understand the IRS definition of qualified medical expenses and to keep detailed records of your expenses.

- Age Restrictions: The age at which you withdraw funds from your HSA can affect the tax implications. Before age 65, non-qualified withdrawals are subject to both income tax and a 20% penalty. After age 65, the penalty is waived, but the withdrawn amount is still subject to income tax.

- Health Plan Restrictions: Your eligibility to contribute to an HSA is tied to having an HDHP. If you no longer have an HDHP, you can’t contribute to your HSA, but you can still use the funds in your account for qualified medical expenses.

- Investment Restrictions: Some HSA providers may have restrictions on the types of investments you can make with your HSA funds. Be sure to review the investment options and restrictions before investing your HSA funds.

16. What are the Benefits of Having an HSA?

Having an HSA offers numerous benefits, including tax savings, flexibility, and the ability to save for future healthcare expenses. These advantages make HSAs a valuable tool for managing healthcare costs and building financial security.

- Tax Savings: HSAs offer a triple tax advantage: contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free. This can result in significant tax savings over time.

- Flexibility: HSAs offer more flexibility than other savings accounts. You can use the funds in your HSA for qualified medical expenses at any time, and you can invest the funds to grow your savings over time.

- Portability: Your HSA is portable, meaning you can take it with you if you change jobs or health plans. This gives you control over your healthcare savings.

- Long-Term Savings: HSAs can be used as a long-term savings vehicle for healthcare expenses in retirement. By investing your HSA funds and allowing them to grow tax-free, you can build a substantial nest egg to cover future medical costs.

17. How to Choose the Right HSA Provider?

Choosing the right HSA provider is an important decision that can affect your ability to save and manage your healthcare expenses. Consider factors such as fees, investment options, and customer service when selecting an HSA provider.

- Fees: HSA providers may charge various fees, such as monthly maintenance fees, transaction fees, and investment fees. Compare the fees charged by different providers to find the most cost-effective option.

- Investment Options: If you plan to invest your HSA funds, consider the investment options offered by different providers. Look for a provider that offers a range of investment options that align with your risk tolerance and financial goals.

- Customer Service: Choose an HSA provider with a reputation for excellent customer service. You want to be able to easily contact the provider with questions or concerns.

- Online Tools: Look for an HSA provider that offers user-friendly online tools for managing your account, tracking your expenses, and initiating withdrawals.

18. What are Some Common Mistakes to Avoid With HSAs?

To maximize the benefits of your HSA and avoid potential pitfalls, it’s important to be aware of common mistakes. These include using HSA funds for non-qualified expenses, exceeding contribution limits, and failing to keep adequate records.

- Using Funds for Non-Qualified Expenses: One of the most common mistakes is using HSA funds for non-qualified expenses. This can result in taxes and penalties. Be sure to understand the IRS definition of qualified medical expenses and to use your HSA funds accordingly.

- Exceeding Contribution Limits: Exceeding the annual contribution limits for HSAs can result in a 6% excise tax on the excess contributions. Be sure to track your contributions carefully and stay within the annual limits.

- Failing to Keep Adequate Records: Failing to keep adequate records of your medical expenses can make it difficult to prove that your withdrawals were for qualified medical expenses if you are ever audited by the IRS. Keep detailed records of all your medical expenses, including receipts, invoices, and explanations of benefits (EOBs).

- Not Investing HSA Funds: Many HSA account holders miss out on the opportunity to grow their savings by not investing their HSA funds. Consider investing your HSA funds to take advantage of the tax-free growth potential.

19. How to Maximize Your HSA Savings?

Maximizing your HSA savings involves a combination of strategies, including contributing the maximum amount each year, investing your funds wisely, and using your HSA for qualified medical expenses. By implementing these strategies, you can build a substantial nest egg for future healthcare expenses.

- Contribute the Maximum Amount: If possible, contribute the maximum amount to your HSA each year. This will allow you to take full advantage of the tax benefits and build your savings more quickly.

- Invest Your Funds Wisely: Consider investing your HSA funds in a diversified portfolio of stocks, bonds, and mutual funds. This can help you grow your savings over time.

- Use Your HSA for Qualified Expenses: Use your HSA funds to pay for qualified medical expenses. This will allow you to avoid taxes and penalties and to stretch your healthcare dollars further.

