Do You Make Money In Residency? Yes, you do get paid during residency, and it’s a crucial step in your journey to becoming a fully licensed physician, allowing you to begin tackling financial obligations. At money-central.com, we provide clear insights into resident salaries, work hours, and financial strategies tailored for medical professionals. We’ll explore how residents are compensated, manage debt, and navigate their finances while in training, focusing on income-driven repayment plans, financial planning, and debt management.

1. Are You Paid During Residency? A Comprehensive Overview

Yes, you absolutely get paid during residency in the United States. While the salary might not seem like a fortune given the demanding hours, it’s a start toward financial independence. Let’s dive into the specifics of resident compensation:

- Salary Structure: Resident doctors receive an annual salary, which is paid out in regular installments, typically bi-weekly or monthly. The exact amount can vary based on factors like location, specialty, and the year of training.

- Regional Differences: Salaries tend to be higher in areas with a higher cost of living. For instance, residents in New York City or California may earn more than those in smaller, more rural states.

- Specialty Impact: Certain specialties might offer slightly higher pay due to longer hours or increased demand. For example, surgical specialties often have different compensation structures compared to primary care.

The primary role of a resident is to gain practical experience and training in their chosen medical field under the supervision of attending physicians. This hands-on experience is invaluable and is a necessary step to becoming a fully qualified doctor. However, the financial aspect can be challenging.

It’s essential to understand your financial situation clearly during residency, so you can plan accordingly.

1.1 Financial Realities of Residency

Residency comes with its own set of financial challenges. It’s a period where you’re working long hours while trying to manage student loan debt, living expenses, and future financial goals.

- Average Resident Salary: According to a 2023 Medscape report, the average resident salary in the US is around $67,400 per year.

- Cost of Living: Depending on where you live, the cost of living can eat up a significant portion of your salary.

- Debt Repayment: Many residents grapple with substantial student loan debt, making budgeting and financial planning essential.

While it might not be the most lucrative phase of your medical career, it’s a crucial stepping stone. Understanding the financial landscape of residency helps you make informed decisions and set the stage for future financial success.

2. Decoding the Average Resident Salary in the US

According to a 2023 Medscape Report, the average salary for a resident in the US is $67,400. Understanding this figure is just the beginning. Let’s break down the components that contribute to it and how it compares across different factors:

- Year-to-Year Increases: Resident salaries typically increase with each year of training. This increment is designed to acknowledge increased experience and responsibility.

- Geographical Variations: Salaries can differ widely based on location. Major metropolitan areas or states with high living costs often provide higher compensation.

- Specialty Matters: Certain specialties may offer higher pay due to the intensity and duration of training.

Knowing these factors helps you contextualize the average salary and better understand your earning potential during residency.

2.1 Factors Influencing Resident Pay

Several elements influence how much a resident earns. Let’s take a closer look:

- Location: States like California, New York, and Massachusetts, which have a higher cost of living, often offer higher resident salaries.

- Specialty: Specializations such as surgery or radiology might provide better compensation packages due to longer hours and more demanding training.

- Hospital Funding: The financial health of the hospital or institution can also impact salaries. Well-funded programs may offer more competitive pay.

Understanding these dynamics can help you make informed decisions when choosing a residency program.

2.2 Comparing Resident Salaries Across Specialties

Resident compensation can vary significantly between different medical specialties. For instance:

- Primary Care: Family medicine and internal medicine residents might earn slightly less compared to surgical specialties.

- Surgical Specialties: General surgery, neurosurgery, and orthopedic surgery often come with higher salaries due to longer hours and on-call responsibilities.

- Specialized Fields: Fields like radiology or anesthesiology may offer competitive pay because of the high demand and technical skills required.

Here’s a table illustrating approximate salary ranges across different specialties:

| Specialty | Average Annual Salary |

|---|---|

| Family Medicine | $64,000 |

| Internal Medicine | $66,000 |

| General Surgery | $69,000 |

| Radiology | $71,000 |

| Emergency Medicine | $70,000 |

Please note these are approximate figures and can vary based on location and institution.

