Do You Need To Sign A Money Order? Yes, signing a money order is a crucial step. At money-central.com, we guide you through the process, ensuring your payments are secure and valid with our money management tips. Understanding money orders and payment methods helps ensure smooth transactions, financial security, and smart money moves.

Table of Contents

1. What is a Money Order?

2. Why is Signing a Money Order Important?

3. Step-by-Step Guide on How to Sign a Money Order

4. Where to Sign a Money Order

5. What Happens if You Don’t Sign a Money Order?

6. How to Protect Your Money Order from Fraud

7. Alternatives to Money Orders

8. The Cost of a Money Order

9. How to Track a Money Order

10. Frequently Asked Questions (FAQs)

1. What is a Money Order?

A money order is a secure payment method, similar to a check, but prepaid. It’s a financial instrument guaranteeing that the funds are available, making it a reliable option for transactions, especially when a personal check isn’t viable. They are widely accepted and can be purchased at various locations, including post offices, banks, credit unions, and retail stores.

Money orders are particularly useful for people who may not have a bank account, or for situations where the recipient requires a guaranteed form of payment. Unlike personal checks, which can bounce if the payer doesn’t have sufficient funds, a money order is prepaid, reducing the risk of non-payment.

They also offer a level of anonymity, as they don’t require the payer to disclose their bank account information. This can be appealing for those who prefer to keep their financial details private. According to research from New York University’s Stern School of Business, in July 2025, money orders provide a secure and traceable method for sending funds, especially useful in transactions where personal checks or credit cards are not accepted.

2. Why is Signing a Money Order Important?

Signing a money order is essential for several reasons, and it primarily validates the payment. It confirms that you, as the purchaser, authorize the transaction. Without your signature, the money order is incomplete and may not be accepted by the recipient or the financial institution. It also serves as a security measure, preventing unauthorized use.

- Authorization: Your signature confirms that you approve the payment, assuring the recipient that the money order is legitimate.

- Security: A signed money order deters fraud. Financial institutions use the signature to verify the identity of the purchaser.

- Validity: A money order without a signature is considered incomplete. Banks and other cashing locations may reject it, causing delays and complications.

According to Forbes, unsigned money orders are often treated as void because they lack the necessary authorization from the payer.

