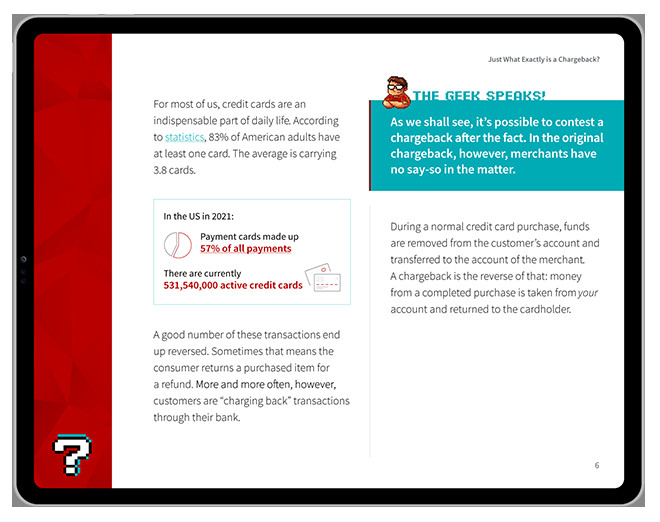

Can You Get Your Money Back On Zelle? Understanding Zelle’s policies and your options is crucial for protecting your finances, and that’s where money-central.com comes in. Zelle is a convenient way to send money, but knowing how to navigate potential issues like scams and unauthorized transactions can save you a lot of financial stress. We’ll explore Zelle’s refund policies, security measures, and alternative payment methods, plus practical tips to help you secure your digital funds and make informed decisions.

1. What Is Zelle and How Does It Work?

Zelle is a digital payment network that allows users to send and receive money directly between bank accounts in the U.S. Zelle is integrated into many banking apps, making it easy to use for people who already manage their finances online. The service facilitates near-instant transfers, offering a convenient way to split bills, send gifts, or pay for services.

How Zelle Works

- Direct Transfers: Money moves directly from one bank account to another without an intermediary holding the funds.

- Integration: Zelle is often built into existing banking apps, simplifying the process for users.

- Speed: Transfers are typically completed within minutes, making it a fast option for payments.

While Zelle offers convenience, it’s important to use it with care, particularly when sending money to individuals or businesses you don’t know well. Understanding the security aspects and user policies of Zelle is crucial to protecting your funds.

2. Understanding Zelle’s Policy on Refunds and Reimbursements

Can you get your money back on Zelle? Zelle’s policies regarding refunds and reimbursements are quite specific. Generally, Zelle transactions are designed to be similar to cash transactions, meaning that once a payment is sent, it’s difficult to reverse. Here’s what you need to know:

Authorized vs. Unauthorized Transactions

- Authorized Transactions: If you willingly send money to someone, even if it turns out to be a scam, getting a refund can be difficult. Zelle’s user agreement states that authorized payments are final and irreversible.

- Unauthorized Transactions: If someone gains access to your account and sends money without your permission, this is considered an unauthorized transaction. In such cases, you may have a better chance of recovering your funds.

Regulation E and Zelle Protection

Regulation E, under the Electronic Fund Transfer Act, provides some protection for consumers in cases of unauthorized electronic fund transfers. If you report an unauthorized Zelle transaction promptly, your bank may be required to investigate and potentially reimburse you.

Zelle’s Stance on Scams

Zelle advises users to only send money to people they know and trust. The platform doesn’t offer purchase protection like some other payment services, so if you get scammed, recovering your money can be challenging.

For more detailed guidance on managing your finances and understanding payment options, visit money-central.com.

3. When Can You Get Your Money Back on Zelle?

Can you get your money back on Zelle? There are specific scenarios where you might be able to recover your funds. Understanding these situations can help you act quickly and increase your chances of a successful recovery.

Unauthorized Transactions

If someone accesses your Zelle account without your permission and sends money, it’s considered an unauthorized transaction. In these cases, you should:

- Report Immediately: Contact your bank as soon as you notice the unauthorized activity.

- File a Police Report: This can provide additional documentation for your bank’s investigation.

- Cooperate with the Investigation: Provide all necessary information to your bank to help them investigate the issue thoroughly.

Technical Errors

Sometimes, technical glitches can cause incorrect transactions. If you experience a technical error, such as a double charge or an incorrect amount being sent, contact your bank immediately. They can investigate the issue and potentially reverse the transaction.