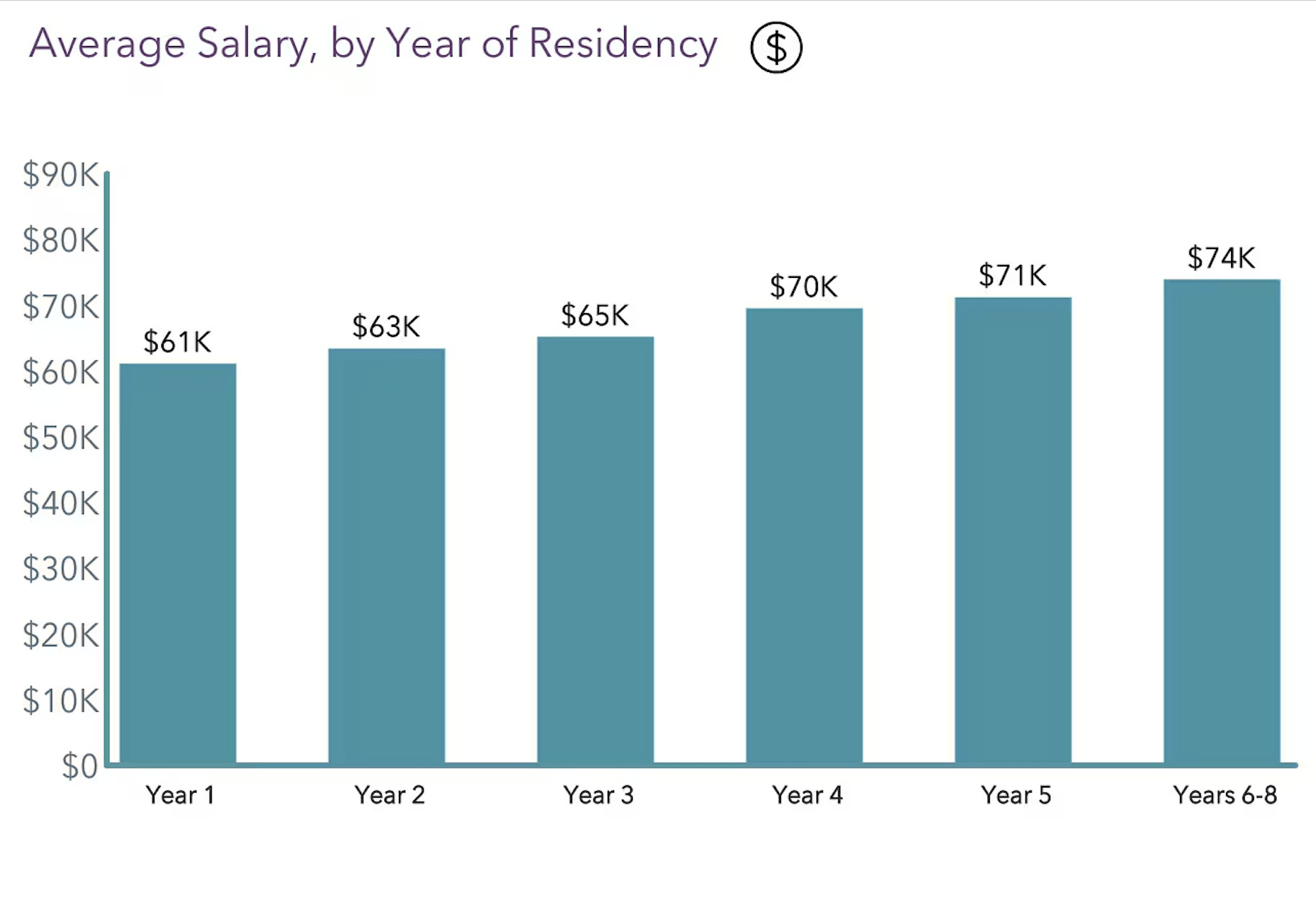

Average salary by year of residency chart

Average salary by year of residency chart

Image Credit: Medscape 2023 Resident Salary & Debt Report.

