It might sound unusual, but opening a Roth IRA for your child is one of the smartest financial moves you can make. If your child is earning money, even from small jobs, you have a powerful opportunity to set them up for long-term financial success. This guide explains how you can leverage your child’s earnings to kickstart their journey to wealth building through a Roth IRA.

Why Start a Roth IRA for Your Child?

You might be wondering, “Why would I open a retirement account for a teenager?” The answer lies in the incredible benefits of a Roth IRA, especially when started early in life.

Tax-Free Growth: A Lifetime Advantage

The magic of a Roth IRA is its tax advantages. Typically, you contribute money to a Roth IRA that has already been taxed. However, for children with low earned income, this can be particularly advantageous. If your child earns less than the standard deduction, they likely won’t owe federal income taxes. This means:

- Tax-free contributions: The money contributed to the Roth IRA is essentially income-tax free at the federal level and potentially at the state level.

- Tax-free growth: The investments within the Roth IRA grow without being taxed.

- Tax-free withdrawals in retirement: When your child retires, they can withdraw the money, including all the growth, completely tax-free.

This “triple tax advantage” is especially powerful for young people with a long time horizon for their investments to grow.

The Power of Compounding: Time is on Their Side

Starting to invest early is crucial because of compound interest. Albert Einstein reportedly called compound interest the “eighth wonder of the world.” It’s the snowball effect of earning returns not only on your initial investment but also on the accumulated interest.

