Can I Withdraw Money From My Health Savings Account? Yes, you can withdraw money from your Health Savings Account (HSA) to cover qualified medical expenses tax-free, making it a powerful tool for managing healthcare costs and financial wellness, as explained by money-central.com. Understanding the rules and regulations surrounding HSA withdrawals is key to maximizing the benefits of this account and avoiding potential penalties, especially when planning your personal finances and budgeting.

1. What Is a Health Savings Account (HSA) and How Does It Work?

A Health Savings Account (HSA) is a tax-advantaged savings account that can be used for healthcare expenses. It is available to taxpayers in the United States who have a high-deductible health insurance plan (HDHP). These accounts are designed to help individuals save for medical expenses while enjoying tax benefits. The money you contribute to an HSA is tax-deductible, the funds grow tax-free, and withdrawals for qualified medical expenses are also tax-free.

1.1. Key Features of Health Savings Accounts

Here are the key features of a Health Savings Account:

- Tax Advantages: Contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are tax-free.

- Eligibility: Must be enrolled in a High Deductible Health Plan (HDHP).

- Contribution Limits: Annual limits set by the IRS (e.g., $3,850 for individuals and $7,750 for families in 2023, plus an additional $1,000 for those age 55 and older).

- Portability: The account is yours, even if you change jobs or health plans.

- Investment Options: Many HSAs offer investment options, allowing you to grow your savings over time.

- Triple Tax Advantage: Contributions, growth, and qualified withdrawals are all tax-free.

- Rollover: Unused funds roll over year after year, allowing you to save for future healthcare expenses.

- Accessibility: Funds can be used to pay for a wide range of qualified medical expenses.

- Retirement Savings Tool: Can be used as a retirement savings vehicle, as funds can be withdrawn for any reason after age 65 (though non-medical withdrawals are subject to income tax).

- Flexibility: Offers flexibility in managing healthcare expenses and saving for the future.

1.2. Who Is Eligible for a Health Savings Account?

To be eligible for a Health Savings Account (HSA), you must meet the following criteria:

- High Deductible Health Plan (HDHP): You must be covered by a qualifying HDHP. For 2023, this means a plan with a deductible of at least $1,500 for individuals and $3,000 for families.

- No Other Health Coverage: You cannot be covered by any other health plan that is not an HDHP, with some exceptions like dental, vision, and long-term care insurance.

- Not Enrolled in Medicare: You cannot be enrolled in Medicare.

- Not a Dependent: You cannot be claimed as a dependent on someone else’s tax return.

1.3. Contribution Limits for Health Savings Accounts

The IRS sets annual contribution limits for Health Savings Accounts. These limits may change each year, so it’s important to stay updated.

| Year | Individual | Family | Catch-Up Contribution (Age 55+) |

|---|---|---|---|

| 2023 | $3,850 | $7,750 | $1,000 |

| 2024 | $4,150 | $8,300 | $1,000 |

These limits include contributions made by both you and your employer. If you are age 55 or older, you are eligible to make an additional “catch-up” contribution.

1.4. Benefits of Using a Health Savings Account

Using a Health Savings Account comes with several key benefits:

- Tax Savings: Enjoy tax deductions on contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

- Healthcare Cost Control: Helps you manage and plan for healthcare expenses.

- Investment Opportunities: Allows you to invest your HSA funds, potentially growing your savings over time.

- Retirement Savings: Can be used as a retirement savings vehicle, providing flexibility and tax advantages.

- Portability: The account is yours, even if you change jobs or health plans.

- Flexibility: Offers flexibility in managing healthcare expenses and saving for the future.

- Long-Term Savings: Encourages long-term savings for healthcare needs.

- Financial Security: Provides a financial cushion for unexpected medical expenses.

- Estate Planning: Can be passed on to beneficiaries, providing potential estate planning benefits.

- Peace of Mind: Offers peace of mind knowing you have a dedicated savings account for healthcare.