2.3 Salary Progression During Residency

One of the positive aspects of residency is that your salary typically increases with each year of training. This progression is intended to reflect your growing skills and responsibilities:

- PGY-1 (Post-Graduate Year 1): This is the first year of residency, and the salary is usually the lowest.

- PGY-2 to PGY-N: Each subsequent year brings a moderate increase in salary, acknowledging your developing expertise.

- End of Residency: By the final year, you can expect to earn significantly more than when you started, though still less than a fully licensed physician.

This steady increase can help alleviate some financial stress as you gain more experience.

3. Calculating the Hourly Rate for Residents: Is It Enough?

The hourly rate of residents varies significantly because while pay is based on a set salary, the number of hours worked can vary by specialty, institution, and year of training. Considering the demanding hours often required, let’s break down how to calculate the hourly rate and whether it’s a fair compensation.

3.1 How to Calculate Your Hourly Rate

To determine your hourly rate, you need to divide your annual salary by the total number of hours worked in a year:

- Determine Annual Hours: Multiply the average number of hours worked per week by 52 (the number of weeks in a year).

- Calculate Hourly Rate: Divide your annual salary by the total annual hours.

For example, if a resident earns $60,000 a year and works 60 hours a week:

- Annual Hours: 60 hours/week * 52 weeks/year = 3120 hours

- Hourly Rate: $60,000 / 3120 hours = $19.23/hour

Understanding this calculation can give you a clearer picture of your financial situation.

3.2 The Reality of Overtime for Residents

One of the significant challenges during residency is the potential for long and unpredictable hours. Residents often work well beyond the standard 40-hour workweek, which can impact their hourly rate and overall well-being.

- ACGME Guidelines: The Accreditation Council for Graduate Medical Education (ACGME) has set guidelines limiting resident work hours to a maximum of 80 hours per week, averaged over a four-week period.

- Non-Compliance: Despite these regulations, many residents report working more than the stipulated hours, effectively reducing their hourly pay.

- Impact on Well-being: Working excessive hours can lead to burnout, decreased job satisfaction, and potential health issues.

It’s crucial to track your hours and ensure they align with ACGME guidelines to protect your health and financial interests.

.50 per hour – How Much do Residents Make

.50 per hour – How Much do Residents Make

3.3 Minimum Wage Comparison

When residents work long hours for relatively low pay, their hourly rate can sometimes fall close to or even below the minimum wage in some states. This raises questions about fair compensation for their critical work and extensive training.

- Federal Minimum Wage: The federal minimum wage is $7.25 per hour.

- State Minimum Wage: Many states have set their minimum wage higher than the federal rate. For example, as of 2024, California’s minimum wage is $16 per hour.

- Resident Hourly Rate: As shown in the previous example, a resident earning $60,000 and working 80 hours a week makes approximately $14.42 per hour.

This comparison highlights the financial strain many residents face, especially when considering their level of education and responsibility.

4. Does a Resident’s Salary Increase During Training? Exploring Salary Growth

Yes, a resident’s salary does increase during training, but not by much compared to the salary of a licensed physician. Let’s explore how resident salaries evolve during training and what factors contribute to these changes:

- Annual Increments: Typically, resident salaries increase incrementally each year as they progress through their training.

- PGY Level: The Post-Graduate Year (PGY) level indicates the year of residency. PGY-1 residents earn the least, with salaries increasing as they advance to PGY-2, PGY-3, and so on.

- Specialty Impact: The specialty can influence the rate of salary increase. Some specialties may offer more substantial raises due to the demand and intensity of the work.

4.1 Typical Salary Progression

While the exact amounts can vary by institution and location, here is a general overview of salary progression during residency:

| PGY Level | Average Annual Salary |

|---|---|

| PGY-1 | $60,000 – $65,000 |

| PGY-2 | $63,000 – $68,000 |

| PGY-3 | $66,000 – $71,000 |

| PGY-4 | $69,000 – $74,000 |

| PGY-5+ | $72,000+ |

These figures are approximate and should be considered as a general guide.

