Are you wondering, “Can You Pull Money Out Of An Hsa?” Absolutely! At money-central.com, we understand the importance of managing your Health Savings Account (HSA) effectively. This comprehensive guide provides a clear understanding of how and when you can access your HSA funds, ensuring you can confidently navigate your healthcare expenses. Unlock financial flexibility with your HSA today and explore the best strategies for managing your healthcare savings, maximizing tax advantages, and planning for future medical expenses.

1. What is a Health Savings Account (HSA)?

A Health Savings Account (HSA) is a tax-advantaged savings account that can be used for healthcare expenses. It is available to individuals who have a high-deductible health insurance plan (HDHP). According to research from New York University’s Stern School of Business, HSAs are becoming increasingly popular as a way to save for medical expenses due to their triple tax advantage. These advantages include:

- Tax-deductible contributions: Contributions to an HSA are tax-deductible, meaning they reduce your taxable income.

- Tax-free growth: The money in your HSA grows tax-free.

- Tax-free withdrawals: Withdrawals for qualified medical expenses are tax-free.

This makes an HSA a powerful tool for managing healthcare costs and saving for the future.

2. When Can You Withdraw Money From an HSA?

You can withdraw money from your HSA at any time, but the tax implications depend on how you use the funds and your age.

2.1. Withdrawals Before Age 65

Before the age of 65, you can withdraw money from your HSA to pay for qualified medical expenses. According to the IRS, qualified medical expenses are those that would generally qualify for the medical expense deduction. These expenses include:

- Copays

- Coinsurance

- Deductibles

- Prescription medications

- Dental care

- Vision care

- And many other healthcare-related costs

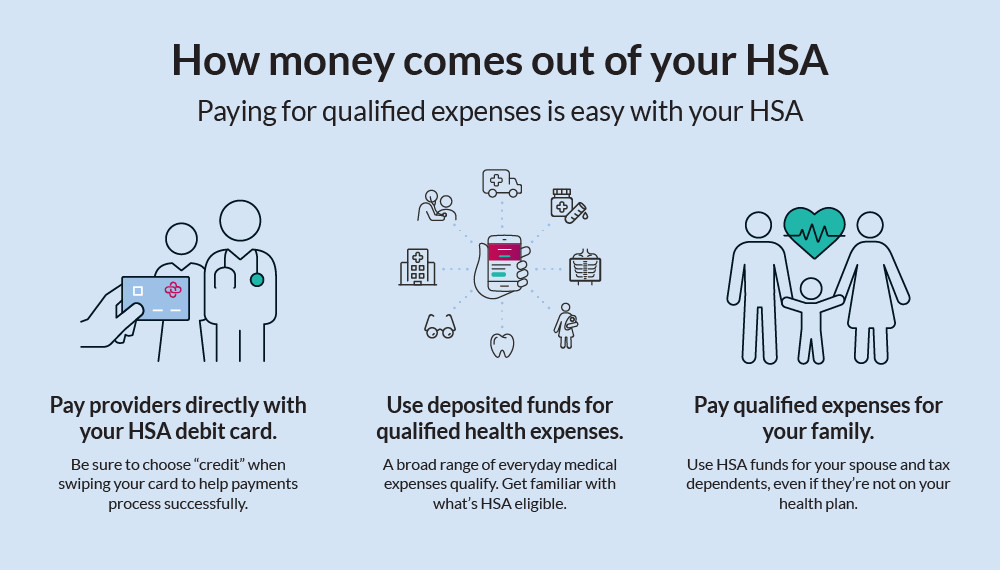

HSA infographic how money comes out of HSA

HSA infographic how money comes out of HSA

If you use your HSA funds for non-qualified expenses before age 65, the withdrawn amount is subject to income tax and a 20% penalty.

2.2. Withdrawals After Age 65

After the age of 65, the rules for HSA withdrawals change. While you can still withdraw money tax-free for qualified medical expenses, withdrawals for non-qualified expenses are treated differently.

- Qualified Medical Expenses: Withdrawals for qualified medical expenses remain tax-free.

- Non-Qualified Expenses: Withdrawals for non-qualified expenses are subject to income tax but are no longer subject to the 20% penalty. This means that after age 65, your HSA functions more like a traditional retirement account.

This flexibility makes the HSA a valuable tool for retirement planning, allowing you to use the funds for healthcare expenses or other needs without penalty.

3. What Are Qualified Medical Expenses?

Qualified medical expenses are costs for medical care that the IRS allows you to deduct from your taxes. These expenses include amounts paid for the diagnosis, cure, mitigation, treatment, or prevention of disease, and for treatments affecting any part or function of the body. Here’s a more detailed list:

3.1. Common Qualified Medical Expenses

- Medical Bills: This includes payments to doctors, dentists, surgeons, and other medical practitioners.

- Prescription Drugs: Costs for prescription medications are qualified medical expenses.

- Medical Equipment: Expenses for equipment like wheelchairs, crutches, and oxygen equipment are covered.

- Diagnostic Tests: Costs for tests like X-rays, MRIs, and lab tests are qualified.

