Do You Make Money During Residency? Yes, residents in the United States receive a salary, offering a financial lifeline during their training years, according to money-central.com. While it might not feel like a fortune given the hours and debt, understanding your income, managing your finances, and exploring debt repayment options are crucial steps toward financial well-being. Let’s explore the realities of resident salaries, financial planning tips, and resources available to help you navigate this challenging yet rewarding phase, and reduce financial stress.

1. What is the Average Resident Salary in the US?

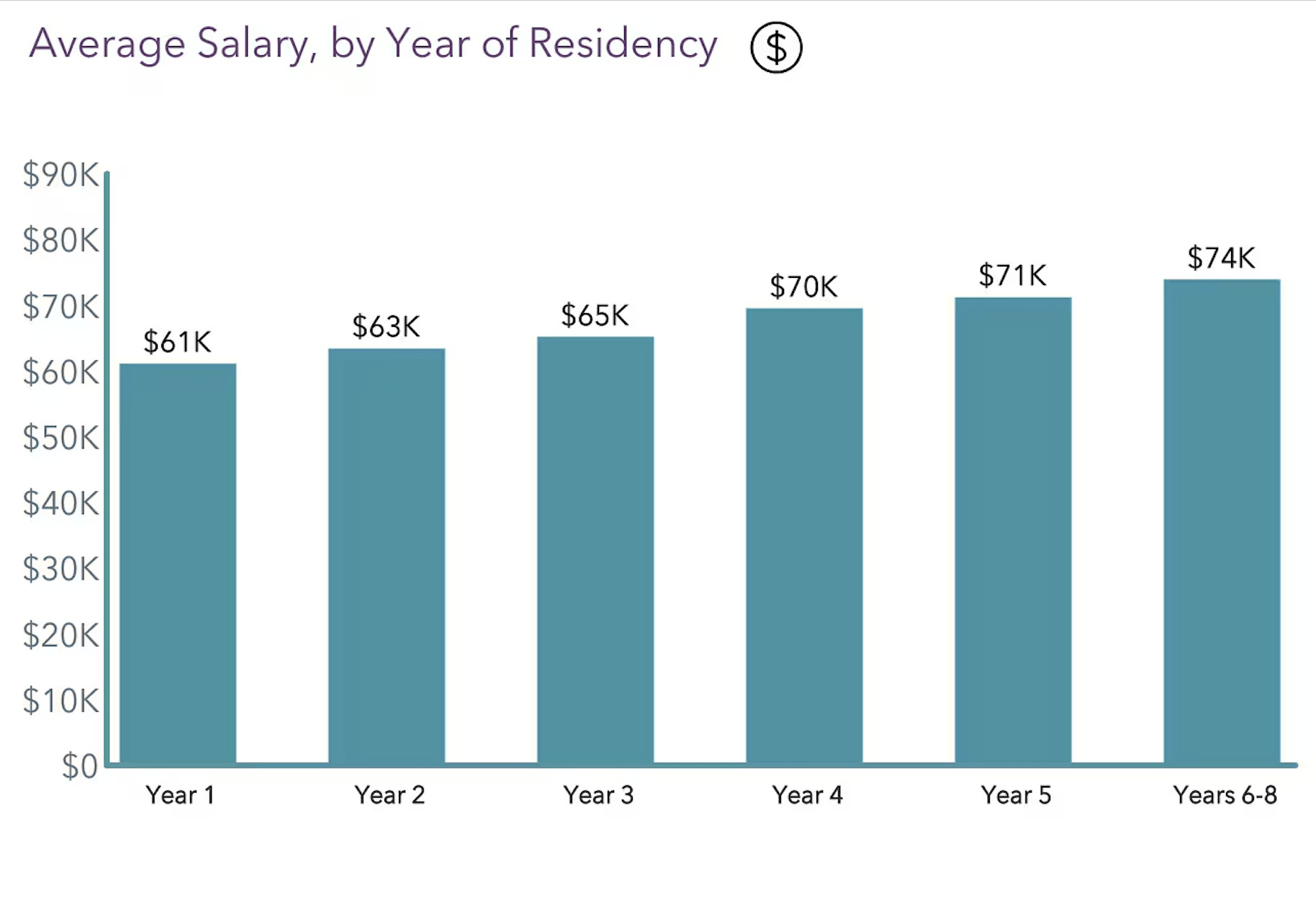

The average resident salary in the United States is approximately $67,400 per year, according to a 2023 Medscape Report. Although this number is an average, keep in mind that several factors affect the actual amount a resident makes. These factors include geographic location, specialty, and postgraduate year (PGY).