4.2 Factors Affecting Salary Increases

Several factors can influence how much a resident’s salary increases each year:

- Institutional Policies: Each hospital or residency program has its own policies regarding salary increases.

- Collective Bargaining: Some residents are part of unions or collective bargaining agreements, which can negotiate better pay and benefits.

- Performance: While less common, exceptional performance may lead to additional bonuses or incentives.

Staying informed about these factors can help you better understand your earning potential during residency.

4.3 Long-Term Financial Implications

While salary increases during residency are helpful, it’s essential to consider the long-term financial implications:

- Debt Accumulation: The increased income can help manage day-to-day expenses, but it may not significantly reduce student loan debt.

- Future Earnings: Residency is a stepping stone to higher earnings as a fully licensed physician, which should be the primary focus.

- Financial Planning: Developing a solid financial plan during residency is crucial for long-term financial health.

Money-central.com offers resources and tools to help you create a budget, manage debt, and plan for the future.

5. Understanding the Cost of Medical Training

Let’s break down just what that kind of debt, and the interest associated with it, looks like. The cost of medical training is substantial, and understanding it is crucial for financial planning. Here are the key components of these expenses:

- Tuition Fees: Medical school tuition can range from $40,000 to $60,000 per year, depending on the institution.

- Living Expenses: Housing, food, transportation, and other living costs add significantly to the overall expense.

- Additional Costs: Fees for board exams, application processes, and professional development can also be considerable.

These costs accumulate rapidly and can result in a significant debt burden by the time you enter residency.

5.1 The Burden of Medical School Debt

One of the most significant financial challenges for medical residents is managing their student loan debt. Let’s explore the implications of this debt:

- Average Debt: The average medical school graduate has around $250,000 in student loan debt.

- Interest Rates: Interest rates on these loans can range from 6% to 8% or higher, depending on the type of loan and the prevailing market conditions.

- Repayment Options: Several repayment options are available, including income-driven repayment plans, standard repayment plans, and loan consolidation.

Managing this debt effectively is crucial for long-term financial stability.

5.2 Example of Debt and Interest Accumulation

As a resident making the average salary of $67,400 a year, that equals $5600 a month.

The average student debt coming out of medical school is approximately $250,000. Let’s be conservative again on interest rates and say the loan interest is at 7%. This puts monthly interest alone at nearly $1500 a month.

Based on income-driven repayment plans, or an IDR plan, residents can be approved for a much lower minimum payment, which can be as low as $300 a month. But keep in mind that only paying the minimum required on your debt will mean you continue to accrue over a thousand dollars of interest every month.

Let’s put it this way, even if you were somehow able to pay $2000 a month toward your medical school loans for a year, that only equates to reducing your debt by about $6000. After a year of monthly payments, you would only reduce that $250K to $244K.

It’s extremely likely that you won’t make any sort of dent in your medical school debt during residency and will come out the other side with more debt than you started with due to accrued interest.

If you’d like us to break down more exact calculations and options for paying off medical school debt in a future video, let us know in the comments.

5.3 Strategies for Managing Medical School Debt

Given the high cost of medical training and the substantial debt burden, effective debt management strategies are essential:

- Income-Driven Repayment (IDR) Plans: These plans adjust your monthly payments based on your income and family size. After a set period (typically 20-25 years), the remaining balance is forgiven.

- Loan Consolidation: Consolidating your loans can simplify the repayment process by combining multiple loans into a single loan with a fixed interest rate.

- Refinancing: Refinancing your loans may help you secure a lower interest rate, potentially saving you thousands of dollars over the life of the loan.

- Public Service Loan Forgiveness (PSLF): If you work for a qualifying non-profit or government organization, you may be eligible for PSLF, which forgives the remaining loan balance after 10 years of qualifying payments.

Money-central.com provides tools and resources to help you evaluate these options and choose the best strategy for your financial situation.