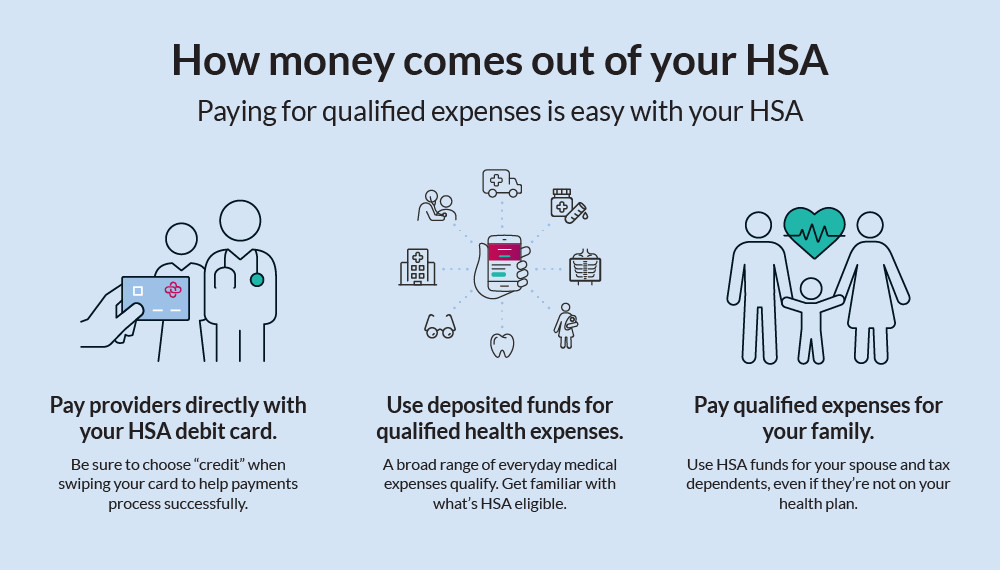

HSA infographic how money comes out of HSA

HSA infographic how money comes out of HSA

2. Understanding the Rules for Withdrawing Money From Your HSA

Understanding the rules for withdrawing money from your Health Savings Account (HSA) is crucial for maximizing its benefits and avoiding penalties. The primary rule is that withdrawals must be used for qualified medical expenses to remain tax-free. If you use the funds for non-qualified expenses, you may be subject to income tax and a penalty, depending on your age.

2.1. Qualified Medical Expenses

Qualified medical expenses are the costs of diagnosis, cure, mitigation, treatment, or prevention of disease, and the costs for treatments affecting any part or function of the body. These expenses include, but are not limited to:

- Doctor Visits: Fees for visits to physicians, specialists, and other healthcare providers.

- Prescriptions: Costs of prescription medications.

- Dental Care: Dental exams, cleanings, fillings, and other dental treatments.

- Vision Care: Eye exams, eyeglasses, and contact lenses.

- Hospital Services: Inpatient and outpatient hospital care.

- Medical Equipment: Costs of medical equipment such as wheelchairs, crutches, and walkers.

- Mental Health Services: Therapy, counseling, and psychiatric care.

- Substance Abuse Treatment: Costs associated with substance abuse treatment programs.

- Long-Term Care: Expenses for long-term care services.

2.2. Non-Qualified Medical Expenses

Non-qualified medical expenses are those that do not meet the IRS definition of qualified medical expenses. If you withdraw money from your HSA for these expenses, the withdrawal will be subject to income tax, and if you are under age 65, it will also be subject to a 20% penalty. Common examples of non-qualified expenses include:

- Cosmetic Surgery: Unless it is medically necessary.

- Health Insurance Premiums: Except for COBRA, Medicare, and long-term care insurance.

- Non-Prescription Medications: Unless a doctor prescribes them.

- Personal Use Items: Such as toiletries or other personal care items.

- Funeral Expenses: These are not considered medical expenses.

2.3. Age Considerations for HSA Withdrawals

Your age plays a significant role in how HSA withdrawals are taxed and penalized. Here’s a breakdown:

- Under Age 65: Withdrawals for non-qualified medical expenses are subject to income tax and a 20% penalty.