1.1 How Does Location Affect Resident Salary?

Location significantly impacts a resident’s salary due to differences in cost of living and regional demand for medical professionals. Areas with higher living costs, such as New York City or California, may offer slightly higher salaries to compensate for the increased expenses.

1.2 Which Medical Specialties Pay Residents the Most?

Some specialties tend to offer higher resident salaries due to longer hours or higher demand. While specific numbers fluctuate annually, surgical specialties and those requiring extensive on-call hours may provide slightly better compensation packages. It’s crucial to research salaries specific to your chosen field.

1.3 How Does a Resident’s Salary Increase Over Time?

Resident salaries typically increase with each postgraduate year (PGY). As residents gain experience and take on more responsibilities, their compensation reflects their growing expertise. The percentage increase varies, but it’s a steady climb toward a more substantial income as an attending physician.

2. What is the Hourly Rate for a Medical Resident?

The hourly rate for a medical resident varies significantly based on the number of hours worked per week. Given the demanding schedules, residents often find their hourly pay can be surprisingly low.

2.1 How Many Hours Does a Resident Typically Work per Week?

Residents often work long hours, typically between 50 to 80 hours per week, sometimes even more. The Accreditation Council for Graduate Medical Education (ACGME) has set a limit of 80 hours per week, averaged over a four-week period, to prevent burnout and ensure patient safety.

2.2 How is the Hourly Rate Calculated for Residents?

To calculate the hourly rate, divide the annual salary by the total number of hours worked in a year. For instance, if a resident earns $60,000 annually and works 60 hours per week, their hourly rate would be approximately $19.23. Here’s the calculation:

- Annual hours worked: 60 hours/week * 52 weeks/year = 3120 hours

- Hourly rate: $60,000 / 3120 hours = $19.23/hour

2.3 How Does This Compare to Other Professions?

The hourly rate of a resident, when considering the extensive hours and high level of education required, is often lower than other professions with similar demands. It is essential to consider this discrepancy and explore strategies to manage finances effectively.

3. What are Common Resident Expenses?

Residents face a variety of expenses that can strain their finances. Understanding these costs is the first step toward effective financial planning.

3.1 How Much Do Residents Pay in Rent and Housing Costs?

Housing is typically one of the most significant expenses. Rent varies depending on location but can easily range from $1,000 to $3,000 per month. Owning a home involves additional costs such as property taxes, insurance, and maintenance.

3.2 What Other Living Expenses Should Residents Consider?

Beyond housing, residents need to budget for groceries, utilities, transportation, and personal care items. These expenses can quickly add up, requiring careful management and prioritization.

3.3 Are There any Additional Costs Unique to Residents?

Residents also face unique costs such as medical licensing fees, professional society memberships, and educational resources. Disability insurance is particularly important to protect against unforeseen health issues that could impact their ability to work.

4. Do Residents Have to Pay Back Student Loans During Residency?

Yes, residents typically need to address their student loans during residency, but they have several options for managing repayment. Income-driven repayment plans are particularly beneficial during this period.

4.1 What Are Income-Driven Repayment Plans?

Income-Driven Repayment (IDR) plans set your monthly student loan payment based on your income and family size. These plans can significantly lower your monthly payments, making them more manageable during residency.

4.2 How Do These Plans Work?

IDR plans, such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), and Revised Pay As You Earn (REPAYE), calculate payments as a percentage of your discretionary income. After a set period (typically 20-25 years), any remaining balance is forgiven, though you may owe income tax on the forgiven amount.