6. Resident Finances: A Hypothetical Monthly Budget Breakdown

Let’s dive into a detailed breakdown of what a resident’s monthly finances might look like. This will help illustrate the financial realities and potential challenges they face.

6.1 Monthly Income Calculation

First, let’s calculate the monthly take-home pay for a resident earning $67,400 annually:

- Annual Salary: $67,400

- Monthly Gross Income: $67,400 / 12 = $5616.67

Next, we need to account for federal taxes, which can significantly reduce the monthly income.

- Federal Income Tax: If you pay zero state tax on your income, federally, you’re looking at paying a little more than $12,000 a year in taxes, which is $1000 a month, bringing your monthly paycheck down to $4600.

6.2 Essential Expenses

After calculating the net monthly income, let’s consider essential expenses:

- Student Loan Payments: If you pay a low minimum payment of $500 toward your debt, you’re now at $4100.

- Rent: The average rent across the US is $1400 a month. That brings you down to $2700.

- Groceries: A low grocery budget for one person is approximately $300, bringing your paycheck down to $2400.

- Transportation: Once again, let’s lean conservative and say your monthly transportation costs are only $500 a month, leaving a mere $1900 left.

6.3 Discretionary and Unexpected Expenses

With only $1900 remaining, residents need to cover a range of other expenses:

- Dining Out: Costs for occasional meals outside.

- Utilities: Electricity, water, gas, and internet.

- Phone Bill: Monthly cell phone expenses.

- Fitness Expenses: Gym memberships or workout classes.

- Medical Expenses: Co-pays and other healthcare costs.

- Travel: Occasional trips and vacations.

- Social Events: Costs for entertainment and socializing.

- Holiday Gifts: Expenses for gifts during holidays.

- Coffee: Daily coffee expenses.

- Prescriptions: Costs for medications.

- Clothing and New Scrubs: Expenses for professional attire.

- Unforeseen Emergencies: Unexpected costs for repairs or emergencies.

- Disability Insurance: Costs for protecting your income.

- Retirement Account Contributions: Saving for retirement.

- Educational Resources: Buying books or online courses for board exams.

Given these expenses, the life of a resident making $70K is far from luxurious.

7. Do Residents Feel Fairly Compensated? Gauging Satisfaction

The 2023 Resident Salary & Debt Report from Medscape shares that only 20% of residents feel fairly compensated for their work during residency. Let’s examine resident perceptions about their compensation and the factors influencing their satisfaction:

- Compensation vs. Workload: Many residents feel that their salary does not adequately reflect the number of hours they work and the level of responsibility they hold.

- Comparison with Peers: Dissatisfaction often arises when residents compare their salaries with those of other healthcare professionals, such as nurses or physician assistants.

- Debt Burden: The high burden of medical school debt exacerbates feelings of undercompensation.

7.1 Factors Influencing Job Satisfaction

Several factors play a role in how residents perceive their compensation and overall job satisfaction:

- Work-Life Balance: Residents who have a better work-life balance are generally more satisfied with their jobs, even if the pay is not ideal.

- Support from Supervisors: Supportive and understanding supervisors can significantly improve job satisfaction.

- Opportunities for Learning: Residents who feel they are gaining valuable skills and knowledge are more likely to be satisfied with their training.

7.2 Satisfaction Trends Over Time

Interestingly, satisfaction levels can change as residents progress through their training:

- Year 1: During year 1 of residency, 21% of residents reported being happy with their salary.

- Later Years: During year 8, 29% of residents reported being satisfied with how much they make.

Are residents happy with their earnings – chart by year of training

Are residents happy with their earnings – chart by year of training

Image Credit: Medscape 2023 Resident Salary & Debt Report.

Residents who were dissatisfied with their compensation felt it did not reflect their work hours and was not comparable to other medical staff.

7.3 Addressing Financial Concerns

Despite the challenges, there are ways to address financial concerns during residency:

- Budgeting: Creating and adhering to a budget can help residents manage their finances more effectively.

- Seeking Financial Advice: Consulting with a financial advisor can provide personalized strategies for debt management and investment.