Recipient Not Enrolled

If you send money to someone who isn’t enrolled in Zelle, you can cancel the transaction. The recipient needs to enroll in Zelle to claim the money, so if they haven’t done so, you can cancel the payment through your banking app.

Bank Intervention

In some cases, if you’ve been scammed, your bank might be willing to help recover the funds, even if Zelle’s official policy doesn’t guarantee a refund. This often depends on the bank’s policies and the specific circumstances of the scam.

Keep in mind that the sooner you act, the better your chances of recovering your money. For more advice on managing your finances and dealing with fraud, explore resources at money-central.com.

4. Step-by-Step Guide to Reporting a Zelle Scam or Unauthorized Transaction

Can you get your money back on Zelle? If you suspect you’ve been scammed or have noticed an unauthorized transaction, taking immediate action is critical. Here’s a step-by-step guide to help you report the issue and potentially recover your funds.

Step 1: Contact Your Bank Immediately

The first and most crucial step is to contact your bank as soon as you notice the fraudulent activity. Most banks have a dedicated fraud department that can assist you.

- Phone Call: Call the bank’s customer service or fraud hotline.

- Online Reporting: Check if your bank allows you to report fraud online through their website or app.

Step 2: Gather Information

Before you report, gather all relevant information about the transaction. This includes:

- Date and Time: When the transaction occurred.

- Amount: The exact amount of money involved.

- Recipient Information: Name, email address, or phone number of the recipient.

- Transaction Details: Any reference numbers or transaction IDs.

- Description of the Incident: A clear and concise explanation of what happened.

Step 3: File a Formal Complaint

Most banks require you to file a formal complaint in writing. This could be through a form on their website, a letter, or an email. Make sure to include all the information you gathered in Step 2.

Step 4: File a Police Report

Filing a police report can provide additional documentation for your case and may be required by your bank. Contact your local police department and provide them with all the details of the scam or unauthorized transaction.

Step 5: Cooperate with the Investigation

Your bank will conduct an investigation into the matter. Be prepared to provide any additional information or documentation they may need. This could include:

- Affidavits: Sworn statements about the incident.

- Additional Transaction History: To help identify any other suspicious activity.

Step 6: Monitor Your Account

Keep a close eye on your account for any further unauthorized activity. Change your passwords and PINs, and consider setting up transaction alerts to notify you of any unusual activity.

Step 7: Follow Up

Stay in contact with your bank to check on the status of the investigation. Ask for updates and ensure they are taking the necessary steps to resolve the issue.

For additional resources on protecting yourself from fraud and managing your finances, visit money-central.com.

Reporting Unauthorized Transactions

Reporting Unauthorized Transactions

5. Common Zelle Scams and How to Avoid Them

Can you get your money back on Zelle? Knowing how to spot common scams can significantly reduce your risk of falling victim. Here are some of the most prevalent Zelle scams and practical tips to avoid them.

1. Impersonation Scams

- How it Works: Scammers impersonate bank representatives, government officials, or customer support agents to trick you into sending money or providing personal information.

- How to Avoid: Always verify the identity of the person contacting you. Call the official number of the bank or organization directly. Never provide personal information or send money to someone who contacts you unexpectedly.

2. Purchase Scams

- How it Works: Scammers sell items online (e.g., on Craigslist or Facebook Marketplace) and ask for payment via Zelle. Once you send the money, they disappear without delivering the item.

- How to Avoid: Only use Zelle with people you know and trust. For online purchases, use payment methods that offer buyer protection, such as credit cards or PayPal.

3. Emergency Scams

- How it Works: Scammers pose as a family member or friend in urgent need of money. They claim to be in a crisis and pressure you to send money immediately via Zelle.

- How to Avoid: Verify the person’s identity by contacting them through a known phone number or social media account. Be wary of urgent requests and never send money without confirming the situation.

4. Business Email Compromise (BEC) Scams

- How it Works: Scammers hack into a business email account and send fake invoices or payment requests to customers or employees. They instruct recipients to send payments via Zelle to a fraudulent account.

- How to Avoid: Always double-check payment requests with the business through a known phone number or in person. Be suspicious of any sudden changes in payment instructions.

5. Refund Scams

- How it Works: Scammers claim they accidentally sent you money via Zelle and ask you to refund it. However, the original transaction was fraudulent, and you’ll be sending your own money to the scammer.

- How to Avoid: Verify any unexpected transactions with your bank. If someone claims to have accidentally sent you money, do not refund it. Contact your bank to report the incident.