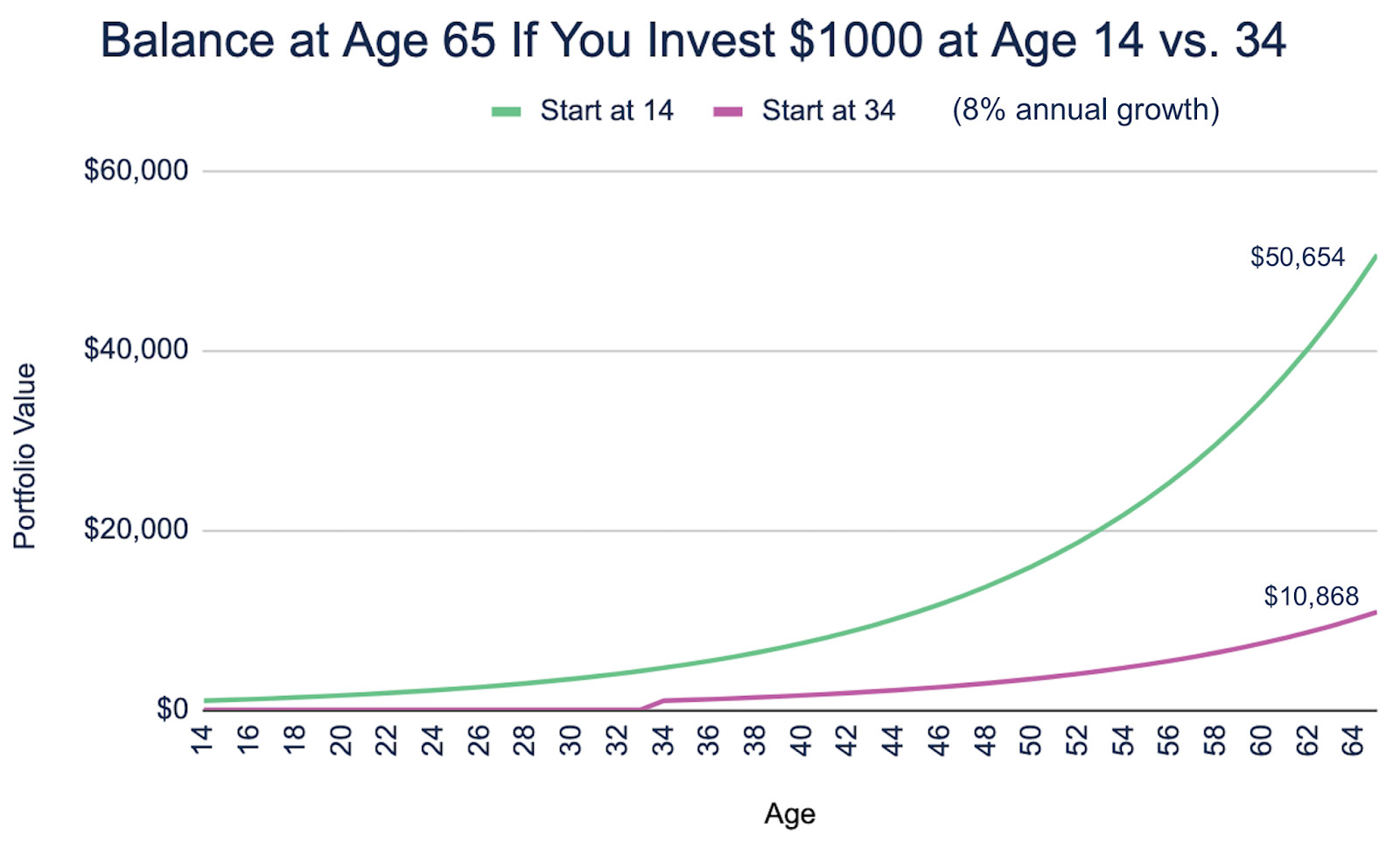

Consider this example: If your 14-year-old child invests $1,000 in a Roth IRA and it grows at an average of 8% per year, by the time they are 65, that initial $1,000 could grow to over $50,000. If they waited until age 34 to invest that same $1,000, it would only grow to around $10,000 by age 65. The 20 extra years of compounding make a monumental difference.

Illustration of the power of compound interest over time, showing the growth of 00 invested at age 14 versus age 34, both reaching age 65.

Illustration of the power of compound interest over time, showing the growth of 00 invested at age 14 versus age 34, both reaching age 65.

Building Financial Literacy from a Young Age

Beyond the impressive dollar amounts, starting a Roth IRA early teaches your child invaluable financial habits. It’s about more than just the money; it’s about instilling a mindset of saving and investing for the future.

By involving your child in this process, you’re showing them firsthand how to participate in the economy and build wealth. Imagine your child growing up with these concepts ingrained:

- Taxes are a part of life: Understanding that taxes are a normal financial consideration.

- Saving is essential: Developing the habit of saving a portion of their earnings.

- Investing for the future: Knowing that their savings can grow through investments like stocks in a Roth IRA.

These early lessons can pave the way for a financially responsible adulthood.

What Kind of “Job” Counts for Roth IRA Contributions?

The good news is your child doesn’t need a formal “job” with a W-2 to contribute to a Roth IRA. Any earned income qualifies, including money from:

- Babysitting

- Lawn mowing

- Pet sitting

- Odd jobs for neighbors or family

- Freelance work

- Self-employment

The crucial element is documenting the income.

If your child has a traditional job with an employer, they will receive paychecks and potentially a W-2 form, making income documentation straightforward. However, for self-employment or gig work, you’ll need to keep records.