- Negotiating Benefits: Some residents may have the opportunity to negotiate additional benefits, such as housing stipends or loan repayment assistance.

Money-central.com offers a range of resources to help residents improve their financial literacy and manage their finances effectively.

8. Financial Implications for Aspiring Physicians: Is It Worth It?

If you’re thinking of getting into medicine for financial reasons, understand that while it’s great money, it takes a huge investment of time and a massive opportunity cost to become a practicing physician. You’ll have nearly a decade of schooling and training that costs hundreds of thousands of dollars. And on top of that, you’ll only start making six figures after residency, which is 7-12 years after someone who decided to pursue a career in engineering, coding, finance, or entrepreneurship. Let’s weigh the pros and cons:

- Long Training Period: Becoming a licensed physician requires many years of education and training, which can delay earning potential.

- High Debt: The cost of medical school can result in significant debt, which can take years to repay.

- Delayed Gratification: It takes a long time to reach the point where you earn a substantial income as a physician.

8.1 Weighing the Financial Pros and Cons

Before embarking on a career in medicine, consider the financial advantages and disadvantages:

Pros:

- High Earning Potential: Fully licensed physicians can earn substantial incomes.

- Job Security: The demand for healthcare professionals is generally stable.

- Opportunities for Advancement: There are many opportunities for career advancement and specialization.

Cons:

- High Initial Investment: The cost of education and training is significant.

- Delayed Income: It takes many years to reach peak earning potential.

- Financial Stress: Managing debt and living expenses during training can be stressful.

8.2 Alternative Career Paths

If financial considerations are a primary concern, it’s worth exploring alternative career paths that may offer better short-term financial rewards:

- Engineering: Engineers often earn high salaries and have strong job prospects.

- Computer Science: Software developers and computer scientists are in high demand and can command excellent salaries.

- Finance: Financial analysts and investment managers can earn substantial incomes.

- Entrepreneurship: Starting your own business can offer significant financial rewards, although it also involves risk.

8.3 Making an Informed Decision

Choosing a career path is a personal decision that should be based on your values, interests, and financial goals. If you are passionate about medicine and willing to make the necessary sacrifices, the financial rewards can be significant in the long run. However, it’s essential to be realistic about the financial challenges and plan accordingly.

Money-central.com provides resources and tools to help you evaluate your financial situation, explore different career options, and make informed decisions about your future.

9. Key Strategies for Financial Success During Residency

Residency can be a financially challenging time, but with the right strategies, you can navigate it successfully and set yourself up for a secure financial future.

- Budgeting: Develop a detailed budget to track your income and expenses.

- Debt Management: Prioritize paying down high-interest debt and explore repayment options.

- Saving: Start saving early, even if it’s just a small amount each month.

9.1 Effective Budgeting Techniques

Budgeting is the cornerstone of financial management. Here are some techniques to help you create and stick to a budget:

- Track Your Expenses: Use budgeting apps or spreadsheets to monitor where your money is going.

- Set Financial Goals: Define your short-term and long-term financial goals.

- Prioritize Needs vs. Wants: Distinguish between essential needs and discretionary wants.

- Automate Savings: Set up automatic transfers to your savings account each month.

9.2 Debt Management Strategies

Managing your debt is crucial for long-term financial health. Consider these strategies:

- Prioritize High-Interest Debt: Focus on paying down debts with the highest interest rates first.

- Consolidate Debt: Consider consolidating your debts to simplify repayment and potentially lower your interest rate.

- Explore Loan Forgiveness Programs: Investigate options like Public Service Loan Forgiveness (PSLF) or income-driven repayment plans.

9.3 Building a Savings Plan

Saving early and consistently is essential for achieving your financial goals. Follow these tips:

- Set Savings Goals: Determine how much you need to save for specific goals, such as retirement or a down payment on a house.

- Automate Savings: Set up automatic transfers from your checking account to your savings account each month.

- Take Advantage of Employer-Sponsored Plans: If your employer offers a retirement plan, such as a 401(k), take advantage of it and contribute enough to receive any matching contributions.