- Mental Health Care: Payments for psychiatric and psychological care qualify.

- Substance Abuse Treatment: Costs for treatment at a substance abuse rehabilitation center are eligible.

- Long-Term Care: Expenses for long-term care services, including nursing homes, can be covered.

- Insurance Premiums: Under certain conditions, such as COBRA coverage or Medicare premiums, insurance premiums can be paid with HSA funds.

3.2. Less Obvious Qualified Medical Expenses

- Acupuncture: Costs for acupuncture treatments can be covered.

- Artificial Limbs: Expenses for artificial limbs are qualified.

- Chiropractic Services: Payments for chiropractic services are eligible.

- Fertility Treatments: Costs for fertility enhancement treatments can be covered.

- Home Health Care: Expenses for home health care services are qualified.

- Special Education: Costs for special education for a child with a disability can be covered.

- Transportation Costs: Incidental expenses for transportation, parking, meals, and lodging required for medical treatment can be eligible.

3.3. Expenses That Are Not Qualified

It’s important to know what expenses do not qualify for tax-free withdrawals from an HSA. These include:

- Cosmetic Surgery: Unless it’s medically necessary, cosmetic surgery is not a qualified medical expense.

- Non-Prescription Medications: Over-the-counter medications are generally not qualified unless prescribed by a doctor.

- Health Club Dues: Membership fees for health clubs are not eligible.

- Personal Care Items: Items like toiletries and personal hygiene products are not qualified medical expenses.

For a comprehensive list of qualified medical expenses, you can refer to IRS Publication 502, “Medical and Dental Expenses.”

4. How to Withdraw Funds From Your HSA

Withdrawing funds from your HSA is typically a straightforward process. Most HSAs offer several convenient options for accessing your money.

4.1. HSA Debit Card

Many HSAs provide a debit card that is linked directly to your account. This card can be used to pay for qualified medical expenses at the point of sale, just like a regular debit card. Simply swipe the card at the doctor’s office, pharmacy, or other healthcare provider, and the funds will be deducted from your HSA.

4.2. Online Bill Payment

Some HSAs offer online bill payment services that allow you to pay your medical bills directly from your account. You can log in to your HSA account online, enter the details of the bill, and authorize the payment. The HSA administrator will then send the payment to the healthcare provider on your behalf.

4.3. Check

Some HSAs may provide you with checks that can be used to pay for qualified medical expenses. You can write a check to your healthcare provider and use it to cover the cost of your treatment.

4.4. Reimbursement

If you pay for a qualified medical expense out-of-pocket, you can reimburse yourself from your HSA. To do this, you will need to submit a claim to your HSA administrator, along with documentation of the expense, such as a receipt orExplanation of Benefits (EOB). Once the claim is approved, the HSA administrator will send you a check or deposit the funds into your bank account.

4.5. Record Keeping

Regardless of how you choose to withdraw funds from your HSA, it’s important to keep detailed records of all your qualified medical expenses. This will help you track your spending, ensure that you are only withdrawing funds for eligible expenses, and provide documentation in case you are ever audited by the IRS.

5. What Happens if You Withdraw Funds for Non-Qualified Expenses?

If you withdraw funds from your HSA for non-qualified expenses before age 65, the withdrawn amount is subject to income tax and a 20% penalty. This can significantly reduce the value of your HSA, so it’s important to use your funds wisely.

5.1. Reporting Non-Qualified Withdrawals

If you make a non-qualified withdrawal from your HSA, you will need to report it on your tax return. You will receive a Form 1099-SA from your HSA administrator, which will show the amount of the withdrawal. You will then need to include this amount as income on your tax return and pay the applicable taxes and penalties.

5.2. Exceptions to the Penalty

There are a few exceptions to the 20% penalty for non-qualified withdrawals. The penalty does not apply if:

- You are over age 65.

- You become disabled.

- You die.

In these cases, the withdrawal is still subject to income tax, but the penalty is waived.

6. How to Withdraw Funds From an Investment HSA

If your HSA allows you to invest your contributions, withdrawing funds may involve an additional step.

6.1. Transferring Funds to Your Cash Account

Before you can withdraw funds from your investment HSA, you may need to transfer them from your investment account to your cash account. This can usually be done online or by contacting your HSA administrator.

6.2. Selling Investments

If you don’t have enough cash in your investment account to cover the withdrawal, you may need to sell some of your investments. This can also be done online or by contacting your HSA administrator. Keep in mind that selling investments may have tax implications, so it’s important to consult with a financial advisor before making any decisions.

6.3. Withdrawing Funds

Once the funds are in your cash account, you can withdraw them using one of the methods described above, such as an HSA debit card, online bill payment, or reimbursement.

7. Can You Withdraw From One HSA to Fund Another?

Yes, you can withdraw funds from one HSA to fund another through a process called a rollover or transfer.

7.1. Rollover

A rollover involves withdrawing the funds from your existing HSA and depositing them into a new HSA within 60 days. You can only do one rollover per 12-month period.