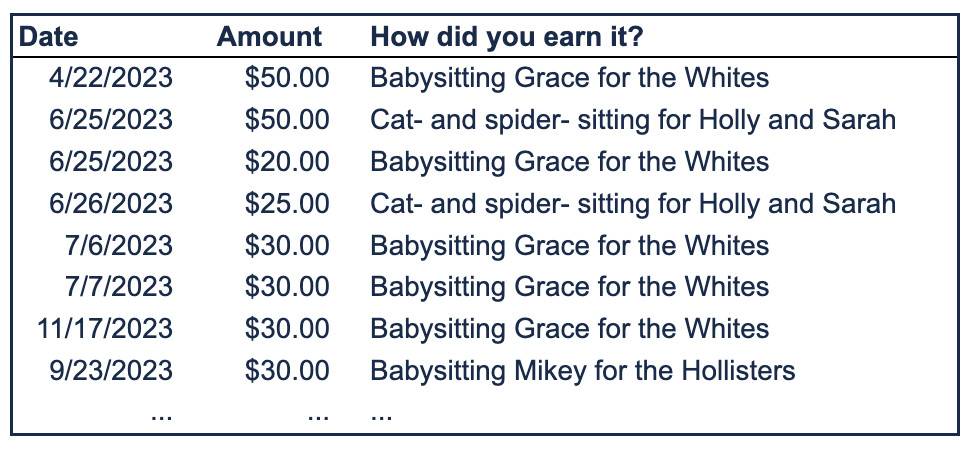

A simple spreadsheet can be very effective for tracking your child’s income. Record the date, amount earned, type of work, and who paid them. This documentation is essential for tax purposes and Roth IRA contributions.

Screenshot of a spreadsheet titled "Alice's Earned Income", showing columns for Date, Amount Earned, Work, and For Whom, used to track a child's income for Roth IRA eligibility.

Screenshot of a spreadsheet titled "Alice's Earned Income", showing columns for Date, Amount Earned, Work, and For Whom, used to track a child's income for Roth IRA eligibility.

Navigating Taxes for Your Child’s Roth IRA

To contribute to a Roth IRA for your child, you’ll likely need to file a tax return for them, even if their income is below the filing threshold. This is because the IRS requires proof of earned income to justify Roth IRA contributions.

While some tax professionals might question the need to file taxes in such cases, it’s generally recommended to err on the side of caution and file a return to properly document your child’s income for IRA purposes.

Tax software like freetaxusa.com can simplify this process, often offering free federal tax return preparation. When filing your child’s taxes, remember a critical step:

Indicate that your child is a dependent on someone else’s return (yours).

Failing to do so can cause complications with your own tax return. If you use a tax professional, be sure to inform them about your plan to open a Roth IRA for your child.

Opening and Funding the Custodial Roth IRA

Since your child is a minor, you’ll need to open a custodial Roth IRA. This is an account held in trust for the child, with you as the custodian managing it until they reach adulthood (typically age 18 or 21, depending on the state and the brokerage).

Reputable brokerage firms like Fidelity or Vanguard are excellent choices for custodial Roth IRAs. Consider factors like customer service and ease of use when selecting a brokerage.

Once the account is open, you can fund it with an amount up to your child’s earned income for the year, but not exceeding the annual Roth IRA contribution limit. For example, if your child earned $1,000, you can contribute up to $1,000 to their Roth IRA.

With your child’s input, you can then invest the money within the Roth IRA. A low-cost, broad market index fund, like VTI (Vanguard Total Stock Market Index Fund), can be a suitable starting investment. (Note: This is not investment advice; consult with a financial advisor for personalized recommendations.)

Boosting Savings with Contribution Matching

To further enhance this financial lesson, consider “matching” your child’s Roth IRA contributions. For instance, you could decide to contribute 50% of their contribution amount. So, if your child contributes $1,000, you contribute an additional $500 (of your own money) to their Roth IRA.

This “match” is a symbolic gesture. It doesn’t increase the contribution limit, but it reinforces the importance of saving and investing and can be a powerful motivator for your child. Grandparents or other family members could also participate in this matching strategy.

By opening a Roth IRA for your child when they earn money, you’re not just saving for their future retirement; you’re equipping them with financial knowledge and habits that will benefit them for a lifetime. It’s a powerful way to teach your children how to Earn With Money and build a secure financial future.

Ready to take control of your family’s financial future? Contact us today for a free consultation to explore personalized financial planning strategies.

Stay informed! Sign up for our twice-monthly newsletter for the latest financial insights and tips.

Disclaimer: This article is for educational purposes only and does not constitute financial, tax, or investment advice. Consult with qualified professionals for advice tailored to your specific situation.