- Age 65 and Older: Withdrawals for non-qualified medical expenses are subject to income tax but are no longer subject to the 20% penalty. In this case, the HSA functions similarly to a traditional IRA.

- Any Age: Withdrawals for qualified medical expenses are always tax-free.

2.4. Documentation and Record-Keeping for Withdrawals

It is crucial to maintain thorough records of all HSA withdrawals and the corresponding medical expenses. This includes:

- Receipts: Keep detailed receipts for all medical expenses.

- Explanation of Benefits (EOB): Obtain EOBs from your insurance company to verify the medical services and costs.

- Withdrawal Records: Maintain records of all HSA withdrawals, including the date, amount, and purpose of the withdrawal.

- Tax Forms: Keep copies of relevant tax forms, such as Form 8889 (Health Savings Accounts (HSAs)).

2.5. Strategies to Maximize HSA Benefits

To make the most of your HSA, consider these strategies:

- Pay Out-of-Pocket: If possible, pay for medical expenses out-of-pocket and let your HSA grow tax-free.

- Invest HSA Funds: If your HSA offers investment options, consider investing a portion of your funds to potentially grow your savings over time.

- Use for Retirement Healthcare: Treat your HSA as a retirement healthcare fund, allowing it to grow and be available for future medical expenses.

- Stay Informed: Keep up-to-date with HSA rules and regulations to ensure you are making informed decisions.

- Consult a Professional: Seek advice from a financial advisor or tax professional to optimize your HSA strategy.

3. Step-by-Step Guide on How to Withdraw Funds From Your HSA

Withdrawing funds from your Health Savings Account (HSA) is a straightforward process, but it’s important to follow the correct steps to ensure you maintain the tax benefits and avoid any potential penalties. Here’s a step-by-step guide on how to withdraw funds from your HSA:

3.1. Determine if the Expense Is Qualified

Before making a withdrawal, verify that the expense is a qualified medical expense as defined by the IRS. Refer to the list of qualified medical expenses to ensure your withdrawal will be tax-free.

3.2. Choose a Withdrawal Method

HSAs typically offer several methods for withdrawing funds, including:

- HSA Debit Card: Many HSAs provide a debit card that can be used to pay for qualified medical expenses directly at the point of service.

- Online Bill Pay: Some HSAs allow you to pay medical bills directly through an online bill pay system.

- Reimbursement: You can pay for the expense out-of-pocket and then reimburse yourself from your HSA.

- Check: Some HSAs offer the option to write checks from your HSA account.

3.3. Initiate the Withdrawal

Follow the specific instructions for your chosen withdrawal method:

- HSA Debit Card: Use the debit card to pay for the expense at the time of service.

- Online Bill Pay: Log in to your HSA account online and use the bill pay feature to pay the medical provider directly.

- Reimbursement: Submit a claim for reimbursement through your HSA administrator’s website or by mail. Include documentation such as receipts and Explanation of Benefits (EOB) statements.

- Check: Write a check from your HSA account and send it to the medical provider or use it to reimburse yourself.

3.4. Provide Necessary Documentation

When submitting a claim for reimbursement, be sure to include all required documentation, such as:

- Receipts: Detailed receipts from the medical provider.

- Explanation of Benefits (EOB): Statements from your insurance company.

- Claim Form: If required by your HSA administrator.

3.5. Track Your Withdrawals

Keep a record of all HSA withdrawals, including the date, amount, and purpose of the withdrawal. This will help you track your spending and ensure you have accurate records for tax purposes.

3.6. File Form 8889 With Your Taxes

When you file your taxes, you will need to complete Form 8889 (Health Savings Accounts (HSAs)) to report your HSA contributions, distributions, and any other relevant information.

3.7. What to Do If You Make a Mistaken Withdrawal

If you accidentally withdraw funds for a non-qualified expense, there are a few steps you can take:

- Return the Funds: If you realize the mistake quickly, you may be able to return the funds to your HSA. Contact your HSA administrator to see if this is possible.