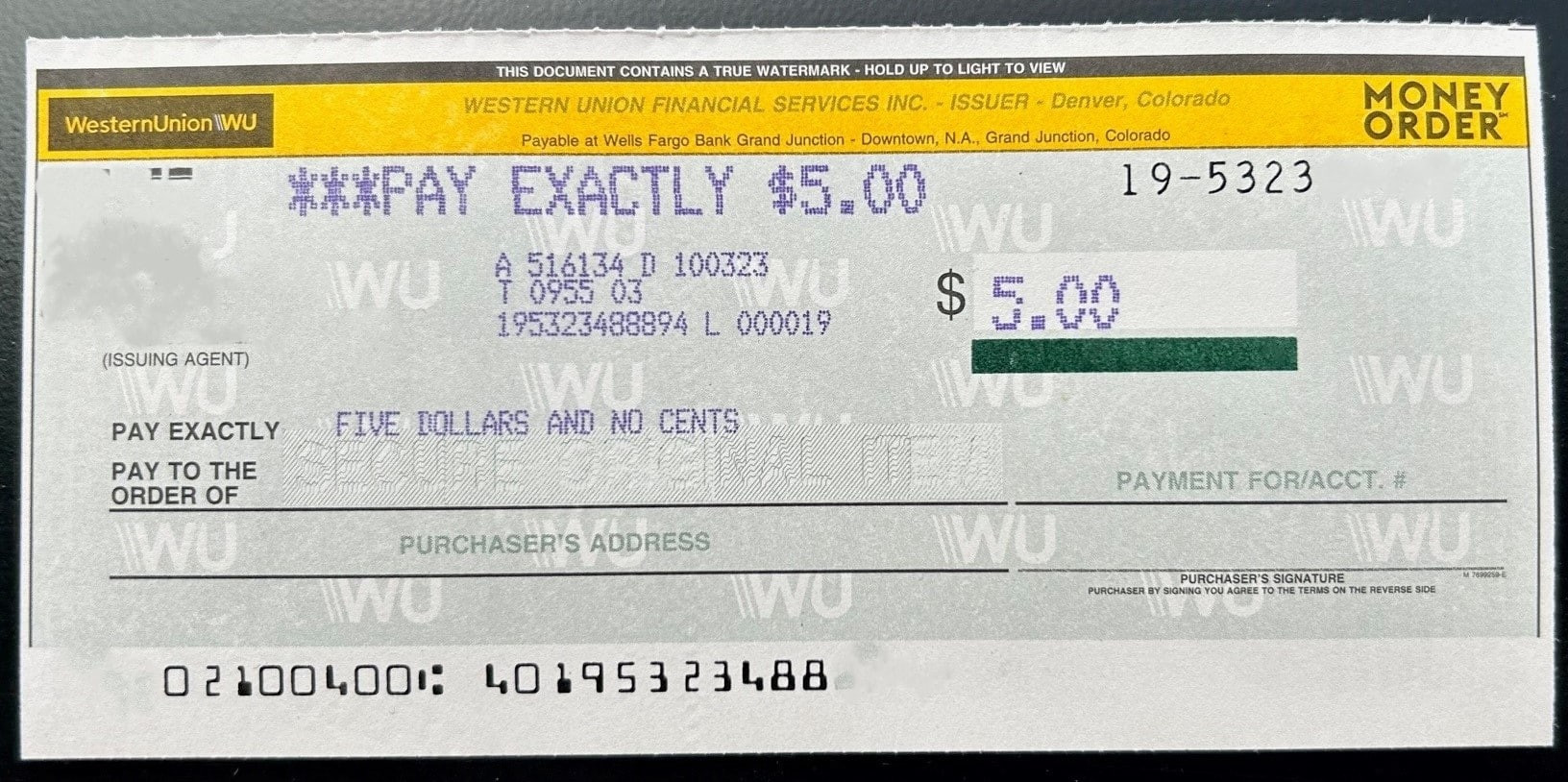

A close-up of the signature line on a money order, highlighting its importance

A close-up of the signature line on a money order, highlighting its importance

3. Step-by-Step Guide on How to Sign a Money Order

Signing a money order might seem straightforward, but following the correct steps ensures its validity. Here’s a detailed guide:

- Locate the Signature Line: Find the line on the front of the money order that says “Sign Here,” “Purchaser’s Signature,” or something similar.

- Use a Pen: Always use a pen, preferably with blue or black ink. Avoid pencils or erasable pens, as these can be altered.

- Sign Your Name: Sign your full legal name. Make sure your signature matches the name you provided when you purchased the money order.

- Avoid Signing the Back: The back of the money order is reserved for the recipient to endorse when they cash or deposit it.

Following these steps ensures that your money order is correctly signed and ready for use.

4. Where to Sign a Money Order

Knowing exactly where to sign is crucial to avoid invalidating the money order. Here’s where you need to sign:

- Front of the Money Order: The signature line for the purchaser is always on the front. Look for labels like “Sign Here,” “Purchaser’s Signature,” or similar wording.

- Designated Area: Ensure you sign only in the designated area. Signing in the wrong place can cause confusion and may lead to rejection of the money order.

- Recipient Area: Never sign the back of the money order. This area is strictly for the recipient when they are ready to cash or deposit the funds.

Always double-check the money order to identify the correct signature line before signing.

5. What Happens if You Don’t Sign a Money Order?

Failing to sign a money order can lead to several complications:

- Rejection: The most immediate consequence is that the recipient may not be able to cash or deposit the money order. Financial institutions require the purchaser’s signature to validate the payment.

- Delays: If the money order is submitted without a signature, the bank may hold the funds and contact the purchaser for verification, causing significant delays.

- Invalidation: In some cases, an unsigned money order may be considered invalid. This means the recipient cannot access the funds, and you may need to request a replacement, which can be a lengthy process.

According to a report by the Consumer Financial Protection Bureau (CFPB), unsigned money orders are a common issue leading to payment delays and customer frustration.

6. How to Protect Your Money Order from Fraud

Protecting your money order from fraud is crucial. Here are some essential tips:

- Purchase from Reputable Sources: Buy money orders only from trusted locations such as banks, post offices, and well-known retail stores.

- Fill Out Completely: Complete all required fields, including the recipient’s name, your name and address, and the memo line.

- Sign Immediately: Sign the money order as soon as you fill it out to prevent anyone else from signing it fraudulently.

- Keep the Receipt: Store your receipt in a safe place. It contains the tracking number and other information needed to verify or cancel the money order if it’s lost or stolen.

- Track Your Money Order: Use the tracking number on your receipt to monitor the status of your money order online or through a customer service hotline.

- Be Wary of Scams: Be cautious of requests for money orders from unknown individuals or businesses. Verify the legitimacy of the recipient before sending any funds.

These steps can significantly reduce the risk of fraud and ensure your money order reaches the intended recipient safely.