7.2. Transfer

A transfer involves directly moving the funds from your existing HSA to a new HSA. There are no limits on how often you can transfer funds.

8. HSA Contribution Limits and Withdrawal Limits

While there are no limits on the number of withdrawals you can make from your HSA, there are limits on the amount you can contribute each year. The IRS sets these limits annually, and they vary based on whether you have individual or family coverage.

| Category | 2023 Limit | 2024 Limit |

|---|---|---|

| Individual | $3,850 | $4,150 |

| Family | $7,750 | $8,300 |

| Catch-Up (Age 55+) | $1,000 | $1,000 |

Staying within these contribution limits is crucial to avoid penalties and maximize the tax benefits of your HSA.

9. Common Questions About HSA Withdrawals

9.1. Can I Use My HSA to Pay for My Spouse’s or Dependents’ Medical Expenses?

Yes, you can use your HSA to pay for the qualified medical expenses of your spouse and dependents, even if they are not covered by your health insurance plan.

9.2. Can I Use My HSA to Pay for Long-Term Care Expenses?

Yes, you can use your HSA to pay for long-term care expenses, including nursing home care and home healthcare services.

9.3. Can I Use My HSA to Pay for Health Insurance Premiums?

In general, you cannot use your HSA to pay for health insurance premiums. However, there are a few exceptions, such as:

- COBRA premiums

- Health insurance premiums while receiving unemployment compensation

- Medicare premiums (including Medicare Parts B and D)

9.4. What Happens to My HSA if I No Longer Have a High-Deductible Health Plan?

If you no longer have a high-deductible health plan, you can still keep your HSA and use the funds to pay for qualified medical expenses. However, you can no longer contribute to the account.

9.5. What Happens to My HSA if I Die?

If you die, your HSA will pass to your beneficiary. If your beneficiary is your spouse, the HSA will become their HSA. If your beneficiary is someone else, the HSA will be liquidated, and the funds will be subject to income tax.

10. Maximizing Your HSA Benefits

To make the most of your HSA, consider these strategies:

10.1. Contribute the Maximum Amount

If possible, contribute the maximum amount to your HSA each year to take advantage of the tax benefits and build your savings.

10.2. Invest Your HSA Funds

If your HSA allows it, invest your funds to potentially grow your savings faster.

10.3. Pay for Qualified Medical Expenses With Your HSA

Use your HSA to pay for qualified medical expenses to avoid taxes and penalties.

10.4. Keep Detailed Records

Keep detailed records of all your qualified medical expenses to ensure you are only withdrawing funds for eligible expenses.

10.5. Plan for Retirement

Use your HSA as a retirement savings tool by saving for future healthcare expenses.

FAQ: Understanding HSA Withdrawals

1. Can I withdraw money from my HSA for non-medical expenses?

Yes, but if you’re under 65, it’s subject to income tax and a 20% penalty. After 65, it’s taxed as regular income.

2. What are considered qualified medical expenses for HSA withdrawals?

Qualified expenses include doctor visits, prescriptions, dental care, vision care, and more, as defined by the IRS.

3. How do I withdraw funds from my HSA?

Most HSAs offer debit cards, online bill payments, checks, and reimbursement options for out-of-pocket expenses.

4. Are there any limits to the number of withdrawals I can make from my HSA?

No, you can make unlimited withdrawals, but contributions are limited annually by the IRS.

5. Can I use my HSA to pay for my family’s medical expenses?

Yes, you can use your HSA to pay for qualified medical expenses for your spouse and dependents.

6. What happens to my HSA if I switch to a non-HDHP health plan?

You can keep your HSA and use the funds, but you can no longer contribute to the account.

7. Can I transfer funds from one HSA to another?

Yes, you can transfer funds through a rollover (once per year) or a direct transfer (unlimited).

8. What happens to my HSA if I die?

It passes to your beneficiary; if it’s your spouse, it becomes their HSA. Otherwise, it’s liquidated and subject to income tax.

9. Is there a deadline for submitting HSA reimbursement claims?

Generally, there is no specific deadline, but it’s best to submit claims promptly to manage your records efficiently.

10. Can I use my HSA to pay for Medicare premiums?

Yes, you can use your HSA to pay for Medicare premiums, including Medicare Parts B and D.

Understanding the ins and outs of HSA withdrawals empowers you to make informed decisions about your healthcare finances. By following these guidelines, you can effectively manage your HSA and maximize its benefits for both short-term and long-term financial well-being.

At money-central.com, we’re dedicated to providing you with the knowledge and resources you need to achieve your financial goals. Our platform offers comprehensive guides, tools, and expert advice to help you navigate the complexities of personal finance. Whether you’re looking to optimize your HSA, plan for retirement, or manage your investments, money-central.com is your trusted partner on the path to financial success.

Ready to take control of your financial future? Visit money-central.com today to explore our full range of resources and connect with financial experts who can provide personalized guidance. Your journey to financial freedom starts here.

Address: 44 West Fourth Street, New York, NY 10012, United States

Phone: +1 (212) 998-0000

Website: money-central.com