10. Expert Financial Advice for Medical Residents

Seeking guidance from financial professionals can provide personalized strategies and insights to help you manage your finances effectively.

- Financial Advisors: Consult with a financial advisor who specializes in working with medical professionals.

- Debt Management Specialists: Work with a debt management specialist to develop a plan for paying down your student loans.

- Tax Professionals: Seek advice from a tax professional to optimize your tax strategy.

10.1 The Role of Financial Advisors

Financial advisors can provide a range of services, including:

- Budgeting and Financial Planning: Helping you create a budget and develop a comprehensive financial plan.

- Debt Management: Advising you on the best strategies for paying down your debt.

- Investment Management: Managing your investments to help you achieve your financial goals.

- Retirement Planning: Helping you plan for retirement and maximize your savings.

10.2 Finding the Right Financial Advisor

When choosing a financial advisor, consider the following factors:

- Experience: Look for an advisor who has experience working with medical professionals.

- Credentials: Check their credentials and certifications to ensure they have the necessary expertise.

- Fees: Understand their fee structure and how they are compensated.

- References: Ask for references and speak with other clients to get their feedback.

10.3 Utilizing Resources from Money-Central.com

Money-central.com offers a wealth of resources to help you manage your finances effectively.

- Articles and Guides: Access articles and guides on budgeting, debt management, and investment.

- Financial Tools and Calculators: Use our financial tools and calculators to estimate your expenses, calculate your debt repayment options, and plan for retirement.

- Expert Advice: Get insights and advice from financial experts on a range of topics.

By leveraging these resources and seeking professional advice, you can take control of your finances and achieve your financial goals during residency and beyond.

Navigating the financial aspects of residency can be challenging, but with the right information and strategies, you can successfully manage your money and set yourself up for a bright financial future. Remember, Money-central.com is here to support you every step of the way.

Address: 44 West Fourth Street, New York, NY 10012, United States

Phone: +1 (212) 998-0000

Website: money-central.com

Visit Money-central.com today to explore more articles, use our financial tools, and connect with financial experts who can help you achieve your financial goals. Take control of your financial future and thrive during your medical residency.

FAQ: Residency Finances

1. Do residents get paid during their medical residency?

Yes, residents in the U.S. are paid an annual salary during their medical residency, though it’s generally lower compared to fully licensed physicians, reflecting their training status.

2. How much do residents typically make in the U.S.?

The average resident salary in the U.S. is approximately $67,400 per year, but this amount can vary based on location, specialty, and year of training.

3. Does a resident’s salary increase each year of training?

Yes, typically a resident’s salary increases incrementally each year as they progress through their training, reflecting their growing experience and responsibilities.

4. How is the hourly rate for residents calculated, and is it a fair wage?

To calculate the hourly rate, divide the annual salary by the total hours worked in a year. Given the long hours, the hourly rate can sometimes be lower than expected, raising questions about fair compensation.

5. What are the typical expenses a resident has to cover each month?

Residents must cover essential expenses like rent, groceries, student loan payments, transportation, utilities, and additional costs such as medical expenses, insurance, and educational resources.

6. Are residents generally satisfied with their compensation during residency?

According to surveys, a minority of residents feel fairly compensated for their work, with many feeling that their salary does not reflect their workload and responsibilities.

7. How can residents effectively manage their student loan debt during residency?

Residents can explore income-driven repayment plans, loan consolidation, refinancing, and Public Service Loan Forgiveness (PSLF) to manage their student loan debt effectively.

8. What are some budgeting and financial planning tips for residents?

Effective strategies include tracking expenses, setting financial goals, prioritizing needs over wants, automating savings, and creating a detailed budget.

9. Should residents seek advice from financial advisors?

Yes, consulting with financial advisors can provide personalized strategies and insights to help residents manage their finances effectively, plan for the future, and optimize their financial well-being.

10. Where can residents find more resources for financial planning and debt management?

Resources are available at money-central.com, including articles, guides, financial tools, calculators, and expert advice on budgeting, debt management, and investment.