- Report the Withdrawal: Report the withdrawal as taxable income on your tax return and pay any applicable penalties.

- Consult a Tax Advisor: Seek advice from a tax advisor to understand the tax implications of the withdrawal and how to correct any errors.

4. HSA Withdrawal Scenarios: Common Situations and How to Handle Them

Health Savings Accounts (HSAs) offer flexibility in managing healthcare expenses, but knowing how to handle different withdrawal scenarios is essential. Here are some common situations and guidance on how to manage them effectively:

4.1. Paying for Routine Medical Expenses

Scenario: You have routine medical expenses such as doctor visits, prescription refills, and dental cleanings.

How to Handle:

- Use your HSA debit card to pay for these expenses directly at the point of service.

- Alternatively, pay out-of-pocket and reimburse yourself later by submitting a claim with receipts.

- Ensure that all expenses are qualified medical expenses to avoid taxes and penalties.

4.2. Covering Unexpected Medical Bills

Scenario: You receive an unexpected medical bill due to an accident, illness, or emergency.

How to Handle:

- Use your HSA funds to pay the medical bill.

- If you don’t have enough funds in your HSA, consider using a payment plan offered by the medical provider.

- Submit a claim for reimbursement with receipts and Explanation of Benefits (EOB) statements.

4.3. Paying for Over-the-Counter Medications

Scenario: You need to purchase over-the-counter (OTC) medications.

How to Handle:

- OTC medications are generally not considered qualified medical expenses unless prescribed by a doctor.

- If a doctor prescribes the medication, obtain a written prescription and keep it for your records.

- Use your HSA funds to pay for the prescribed OTC medication and submit a claim for reimbursement.

4.4. Using HSA Funds While Unemployed

Scenario: You are unemployed and need to use your HSA funds for medical expenses.

How to Handle:

- You can continue to use your HSA funds for qualified medical expenses even if you are unemployed.

- If you are no longer eligible to contribute to your HSA due to not having a qualifying High Deductible Health Plan (HDHP), you can still withdraw funds for qualified medical expenses.

- Consider using your HSA funds to pay for COBRA premiums to maintain health insurance coverage.

4.5. Paying for Expenses of Dependents

Scenario: You want to use your HSA funds to pay for the medical expenses of your spouse or dependents.

How to Handle:

- You can use your HSA funds to pay for the qualified medical expenses of your spouse and dependents, even if they are not covered by your HDHP.

- Keep records of the expenses and ensure they are qualified medical expenses.

4.6. Transferring HSA Funds

Scenario: You want to transfer your HSA funds to a different HSA provider.

How to Handle:

- You can transfer your HSA funds to a different provider through a direct transfer or a rollover.

- A direct transfer involves your current HSA provider sending the funds directly to your new HSA provider.

- A rollover involves you receiving the funds and then depositing them into your new HSA within 60 days.

- Direct transfers are generally preferred as they do not count towards the one-rollover-per-year limit.

4.7. Using HSA Funds in Retirement

Scenario: You are retired and want to use your HSA funds for medical expenses.

How to Handle:

- You can continue to use your HSA funds for qualified medical expenses in retirement.

- After age 65, you can withdraw funds for non-qualified expenses without penalty, but the withdrawals will be subject to income tax.

- Consider using your HSA funds to pay for Medicare premiums, long-term care insurance, and other healthcare expenses in retirement.

5. Common Mistakes to Avoid When Withdrawing From Your HSA

Withdrawing from your Health Savings Account (HSA) requires careful attention to detail to avoid costly mistakes. Here are some common pitfalls to watch out for:

5.1. Withdrawing for Non-Qualified Expenses

Mistake: Withdrawing funds for expenses that do not qualify as medical expenses under IRS guidelines.

How to Avoid:

- Always verify that the expense is a qualified medical expense before making a withdrawal.

- Refer to IRS Publication 502 for a comprehensive list of qualified medical expenses.

- When in doubt, consult with your HSA administrator or a tax professional.

5.2. Failing to Keep Adequate Records

Mistake: Not maintaining detailed records of HSA withdrawals and the corresponding medical expenses.