General Tips to Avoid Zelle Scams

- Only Send Money to People You Know: Zelle is designed for sending money to friends, family, and people you trust.

- Verify Requests: Always verify any requests for money, especially if they come unexpectedly.

- Be Wary of Urgency: Scammers often create a sense of urgency to pressure you into acting quickly.

- Protect Your Information: Never share your Zelle login credentials or banking information with anyone.

- Monitor Your Account: Regularly check your account for any suspicious activity.

For more tips on managing your finances and staying safe from scams, visit money-central.com.

6. Alternative Payment Methods That Offer More Protection

Can you get your money back on Zelle? Zelle is convenient, but it doesn’t offer the same level of protection as some other payment methods. If you’re concerned about security, consider using these alternatives.

1. Credit Cards

Credit cards offer strong consumer protections, including:

- Fraud Protection: If your credit card is used for unauthorized purchases, you can dispute the charges and potentially get your money back.

- Purchase Protection: Some credit cards offer purchase protection, which covers you if an item you bought is damaged, stolen, or never delivered.

- Dispute Rights: You have the right to dispute charges for goods or services that weren’t provided as agreed.

2. PayPal

PayPal offers buyer and seller protection programs:

- Buyer Protection: If an item you purchased through PayPal isn’t delivered or doesn’t match the seller’s description, you can file a dispute and potentially get a refund.

- Seller Protection: Sellers are protected against chargebacks and fraud claims.

3. Venmo

Venmo, like PayPal, offers some protections, although they are more limited than credit cards:

- Dispute Resolution: Venmo provides a process for resolving disputes between buyers and sellers.

- Fraud Monitoring: Venmo monitors transactions for suspicious activity and may freeze accounts to prevent fraud.

4. Apple Pay and Google Pay

These mobile payment platforms offer enhanced security features:

- Tokenization: Your actual credit card number is never shared with the merchant. Instead, a unique token is used for each transaction, reducing the risk of fraud.

- Biometric Authentication: Transactions are often secured with fingerprint or facial recognition, adding an extra layer of protection.

5. Escrow Services

For high-value transactions, consider using an escrow service:

- Third-Party Protection: An escrow service holds the payment until the buyer receives and approves the goods or services. This provides protection for both parties.

Comparison Table

| Payment Method | Fraud Protection | Purchase Protection | Dispute Rights | Security Features |

|---|---|---|---|---|

| Credit Cards | High | High | Yes | EMV chip, fraud monitoring |

| PayPal | Medium | Medium | Yes | Buyer and seller protection |

| Venmo | Limited | Limited | Yes | Dispute resolution |

| Apple Pay/Google Pay | High | N/A | N/A | Tokenization, biometric authentication |

| Escrow Services | High | High | Yes | Third-party holding of funds |

Choosing the right payment method can significantly impact your ability to recover funds in case of fraud or disputes. For more information on making smart financial choices, visit money-central.com.

Secure Payment

Secure Payment

7. How to Improve Your Financial Security When Using Digital Payment Apps

Can you get your money back on Zelle? While digital payment apps offer convenience, it’s essential to take steps to protect your financial security. Here are some actionable tips to help you stay safe when using these apps.

1. Use Strong, Unique Passwords

- Create Complex Passwords: Use a combination of uppercase and lowercase letters, numbers, and symbols.

- Avoid Reusing Passwords: Use a different password for each of your accounts.

- Use a Password Manager: Consider using a password manager to securely store and generate strong passwords.

2. Enable Two-Factor Authentication (2FA)

- Add an Extra Layer of Security: 2FA requires a second form of verification, such as a code sent to your phone, in addition to your password.

- Enable 2FA on All Accounts: Turn on 2FA for all your digital payment apps and other important accounts.

3. Monitor Your Accounts Regularly

- Check Transactions Frequently: Review your transaction history regularly for any unauthorized or suspicious activity.

- Set Up Transaction Alerts: Configure your apps to send you notifications for every transaction.

4. Be Cautious of Phishing Scams

- Verify Emails and Messages: Be wary of emails or messages asking for your personal information. Always verify the sender’s identity by contacting the organization directly.

- Avoid Clicking Suspicious Links: Do not click on links in emails or messages from unknown or suspicious sources.

5. Keep Your Software Updated

- Update Apps and Operating Systems: Regularly update your apps and operating systems to patch security vulnerabilities.

- Install Antivirus Software: Use reliable antivirus software on your devices to protect against malware and other threats.

