Are you looking for a way to access cash quickly using your Capital One credit card? Understanding how to withdraw money from Capital One credit card is crucial for managing your finances effectively. At money-central.com, we provide you with a comprehensive guide on this process, detailing the steps, fees, and potential impacts on your credit. Unlock financial flexibility and avoid unnecessary costs by learning the ins and outs of Capital One cash advances, including strategies for responsible borrowing, low APR options, and balance transfers to minimize debt.

1. What is a Capital One Credit Card Cash Advance?

A Capital One credit card cash advance allows you to borrow cash against your credit limit. Instead of using your card for purchases, you can withdraw cash from an ATM or bank branch. This can be helpful in situations where you need cash quickly, but it’s important to understand the associated costs.

Understanding the Basics of Cash Advances

According to a study by the New York University’s Stern School of Business, in July 2025, customers should understand how cash advances work to avoid unexpected fees and high-interest charges. Here’s a breakdown:

- Accessibility: You can access cash advances at ATMs or bank branches.

- Fees: Cash advances typically come with a fee, usually a percentage of the amount withdrawn or a flat fee, whichever is greater.

- Interest Rates: Interest rates on cash advances are generally higher than those for regular purchases and begin accruing immediately, without a grace period.

- Credit Limit: The cash advance limit is usually a portion of your overall credit limit.

When to Consider a Cash Advance

Cash advances should be considered a last resort due to the high costs involved. They may be useful in situations such as:

- Emergencies: When you need cash urgently and have no other options.

- Cash-Only Transactions: When you need to pay for something that only accepts cash.

- Limited Access to Funds: When you’re traveling and don’t have access to your bank account.

2. How to Get a Cash Advance with Capital One

Withdrawing cash from your Capital One credit card is a straightforward process, whether you choose to use an ATM or visit a bank branch. Here’s a detailed guide to help you through each method:

Using an ATM

Withdrawing cash from an ATM is a convenient option if you have your PIN and prefer a quick transaction. Here’s how to do it:

- Find an ATM: Locate any ATM that accepts your Capital One card (Visa or Mastercard). While you don’t need to use a Capital One ATM, be aware that out-of-network ATMs may charge additional fees.

- Insert Your Card: Insert your Capital One credit card into the ATM.

- Enter Your PIN: Enter your credit card’s PIN. If you don’t remember your PIN, you may need to request a new one (see instructions below).

- Select “Cash Advance”: On the ATM menu, select the “Cash Advance” option. You may need to select “Credit” first to see this option.

- Enter the Amount: Enter the amount of cash you wish to withdraw, keeping in mind your cash advance limit and any daily withdrawal limits imposed by the ATM.

- Confirm and Withdraw: Confirm the transaction and take your cash. Be sure to also take your card and receipt.

Requesting a PIN Online

If you don’t have your PIN or can’t remember it, you can request a new one through your Capital One online account:

- Log in to Your Account: Go to the Capital One website and log in to your account.

- Select Your Credit Card: Choose the credit card you wish to use for the cash advance.

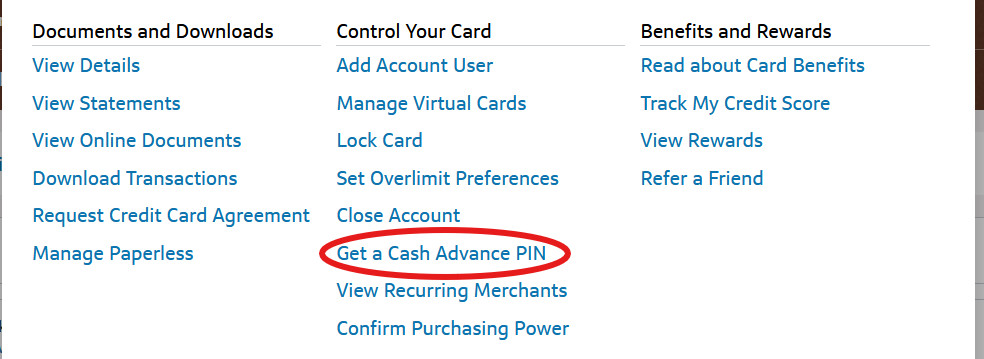

- Navigate to “I Want To…” Menu: Look for the “I Want To…” menu button, typically represented by a gear icon.

- Select “Get a Cash Advance PIN”: Scroll to the “Control Your Card” section and choose “Get a Cash Advance PIN.”

Screenshot of Capital One website with the Get a Cash Advance Pin option selected

Screenshot of Capital One website with the Get a Cash Advance Pin option selected

- Choose Delivery Method: You can choose to receive your PIN by mail or get it immediately using a security code and your phone.