4.3 What Are the Pros and Cons of Using These Plans?

The primary advantage of IDR plans is lower monthly payments, which can ease financial stress during residency. However, the total amount repaid over the life of the loan may be higher due to accruing interest. Additionally, the forgiven amount may be taxed as income.

5. Can Loan Forgiveness Programs Help Residents?

Loan forgiveness programs can offer significant relief to residents burdened by student debt. The Public Service Loan Forgiveness (PSLF) program is one such option.

5.1 What is Public Service Loan Forgiveness?

The Public Service Loan Forgiveness (PSLF) program forgives the remaining balance on your Direct Loans after you have made 120 qualifying monthly payments while working full-time for a qualifying employer.

5.2 Who is Eligible for PSLF?

To be eligible for PSLF, you must work for a government organization or a non-profit organization. Many residency programs affiliated with hospitals qualify, but it’s essential to confirm your employer’s eligibility.

5.3 How Can Residents Apply for PSLF?

To apply for PSLF, submit the PSLF form to the U.S. Department of Education. It’s recommended to submit the form annually and keep detailed records of your employment and payments to ensure you meet all requirements.

6. What are Some Strategies for Budgeting During Residency?

Effective budgeting is crucial for managing finances during residency. Creating a budget helps you track your income and expenses, identify areas to save money, and set financial goals.

6.1 How Can Residents Create a Realistic Budget?

Start by listing all sources of income and tracking your monthly expenses. Use budgeting apps, spreadsheets, or traditional pen and paper methods to monitor where your money is going.

6.2 Which Budgeting Apps and Tools Are Most Helpful?

Popular budgeting apps include Mint, YNAB (You Need A Budget), and Personal Capital. These tools can help you track spending, set goals, and provide insights into your financial habits.

6.3 How Can Residents Track Expenses Effectively?

Categorize your expenses to identify areas where you can cut back. Differentiate between essential and non-essential spending. Regularly review your budget and make adjustments as needed to stay on track.

7. Are There Any Tax Benefits for Residents?

Residents may be eligible for certain tax benefits that can help reduce their overall tax burden. Understanding these deductions and credits is essential for maximizing your financial resources.

7.1 What Deductions Can Residents Claim?

Common deductions for residents include student loan interest, moving expenses (if you moved for your residency), and contributions to retirement accounts. Consult a tax professional for personalized advice.

7.2 How Does the Student Loan Interest Deduction Work?

You can deduct the interest you paid on student loans during the year, up to $2,500. This deduction can lower your taxable income, resulting in a lower tax bill.

7.3 What Tax Credits Are Available to Residents?

Tax credits, such as the Lifetime Learning Credit or the American Opportunity Tax Credit, may be available if you are pursuing further education or training. These credits can directly reduce the amount of tax you owe.

8. Should Residents Invest During Residency?

While it may seem challenging to invest during residency, even small contributions to retirement accounts can have a significant impact over time. Starting early allows you to take advantage of compounding returns.

8.1 What Are the Benefits of Investing Early?

Investing early allows your money to grow exponentially over time due to compounding. Even small, consistent investments can accumulate substantial wealth over the long term.

8.2 What Types of Investment Accounts Are Suitable for Residents?

Consider opening a Roth IRA or contributing to your employer’s 401(k) plan, if available. These accounts offer tax advantages and can help you build a secure financial future.

8.3 How Can Residents Balance Debt Repayment and Investing?

Prioritize debt repayment, particularly high-interest student loans, while also making small, consistent investments. Aim to strike a balance between reducing debt and building a foundation for long-term financial security.

9. How Can Residents Improve Their Credit Score?

A good credit score is essential for securing favorable interest rates on loans and credit cards. Residents can improve their credit score by practicing responsible financial habits.

9.1 Why is a Good Credit Score Important?

A good credit score can save you money on loans, insurance, and other financial products. It also demonstrates financial responsibility to lenders and creditors.

9.2 What Factors Influence Credit Score?

Factors that influence your credit score include payment history, credit utilization, length of credit history, credit mix, and new credit.