How to Avoid:

- Keep all receipts, Explanation of Benefits (EOB) statements, and other documentation related to your medical expenses.

- Use a spreadsheet or software to track your HSA withdrawals and expenses.

- Store your records in a safe and organized manner for easy access.

5.3. Missing the 60-Day Rollover Deadline

Mistake: Failing to deposit rolled-over funds into a new HSA within 60 days.

How to Avoid:

- If you choose to roll over your HSA funds, make sure to deposit the funds into a new HSA within 60 days of receiving them.

- Set a reminder to ensure you don’t miss the deadline.

- Consider a direct transfer instead of a rollover to avoid the 60-day deadline altogether.

5.4. Withdrawing Funds After Enrolling in Medicare

Mistake: Contributing to an HSA after enrolling in Medicare.

How to Avoid:

- Stop contributing to your HSA once you enroll in Medicare.

- You can continue to withdraw funds from your HSA for qualified medical expenses, but you cannot make new contributions.

5.5. Paying Taxes and Penalties Unnecessarily

Mistake: Paying taxes and penalties on HSA withdrawals that could have been avoided.

How to Avoid:

- Only withdraw funds for qualified medical expenses to avoid taxes and penalties.

- Keep accurate records of your withdrawals and expenses to substantiate your claims.

- If you make a mistake, correct it as soon as possible by returning the funds to your HSA or reporting the withdrawal as taxable income.

5.6. Not Understanding HSA Rules

Mistake: Making decisions about your HSA without fully understanding the rules and regulations.

How to Avoid:

- Take the time to learn about HSA rules and regulations.

- Read IRS publications and consult with your HSA administrator or a tax professional.

- Stay informed about changes to HSA rules and regulations.

5.7. Using HSA Funds for Non-Medical Expenses Before Age 65

Mistake: Withdrawing funds for non-medical expenses before age 65, incurring taxes and penalties.

How to Avoid:

- Avoid using HSA funds for non-medical expenses before age 65 unless absolutely necessary.

- If you must use the funds for non-medical expenses, be prepared to pay income tax and a 20% penalty.

5.8. Forgetting About State Taxes

Mistake: Ignoring state tax implications of HSA contributions and withdrawals.

How to Avoid:

- Research the state tax laws in your state to understand how HSAs are treated.

- Some states may not offer the same tax benefits as the federal government.

5.9. Not Reviewing HSA Investment Options

Mistake: Failing to review and optimize your HSA investment options.

How to Avoid:

- If your HSA offers investment options, take the time to review them and choose investments that align with your risk tolerance and financial goals.

- Rebalance your portfolio periodically to maintain your desired asset allocation.

5.10. Withdrawing Too Much Too Soon

Mistake: Depleting your HSA funds too quickly, leaving you unprepared for future medical expenses.

How to Avoid:

- Avoid withdrawing more funds than you need for current medical expenses.

- Let your HSA funds grow over time to cover future healthcare costs.

- Consider paying for some medical expenses out-of-pocket to preserve your HSA funds.

6. Tax Implications of HSA Withdrawals

Understanding the tax implications of Health Savings Account (HSA) withdrawals is essential for maximizing the benefits of your account and avoiding potential penalties. Here’s a detailed overview of how HSA withdrawals are taxed:

6.1. Qualified Medical Expenses

Tax Treatment: Withdrawals for qualified medical expenses are tax-free at the federal level. This means you won’t pay income tax on the withdrawn amount, and it won’t be subject to any penalties.

Requirements: To qualify for tax-free treatment, the expenses must meet the IRS definition of qualified medical expenses. This includes costs for diagnosis, cure, mitigation, treatment, or prevention of disease, and the costs for treatments affecting any part or function of the body.

Examples: Doctor visits, prescription medications, dental care, vision care, hospital services, and medical equipment.

6.2. Non-Qualified Medical Expenses (Under Age 65)

Tax Treatment: Withdrawals for non-qualified medical expenses before age 65 are subject to income tax and a 20% penalty at the federal level.