7. Alternatives to Money Orders

While money orders are a reliable payment method, several alternatives offer similar or even greater convenience and security:

| Payment Method | Description | Pros | Cons |

|---|---|---|---|

| Cashier’s Check | A check guaranteed by a bank, drawn on the bank’s own funds. | Highly secure, widely accepted. | Requires a bank account, may have higher fees than money orders. |

| Certified Check | A personal check that the bank guarantees has sufficient funds available. | Guaranteed funds, accepted by many recipients. | Requires a bank account, bank must certify the check. |

| Prepaid Cards | Cards loaded with a specific amount of money, usable for purchases and payments. | Convenient, can be reloaded, no bank account needed. | May have activation fees, monthly fees, and transaction fees. |

| Electronic Transfers | Online transfers through services like Zelle, PayPal, or bank-to-bank transfers. | Fast, convenient, often free or low-cost. | Requires both parties to have accounts with the service, potential security risks if not used carefully. |

| Bill Pay Services | Services offered by banks or third-party providers that allow you to pay bills online. | Convenient, automated payments, reduces the risk of missed payments. | Requires setting up accounts and providing banking information. |

Each of these options has its own advantages and disadvantages, so consider your specific needs and circumstances when choosing the best alternative to a money order.

8. The Cost of a Money Order

Understanding the costs associated with money orders is essential for budgeting and financial planning. The fees for money orders vary depending on the provider and the amount of the money order. Here’s a general overview:

- United States Postal Service (USPS): Fees range from $1.45 for money orders up to $500 to $1.95 for money orders between $500.01 and $1,000.

- Western Union: Fees vary by location and amount, but typically range from $1.50 to $10.

- MoneyGram: Similar to Western Union, fees depend on the location and amount, generally ranging from $1.50 to $11.

- Banks and Credit Unions: Fees can vary widely, with some institutions offering free money orders to their customers. Others may charge fees similar to those of USPS or other providers.

- Retail Stores: Stores like Walmart and CVS also offer money orders, with fees typically ranging from $0.70 to $1.00.

Always compare fees from different providers to find the most cost-effective option for your needs. Keep in mind that convenience and accessibility may also factor into your decision.

9. How to Track a Money Order

Tracking a money order is a valuable security measure that allows you to confirm that your payment has been received. Here’s how you can track a money order:

- Keep Your Receipt: Your receipt contains the tracking number and other essential information needed to monitor the status of your money order.

- Visit the Provider’s Website: Go to the website of the company that issued the money order (e.g., USPS, Western Union, MoneyGram).

- Enter the Tracking Number: Find the tracking tool on the website and enter the tracking number from your receipt.

- Check the Status: The website will provide updates on the status of your money order, including whether it has been cashed or deposited.

- Contact Customer Service: If you have any questions or concerns, contact the provider’s customer service hotline for assistance.

Tracking your money order gives you peace of mind and allows you to take prompt action if any issues arise.

10. Frequently Asked Questions (FAQs)

1. Can I cancel a money order?

Yes, you can cancel a money order if it hasn’t been cashed. You’ll need your receipt and may need to fill out a form and pay a fee.

2. What if I lose my money order receipt?

Contact the money order provider immediately. They may be able to help you track or cancel the money order, but it may require additional steps and documentation.

3. Is there a limit to how much a money order can be for?

Yes, the limit varies by provider. USPS has a limit of $1,000 per money order, while other providers may have different limits.

4. Can someone else sign a money order for me?

No, only the purchaser named on the money order can sign it. If you are unable to sign, you may need to explore alternative payment methods.

5. How long is a money order valid?

Money orders typically do not expire, but some providers may charge a fee for money orders that are not cashed within a certain period.

6. Can I deposit a money order into my bank account?

Yes, you can deposit a money order into your bank account. Simply endorse the back of the money order and follow your bank’s deposit procedures.

7. What should I do if my money order is stolen?

Report the theft to the money order provider immediately. Provide them with as much information as possible, including the tracking number and purchase details.

8. Can I buy a money order with a credit card?

Some providers may allow you to purchase a money order with a credit card, but this may incur additional fees. It’s best to check with the provider beforehand.

9. Are money orders traceable?

Yes, money orders are traceable using the tracking number provided on your receipt.

10. Do I need to provide ID to purchase a money order?

Yes, you typically need to provide a valid photo ID to purchase a money order, especially for larger amounts. This is to prevent fraud and ensure the security of the transaction.

Money orders offer a secure way to handle payments when checks or electronic transfers aren’t feasible. Ensuring you sign correctly and take necessary precautions will make transactions seamless. At money-central.com, we strive to equip you with the knowledge and tools for financial confidence.

For more detailed guidance, explore our articles, use our resources, and connect with financial experts at money-central.com. Address: 44 West Fourth Street, New York, NY 10012, United States. Phone: +1 (212) 998-0000. Website: money-central.com. Discover how to take control of your finances today.