- Let Your HSA Grow: If you don’t need to use your HSA funds for immediate medical expenses, let them grow over time. The longer your HSA funds have to grow, the more tax-free earnings you’ll accumulate.

20. Where Can I Find More Information About HSAs?

There are numerous resources available to help you learn more about HSAs. These include the IRS, HSA providers, and financial advisors. By consulting these resources, you can gain a deeper understanding of HSAs and make informed decisions about your healthcare savings.

- IRS: The IRS provides detailed information about HSAs in Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans. This publication covers topics such as eligibility, contributions, withdrawals, and tax implications.

- HSA Providers: HSA providers offer a wealth of information about HSAs on their websites. You can find information about HSA rules, contribution limits, investment options, and withdrawal procedures.

- Financial Advisors: A financial advisor can provide personalized advice about HSAs and help you develop a savings and investment strategy that aligns with your financial goals.

- money-central.com: Visit money-central.com for comprehensive guides, tools, and resources to help you understand and manage your HSA effectively.

An HSA can be a powerful tool for managing healthcare costs and saving for the future, as highlighted by money-central.com. While you can withdraw money from your HSA for personal use, it’s essential to understand the tax implications and potential penalties. By using your HSA wisely and following the IRS guidelines, you can maximize the benefits of this valuable savings account and achieve your financial goals.

Remember to explore money-central.com for more insights, tools, and expert advice to help you make the most of your HSA and other financial resources. Take control of your financial future today! Visit money-central.com at Address: 44 West Fourth Street, New York, NY 10012, United States. Phone: +1 (212) 998-0000.

FAQ: Health Savings Accounts (HSAs)

Here are 10 frequently asked questions about Health Savings Accounts (HSAs) to help you better understand how they work and how you can benefit from them.

1. What is a Health Savings Account (HSA)?

An HSA is a tax-advantaged savings account that can be used for healthcare expenses if you have a High Deductible Health Plan (HDHP). It offers a triple tax advantage: contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free.

2. Who is eligible for an HSA?

To be eligible for an HSA, you must have a High Deductible Health Plan (HDHP), not be covered by other non-HDHP health insurance, and not be claimed as a dependent on someone else’s tax return.

3. What are qualified medical expenses for HSA withdrawals?

Qualified medical expenses include a broad range of healthcare costs, such as doctor visits, prescriptions, dental and vision care, and certain over-the-counter items. Refer to IRS Publication 502 for a comprehensive list.

4. Can I use my HSA for non-medical expenses?

Yes, but there are consequences. Before age 65, withdrawals for non-qualified expenses are subject to income tax and a 20% penalty. After age 65, withdrawals for non-qualified expenses are subject to income tax, but the penalty no longer applies.

5. What happens to my HSA if I no longer have a High Deductible Health Plan (HDHP)?

If you no longer have an HDHP, you can no longer contribute to your HSA, but you can still use the funds in your account for qualified medical expenses.

6. Can I invest my HSA funds?

Yes, many HSAs allow you to invest your funds, providing an opportunity for tax-free growth. Investment options typically include mutual funds, stocks, and bonds.

7. What are the contribution limits for HSAs?

The IRS sets annual contribution limits for HSAs, which vary based on whether you have individual or family coverage. For 2023, the limits are $3,850 for individual coverage and $7,750 for family coverage, with an additional $1,000 catch-up contribution for those age 55 and older.

8. How do I withdraw money from my HSA?

Most HSAs provide a debit card or checks that you can use to pay for qualified medical expenses directly. You can also submit receipts for reimbursement.

9. Can I transfer or rollover funds from one HSA to another?

Yes, you can transfer or rollover funds from one HSA to another. A rollover involves taking a distribution from your existing HSA and then contributing it to a new HSA within 60 days. A transfer involves directly moving funds from your existing HSA to a new HSA without you ever taking possession of the money.

10. What happens to my HSA when I die?

What happens to your HSA when you die depends on who you designate as your beneficiary. If you designate your spouse as your beneficiary, your HSA will become their HSA. If you designate someone else as your beneficiary, the HSA will be distributed to them, and the funds will be subject to income tax.