Implications: The withdrawn amount will be added to your taxable income for the year, and you will owe income tax based on your tax bracket. Additionally, you will owe a penalty of 20% of the withdrawn amount.

Examples: Cosmetic surgery (unless medically necessary), health insurance premiums (except for COBRA, Medicare, and long-term care insurance), and non-prescription medications (unless prescribed by a doctor).

6.3. Non-Qualified Medical Expenses (Age 65 and Older)

Tax Treatment: Withdrawals for non-qualified medical expenses at age 65 and older are subject to income tax but are not subject to the 20% penalty.

Implications: The withdrawn amount will be added to your taxable income for the year, and you will owe income tax based on your tax bracket. However, the 20% penalty is waived.

Functionality: At age 65, the HSA functions similarly to a traditional IRA, where withdrawals are taxed as income but are not penalized.

6.4. State Tax Implications

Tax Treatment: State tax treatment of HSA contributions and withdrawals can vary. Some states follow the federal tax rules, while others have their own rules.

Considerations: Research the state tax laws in your state to understand how HSAs are treated. Some states may not offer the same tax benefits as the federal government.

Examples: Some states may tax HSA contributions or withdrawals, while others may not.

6.5. Reporting HSA Withdrawals on Your Tax Return

Form 8889: You will need to complete Form 8889 (Health Savings Accounts (HSAs)) when you file your taxes to report your HSA contributions, distributions, and any other relevant information.

Instructions: Follow the instructions on Form 8889 to accurately report your HSA activity.

Record-Keeping: Keep detailed records of all HSA withdrawals and the corresponding medical expenses to support your tax return.

6.6. Tax Advantages of HSAs

Triple Tax Advantage: HSAs offer a triple tax advantage:

- Contributions are tax-deductible.

- Earnings grow tax-free.

- Qualified withdrawals are tax-free.

Long-Term Savings: This triple tax advantage makes HSAs an attractive vehicle for long-term healthcare savings.

6.7. Avoiding Tax Penalties

Qualified Expenses: To avoid tax penalties, only withdraw funds for qualified medical expenses.

Record-Keeping: Keep accurate records of your withdrawals and expenses.

Consult a Professional: Consult with a tax professional or financial advisor for personalized advice on managing your HSA and minimizing your tax liability.

7. Alternatives to Withdrawing Money From Your HSA

While withdrawing money from your Health Savings Account (HSA) is a common way to cover medical expenses, there are alternative strategies you can use to preserve your HSA funds and maximize their long-term benefits. Here are some alternatives to consider:

7.1. Paying Out-of-Pocket and Reimbursing Later

Strategy: Pay for medical expenses out-of-pocket and reimburse yourself from your HSA at a later date.

Benefits:

- Allows your HSA funds to continue growing tax-free.

- Provides flexibility in managing your cash flow.

- Enables you to save your HSA funds for future healthcare needs.

Considerations:

- Requires you to have sufficient funds available to pay for medical expenses out-of-pocket.

- You must keep detailed records of your expenses and reimbursements.

7.2. Using a Health Savings Credit Card

Strategy: Use a health savings credit card to pay for medical expenses.

Benefits:

- Provides a convenient way to pay for medical expenses.

- Allows you to track your medical expenses separately from other expenses.

- Offers rewards or cashback on medical purchases.

Considerations:

- Requires you to have a good credit score to qualify for a health savings credit card.

- You must pay off the credit card balance in full each month to avoid interest charges.

7.3. Investing HSA Funds

Strategy: Invest your HSA funds in stocks, bonds, or mutual funds.

Benefits:

- Allows your HSA funds to grow over time.

- Provides the potential for higher returns compared to traditional savings accounts.

- Enables you to save for future healthcare needs.

Considerations:

- Involves investment risk, and you could lose money.

- Requires you to have a long-term investment horizon.

7.4. Utilizing Employer Wellness Programs

Strategy: Participate in employer wellness programs to reduce your healthcare costs.