6. Use Biometric Authentication

- Enable Fingerprint or Facial Recognition: Use fingerprint or facial recognition for added security when logging into your digital payment apps.

7. Limit Account Access

- Review Authorized Devices: Check which devices have access to your accounts and remove any that are no longer in use.

- Log Out After Use: Always log out of your accounts when you’re finished using them, especially on shared devices.

8. Be Mindful of Public Wi-Fi

- Avoid Sensitive Transactions: Avoid making sensitive transactions on public Wi-Fi networks, as they are less secure.

- Use a VPN: Consider using a Virtual Private Network (VPN) to encrypt your internet traffic when using public Wi-Fi.

9. Educate Yourself About Scams

- Stay Informed: Keep up-to-date with the latest scams and fraud tactics.

- Share Information: Share what you learn with your friends and family to help them stay safe as well.

By taking these steps, you can significantly enhance your financial security and protect yourself from fraud when using digital payment apps. For more expert advice and resources, visit money-central.com.

8. The Role of Banks in Protecting Consumers from Zelle Fraud

Can you get your money back on Zelle? Banks play a crucial role in protecting consumers from Zelle fraud. While Zelle itself has certain policies and security measures, banks are on the front lines of fraud prevention and detection. Here’s how banks help safeguard consumers:

1. Fraud Detection Systems

- Transaction Monitoring: Banks use sophisticated algorithms to monitor transactions for suspicious activity.

- Anomaly Detection: These systems identify unusual patterns that may indicate fraud, such as large transfers or transactions from unfamiliar locations.

2. Account Security Measures

- Two-Factor Authentication (2FA): Banks offer 2FA to add an extra layer of security to your account.

- Biometric Authentication: Many banks now support biometric authentication, such as fingerprint or facial recognition, for logging into accounts and authorizing transactions.

3. Customer Education and Awareness

- Fraud Prevention Tips: Banks provide educational resources to help customers recognize and avoid scams.

- Security Alerts: Banks send out alerts about common scams and security threats.

4. Investigation and Resolution of Fraud Claims

- Fraud Reporting: Banks have dedicated channels for reporting fraud, such as fraud hotlines and online reporting tools.

- Investigation Process: When a fraud claim is filed, banks conduct a thorough investigation to determine whether the transaction was unauthorized.

5. Compliance with Regulations

- Regulation E: Banks must comply with Regulation E of the Electronic Fund Transfer Act, which protects consumers from unauthorized electronic fund transfers.

- Liability Limits: Regulation E sets limits on a consumer’s liability for unauthorized transfers, provided the consumer reports the fraud promptly.

6. Collaboration with Zelle

- Information Sharing: Banks work with Zelle to share information about fraud trends and security threats.

- Coordinated Efforts: Banks and Zelle collaborate to develop and implement new security measures.

7. Reimbursement Policies

- Unauthorized Transfers: If a bank determines that a Zelle transaction was unauthorized, they may reimburse the customer for the loss.

- Case-by-Case Basis: Reimbursement policies can vary depending on the bank and the specific circumstances of the fraud.

How to Work with Your Bank

- Report Fraud Promptly: The sooner you report fraud, the better your chances of recovering your money.

- Provide Detailed Information: Give your bank as much information as possible about the fraud, including transaction details and a description of the incident.

- Follow Instructions: Follow your bank’s instructions for filing a fraud claim and providing documentation.

- Stay in Communication: Keep in touch with your bank to check on the status of your claim and provide any additional information they may need.

For more guidance on protecting your finances and working with your bank, visit money-central.com.

Financial Security

Financial Security

9. Future of Zelle and Consumer Protection

Can you get your money back on Zelle? The future of Zelle and consumer protection is an evolving landscape. As digital payment methods become more prevalent, there’s increasing pressure to enhance security and protect consumers from fraud and scams. Here are some potential developments on the horizon:

1. Enhanced Security Measures

- Advanced Authentication: Expect to see more sophisticated authentication methods, such as behavioral biometrics and multi-factor authentication, to verify users’ identities.

- Real-Time Fraud Detection: AI-powered fraud detection systems will become more adept at identifying and preventing fraudulent transactions in real time.

2. Regulatory Changes

- Increased Scrutiny: Regulatory bodies like the Consumer Financial Protection Bureau (CFPB) are likely to increase their oversight of digital payment platforms like Zelle.

- Stronger Consumer Protections: New regulations may be introduced to provide stronger consumer protections for digital payment transactions, including clearer guidelines for fraud claims and reimbursement.