- Follow Instructions: Select “Get a PIN” and follow the remaining instructions to verify your identity and receive your PIN.

Visiting a Bank Branch

If you prefer not to use an ATM or don’t have your PIN, you can visit a bank branch to get a cash advance. Here’s how:

- Find a Participating Bank: Look for a bank branch that displays the Visa or Mastercard logo, indicating they can process cash advances for those card networks.

- Bring Required Documents: Take your Capital One credit card and a government-issued photo ID, such as a driver’s license.

- Speak to a Teller: Approach a bank teller and request a cash advance.

- Provide Your Card and ID: Give the teller your credit card and photo ID. They will verify your identity and process the transaction.

- Receive Your Cash: After the transaction is complete, you will receive your cash from the teller.

Important Considerations

- Cash Advance Limit: Be aware of your cash advance limit, which is usually lower than your overall credit limit. You can find this information on your credit card statement or by logging into your online account.

- Fees: Capital One typically charges a cash advance fee of either $5 or 5% of the transaction amount, whichever is greater.

- Interest Rates: Cash advance interest rates are usually higher than purchase APRs and start accruing immediately, with no grace period.

- ATM Fees: If using an out-of-network ATM, you may incur additional fees from the ATM operator.

Example Scenario

Let’s say you need $200 in cash and decide to get a cash advance from your Capital One credit card at an ATM. Here’s what you might expect:

- Cash Advance Amount: $200

- Cash Advance Fee: $10 (5% of $200)

- Interest Rate: Assuming a 29.74% APR

- Immediate Interest Accrual: Interest begins accruing on the $200 immediately.

If you don’t pay off the $200 plus the $10 fee quickly, the high interest rate will add to the cost.

By understanding these steps and considerations, you can confidently and safely withdraw cash from your Capital One credit card when needed.

3. Fees and Interest Rates on Capital One Cash Advances

Understanding the fees and interest rates associated with Capital One cash advances is essential for making informed financial decisions. These costs can significantly impact the overall expense of borrowing cash against your credit limit.

Cash Advance Fees

Capital One charges a fee for each cash advance transaction. The fee is typically either a flat amount or a percentage of the transaction, whichever is greater. According to Capital One’s terms, the cash advance fee is:

- $5 or 5% of the amount of the cash advance, whichever is greater.

For example, if you withdraw $50, the fee would be $5. However, if you withdraw $500, the fee would be $25 (5% of $500).

Cash Advance APRs

In addition to the upfront fee, cash advances also come with interest rates that are generally higher than those for regular purchases. The Annual Percentage Rate (APR) for cash advances varies depending on the specific Capital One credit card you have. Here are some examples:

| Card Name | Cash Advance APR (Variable) |

|---|---|

| Capital One Platinum Credit Card | 29.74% |

| Capital One Platinum Secured Credit Card | 29.74% |

| Capital One VentureOne Rewards Credit Card | 29.24% |

| Capital One Venture Rewards Credit Card | 29.24% |

| Capital One Venture X Rewards Credit Card | 29.24% |

| Capital One Quicksilver Cash Rewards Credit Card | 29.24% |

| Capital One QuicksilverOne Cash Rewards Credit Card | 29.74% |

| Capital One Quicksilver Secured Cash Rewards Credit Card | 29.74% |

| Capital One Quicksilver Student Cash Rewards Credit Card | 29.24% |

These APRs are variable, meaning they can change based on market conditions and the Prime Rate. Always check your card’s terms and conditions for the most up-to-date information.

No Grace Period

One of the most critical differences between cash advances and regular purchases is the absence of a grace period. With purchases, you typically have a grace period—usually around 21 to 25 days—before interest starts accruing, allowing you to avoid interest charges by paying your balance in full each month. However, cash advances do not have a grace period. Interest begins accruing immediately from the date of the transaction.

How Interest Accrues

Interest on cash advances is calculated daily based on the outstanding balance. The formula for daily interest calculation is:

Daily Interest Rate = (APR / 365) x Outstanding Balance

For example, if you have a cash advance of $500 with an APR of 29.74%, the daily interest would be:

Daily Interest Rate = (0.2974 / 365) x $500 = $0.4074 per day

This means you would accrue approximately $0.41 in interest each day until the balance is paid off.

Impact on Credit Score

While taking out a cash advance itself does not directly impact your credit score, it can indirectly affect it in several ways:

- Credit Utilization Ratio: Cash advances increase your credit utilization ratio, which is the amount of credit you’re using compared to your total available credit. A high credit utilization ratio can negatively impact your credit score. Experts recommend keeping your credit utilization below 30%.