Benefits:

- May provide incentives for participating in wellness activities.

- Can help you improve your health and reduce your risk of medical expenses.

- May offer discounts on health insurance premiums.

Considerations:

- Requires you to actively participate in wellness programs.

- May not be available at all employers.

7.5. Negotiating Medical Bills

Strategy: Negotiate medical bills with healthcare providers to reduce your costs.

Benefits:

- Can help you save money on medical expenses.

- May result in a lower overall cost of care.

Considerations:

- Requires you to be proactive in negotiating your bills.

- May not always be successful.

7.6. Seeking Generic Medications

Strategy: Ask your doctor for generic alternatives to brand-name medications.

Benefits:

- Can help you save money on prescription drugs.

- Generic medications are typically less expensive than brand-name medications.

Considerations:

- Requires you to talk to your doctor about generic alternatives.

- May not be suitable for all medications.

7.7. Using Telehealth Services

Strategy: Utilize telehealth services for medical consultations and treatment.

Benefits:

- Provides convenient access to healthcare services.

- Can save you time and money compared to traditional in-office visits.

Considerations:

- May not be suitable for all medical conditions.

- Requires you to have access to technology and a reliable internet connection.

7.8. Preventive Care

Strategy: Investing in preventive care to avoid costly medical expenses in the future.

Benefits:

- Can help you stay healthy and avoid medical expenses.

- Preventive care services are often covered by insurance.

Considerations:

- Requires you to be proactive in taking care of your health.

- May involve lifestyle changes and regular check-ups.

7.9. Comparing Prices

Strategy: Comparison shopping between doctors.

Benefits:

- Can help you save money on medical expenses.

- You may be able to use online tools to compare the cost of doctor visits in your area.

Considerations:

- Requires you to actively compare the costs of different doctors in your area.

By considering these alternatives, you can make informed decisions about how to manage your healthcare expenses and maximize the benefits of your HSA.

8. The Future of Health Savings Accounts

Health Savings Accounts (HSAs) have become an increasingly popular tool for managing healthcare expenses, and their future looks promising as they continue to evolve and adapt to the changing healthcare landscape. Here’s a look at the potential future trends and developments for HSAs:

8.1. Increased Adoption

Trend: HSAs are expected to continue growing in popularity as more people recognize their benefits.

Factors Driving Growth:

- Rising healthcare costs.

- Increased awareness of the tax advantages of HSAs.

- Expansion of HSA-compatible health plans.

Implications:

- Greater availability of HSA products and services.

- Increased competition among HSA providers.

8.2. Expansion of Investment Options

Trend: HSA providers are likely to expand their investment options to attract more savers.

Potential Developments:

- More diverse investment choices, including ETFs, mutual funds, and individual stocks.

- Robo-advisors to help HSA holders manage their investments.

- Integration of financial planning tools to help HSA holders plan for retirement healthcare expenses.

Implications:

- Greater potential for HSA funds to grow over time.

- Increased complexity in managing HSA investments.

8.3. Integration With Wellness Programs

Trend: HSAs may become more closely integrated with employer wellness programs.

Potential Developments:

- Employers may offer incentives for participating in wellness programs, such as contributions to HSAs.

- HSAs may be used to pay for wellness-related expenses, such as gym memberships or nutrition counseling.

Implications:

- Greater emphasis on preventive care.

- Improved health outcomes for HSA holders.

8.4. Legislative Changes

Trend: Legislative changes could impact the rules and regulations governing HSAs.

Potential Changes:

- Changes to contribution limits.

- Modifications to the definition of qualified medical expenses.

- New rules regarding HSA eligibility.

Implications:

- HSA holders need to stay informed about legislative changes.

- Legislative changes could impact the attractiveness of HSAs.

8.5. Increased Use in Retirement Planning

Trend: HSAs are likely to be increasingly used as a tool for retirement healthcare planning.

Potential Developments:

- Financial advisors may recommend HSAs as part of a comprehensive retirement plan.

- HSA providers may offer tools and resources to help HSA holders plan for retirement healthcare expenses.