9.3 What Steps Can Residents Take to Improve Their Credit?

To improve your credit, pay bills on time, keep credit utilization low, avoid opening too many new accounts at once, and regularly monitor your credit report for errors.

10. What Financial Resources Are Available to Residents?

Residents have access to a variety of financial resources that can help them navigate the challenges of managing money during training.

10.1 Where Can Residents Find Financial Advice?

Consider consulting with a financial advisor who specializes in working with medical professionals. They can provide personalized advice on budgeting, debt repayment, investing, and tax planning.

10.2 What Organizations Offer Financial Assistance to Residents?

Professional medical organizations, such as the American Medical Association, often offer financial resources and guidance to residents. Additionally, non-profit organizations may provide grants or scholarships to help with educational expenses.

10.3 How Can money-central.com Help Residents?

money-central.com offers a wealth of information and tools to help residents manage their finances. From budgeting templates to investment guides, our resources are designed to empower you to make informed financial decisions.

Medical Resident Finances

Medical Resident Finances

Average salary by year of residency chart. Image Credit: Medscape 2023 Resident Salary & Debt Report.

Call to Action:

Ready to take control of your finances during residency? Visit money-central.com for articles, tools, and expert advice to help you budget, manage debt, invest wisely, and achieve your financial goals. Your journey to financial well-being starts here. Address: 44 West Fourth Street, New York, NY 10012, United States. Phone: +1 (212) 998-0000. Website: money-central.com.

FAQ: Managing Your Finances During Residency

1. Is it possible to live comfortably on a resident’s salary?

Yes, it is possible to live comfortably on a resident’s salary, but it requires careful budgeting and financial planning. Understanding your expenses, utilizing budgeting tools, and making informed financial decisions are key to managing your finances effectively.

2. How can residents handle unexpected medical expenses?

Residents can handle unexpected medical expenses by having an emergency fund. Aim to save three to six months’ worth of living expenses in a readily accessible account to cover unforeseen costs such as medical bills or car repairs.

3. What is the best way for residents to pay off student loans?

The best way for residents to pay off student loans depends on their individual circumstances. Income-Driven Repayment (IDR) plans and Public Service Loan Forgiveness (PSLF) are popular options. Evaluate your income, debt, and career goals to determine the most suitable repayment strategy.

4. Are there any specific financial mistakes residents should avoid?

Yes, residents should avoid high-interest debt, such as credit card debt, and overspending on non-essential items. Neglecting to budget and plan for the future can also lead to financial challenges down the road.

5. How important is disability insurance for residents?

Disability insurance is crucial for residents, as it protects against the risk of becoming unable to work due to illness or injury. Ensure you have adequate coverage to replace a portion of your income if you become disabled.

6. Can residents use a financial advisor, or is it too expensive?

Residents can benefit from using a financial advisor, and it may not be as expensive as you think. Many advisors offer affordable services or work on a fee-only basis. The guidance and expertise of a financial advisor can help you make informed decisions and achieve your financial goals.

7. How can residents balance saving for retirement with paying off debt?

Residents can balance saving for retirement with paying off debt by prioritizing high-interest debt repayment while making small, consistent contributions to retirement accounts. Even small investments can grow significantly over time, so start early and stay consistent.

8. What are the pros and cons of deferring student loans during residency?

Deferring student loans during residency can provide temporary relief from monthly payments, but interest may continue to accrue. This can result in a higher overall debt balance. Consider Income-Driven Repayment plans as an alternative, as they offer lower payments and potential loan forgiveness.

9. Are there any grants or scholarships available to residents?

Yes, there are grants and scholarships available to residents, particularly those from underrepresented backgrounds or those pursuing research. Research and apply for these opportunities to help offset educational expenses.

10. How can residents stay motivated to manage their finances during a demanding residency program?

Residents can stay motivated to manage their finances during a demanding residency program by setting clear financial goals, tracking their progress, and celebrating small victories. Surround yourself with a supportive community and seek guidance from financial professionals when needed.