3. Industry Collaboration

- Information Sharing: Greater collaboration among banks, payment processors, and law enforcement agencies will help to share information about fraud trends and identify scammers more effectively.

- Industry Standards: The development of industry-wide standards for security and consumer protection will help to create a more consistent and secure payment ecosystem.

4. Consumer Education

- Awareness Campaigns: More comprehensive consumer education campaigns will help to raise awareness about the risks of digital payment scams and provide tips for staying safe.

- Financial Literacy Programs: Financial literacy programs will equip consumers with the knowledge and skills they need to manage their finances and avoid fraud.

5. Dispute Resolution Mechanisms

- Streamlined Processes: Digital payment platforms may introduce more streamlined dispute resolution processes to make it easier for consumers to report fraud and seek reimbursement.

- Mediation Services: Mediation services may be offered to help resolve disputes between consumers and payment platforms.

6. Technological Innovations

- Blockchain Technology: Blockchain technology could be used to create more secure and transparent payment systems.

- Decentralized Identity Solutions: Decentralized identity solutions could give consumers more control over their personal information and reduce the risk of identity theft.

7. Zelle’s Own Initiatives

- Enhanced User Verification: Zelle may implement more rigorous user verification processes to prevent scammers from creating fake accounts.

- Transaction Monitoring: Zelle may enhance its transaction monitoring capabilities to identify and flag suspicious transactions more effectively.

The future of Zelle and consumer protection will depend on a combination of technological innovation, regulatory action, industry collaboration, and consumer education. By staying informed and taking proactive steps to protect your financial security, you can navigate the evolving digital payment landscape with confidence. Visit money-central.com for the latest insights and advice on managing your finances and staying safe from fraud.

10. FAQs About Getting Your Money Back on Zelle

Can you get your money back on Zelle? Here are some frequently asked questions to provide you with clear and concise answers about Zelle’s policies and your options.

1. Can I cancel a Zelle payment after it’s been sent?

- Answer: You can only cancel a Zelle payment if the recipient hasn’t yet enrolled in Zelle. Once the recipient is enrolled, the payment is typically irreversible.

2. What should I do if I accidentally sent money to the wrong person on Zelle?

- Answer: Contact your bank immediately and explain the situation. They may be able to contact the recipient’s bank to request a return of the funds, but this is not guaranteed.

3. Is Zelle responsible for refunding my money if I get scammed?

- Answer: Zelle’s policy states that it is not responsible for losses resulting from scams or fraud if you authorized the transaction. However, you should still report the incident to your bank, as they may investigate and potentially reimburse you.

4. What is Regulation E, and how does it protect me when using Zelle?

- Answer: Regulation E, under the Electronic Fund Transfer Act, protects consumers from unauthorized electronic fund transfers. If you report an unauthorized Zelle transaction promptly, your bank may be required to investigate and potentially reimburse you.

5. How quickly should I report a Zelle scam to my bank?

- Answer: You should report the scam to your bank as soon as you notice the fraudulent activity. The sooner you report it, the better your chances of recovering your money.

6. Can I file a chargeback for a Zelle transaction?

- Answer: No, Zelle does not offer chargeback protection like credit cards. Zelle transactions are designed to be similar to cash transactions, meaning that once a payment is sent, it’s difficult to reverse.

7. What information do I need to provide when reporting a Zelle scam to my bank?

- Answer: You should provide the date and time of the transaction, the amount of money involved, the recipient’s information (name, email address, or phone number), transaction details, and a description of the incident.

8. Will filing a police report increase my chances of getting my money back from a Zelle scam?

- Answer: Yes, filing a police report can provide additional documentation for your case and may be required by your bank.

9. Are there any alternative payment methods that offer better protection than Zelle?

- Answer: Yes, credit cards and PayPal offer stronger consumer protections, including fraud protection, purchase protection, and dispute rights.

10. What steps can I take to protect myself from Zelle scams in the future?

- Answer: Only send money to people you know and trust, verify requests for money, be wary of urgency, protect your personal information, and monitor your account regularly.

For more detailed information and expert advice on managing your finances and protecting yourself from fraud, visit money-central.com.

We hope this comprehensive guide has helped you understand your options. At money-central.com, we provide a range of articles, tools, and resources to help you navigate the complexities of personal finance. Don’t wait until it’s too late – take control of your financial future today. Check out our latest articles, use our budget planning tools, and connect with financial advisors who can provide personalized guidance.