Implications:

- Greater awareness of the long-term benefits of HSAs.

- Increased use of HSAs to pay for healthcare expenses in retirement.

8.6. Technological Advancements

Trend: Technological advancements could make it easier to manage and use HSAs.

Potential Developments:

- Mobile apps for managing HSA accounts.

- Integration of HSA accounts with electronic health records.

- Artificial intelligence (AI) to help HSA holders make informed decisions about their healthcare spending.

Implications:

- Greater convenience and ease of use.

- Improved decision-making regarding healthcare expenses.

8.7. Focus on Financial Literacy

Trend: There may be a greater focus on financial literacy related to HSAs.

Potential Developments:

- Educational resources to help people understand the benefits of HSAs.

- Financial literacy programs to help people make informed decisions about their healthcare spending.

Implications:

- Greater awareness of the benefits of HSAs.

- Improved financial outcomes for HSA holders.

8.8. HSAs and Healthcare Reform

Trend: The future of HSAs may be influenced by broader healthcare reform efforts.

Potential Impacts:

- Changes to the Affordable Care Act (ACA).

- Implementation of new healthcare policies.

Implications:

- HSA holders need to stay informed about healthcare reform efforts.

- Healthcare reform could impact the attractiveness of HSAs.

By staying informed about these trends and developments, you can make informed decisions about how to use your HSA and prepare for the future of healthcare.

9. Finding the Right HSA Provider

Choosing the right Health Savings Account (HSA) provider is a crucial step in maximizing the benefits of your account. With numerous providers available, each offering different features and services, it’s important to consider your individual needs and preferences. Here’s a guide to help you find the right HSA provider:

9.1. Evaluate Fees

Consideration: Look for providers with low or no fees.

Types of Fees:

- Maintenance Fees: Monthly or annual fees for maintaining the account.

- Transaction Fees: Fees for withdrawals, transfers, or other transactions.

- Investment Fees: Fees for investing your HSA funds.

Recommendation: Compare the fee structures of different providers and choose one with minimal fees.

9.2. Assess Investment Options

Consideration: If you plan to invest your HSA funds, evaluate the investment options offered by the provider.

Factors to Consider:

- Investment Choices: Availability of a variety of investment options, such as stocks, bonds, and mutual funds.

- Expense Ratios: The expense ratios of the investment options.

- Investment Performance: The historical performance of the investment options.

Recommendation: Choose a provider with a range of low-cost investment options that align with your risk tolerance and financial goals.

9.3. Check Interest Rates

Consideration: If you plan to keep a portion of your HSA funds in cash, check the interest rates offered by the provider.

Factors to Consider:

- Interest Rate: The interest rate paid on cash balances.

- Compounding Frequency: How often the interest is compounded.

Recommendation: Choose a provider that offers a competitive interest rate on cash balances.

9.4. Review Customer Service

Consideration: Evaluate the customer service provided by the HSA provider.

Factors to Consider:

- Availability: The availability of customer service representatives by phone, email, or chat.

- Responsiveness: The responsiveness of customer service representatives to your inquiries.

- Knowledge: The knowledge and expertise of customer service representatives.

Recommendation: Read reviews and testimonials from other HSA holders to assess the quality of customer service provided by the provider.

9.5. Evaluate Online Tools and Resources

Consideration: Assess the online tools and resources offered by the HSA provider.

Factors to Consider:

- Website Usability: The ease of use and navigation of the provider’s website.

- Mobile App: The availability of a mobile app for managing your HSA account.

- Educational Resources: The availability of educational articles, videos, and tools to help you learn about HSAs.

Recommendation: Choose a provider with user-friendly online tools and resources that make it easy to manage your HSA account.

9.6. Check Account Minimums

Consideration: Determine if the HSA provider has any account minimums.

Factors to Consider:

- Minimum Balance Requirements: The minimum balance required to open and maintain an HSA account.

- Minimum Contribution Requirements: The minimum contribution required to open and maintain an HSA account.

Recommendation: Choose a provider with no or low account minimums.