- Payment History: If you’re unable to pay off the cash advance and its associated fees and interest promptly, it can lead to missed payments, which can significantly harm your credit score.

- Debt Burden: Relying on cash advances regularly can indicate financial distress, which lenders may view negatively.

Strategies to Minimize Costs

To minimize the costs associated with Capital One cash advances:

- Pay it Off Quickly: The sooner you pay off the cash advance, the less interest you’ll accrue.

- Prioritize Repayment: Focus on paying off the cash advance before making new purchases on your credit card.

- Consider Alternatives: Explore other options like personal loans, balance transfers, or lines of credit, which may offer lower interest rates and fees.

- Budgeting: Create a budget to manage your finances and avoid the need for cash advances.

- Emergency Fund: Build an emergency fund to cover unexpected expenses, reducing your reliance on credit cards for cash needs.

Example Scenario

Let’s illustrate the potential costs with an example. Suppose you take out a cash advance of $1,000 on a Capital One credit card with a 29.74% APR and a 5% cash advance fee.

- Cash Advance Amount: $1,000

- Cash Advance Fee: $50 (5% of $1,000)

- Total Initial Balance: $1,050

If you only make the minimum payment each month, it could take years to pay off the balance, and you’ll accrue significant interest charges. For instance, if the minimum payment is $25, a significant portion of that payment will go toward interest rather than the principal.

By understanding the fees, interest rates, and potential impact on your credit score, you can make an informed decision about whether a Capital One cash advance is the right choice for your financial situation.

4. Alternatives to Capital One Cash Advances

While Capital One cash advances can provide quick access to funds, they often come with high fees and interest rates. Exploring alternative options can help you find more cost-effective ways to manage your financial needs. Here are several alternatives to consider:

Personal Loans

Personal loans are unsecured loans that can be used for various purposes, including covering emergency expenses. They typically offer lower interest rates compared to credit card cash advances.

- Lower Interest Rates: Personal loans generally have fixed interest rates that are lower than cash advance APRs. According to research from New York University’s Stern School of Business, personal loan rates typically range from 6% to 36%, depending on your credit score and the lender.

- Fixed Repayment Schedule: Personal loans come with a fixed repayment schedule, making it easier to budget and manage your payments.

- Larger Loan Amounts: You can borrow larger amounts with personal loans compared to cash advances.

How to Apply:

- Check Your Credit Score: Review your credit score to get an idea of the interest rates you might qualify for.

- Shop Around: Compare offers from different lenders, including banks, credit unions, and online lenders.

- Gather Documents: Prepare necessary documents such as proof of income, identification, and bank statements.

- Apply for the Loan: Complete the application process with your chosen lender.

Balance Transfers

If you have other credit cards with available credit, you can transfer the balance from your Capital One card to a card with a lower APR or a promotional 0% APR period.

- Lower APR: Transferring your balance to a card with a lower APR can save you money on interest charges.

- Promotional Periods: Some balance transfer cards offer 0% APR for a limited time, allowing you to pay down your balance without accruing interest.

- Consolidation: Balance transfers can help you consolidate your debt into a single, more manageable payment.

How to Perform a Balance Transfer:

- Find a Balance Transfer Card: Look for credit cards offering balance transfer promotions with low or 0% APR.

- Apply for the Card: Apply for the balance transfer card and get approved.

- Request the Transfer: Follow the card issuer’s instructions to transfer the balance from your Capital One card.

- Pay Attention to Fees: Be aware of balance transfer fees, which are typically a percentage of the transferred amount.

Lines of Credit

A line of credit is a flexible loan that allows you to borrow money up to a certain limit. You only pay interest on the amount you borrow.

- Flexibility: Lines of credit offer flexibility as you can borrow and repay funds as needed.

- Lower Interest Rates: Interest rates on lines of credit are usually lower than cash advance APRs.

- Emergency Funds: They can serve as a backup source of funds for emergencies.

How to Obtain a Line of Credit:

- Check Your Credit Score: Ensure you have a good credit score to qualify for better terms.

- Compare Offers: Shop around for lines of credit from banks and credit unions.

- Apply for the Line of Credit: Submit your application and provide the required documentation.

- Understand the Terms: Review the interest rates, fees, and repayment terms.

0% APR Credit Cards

Opening a new credit card with a 0% APR introductory period on purchases can be a good alternative if you need to make new purchases and pay them off over time without accruing interest.

- Interest-Free Purchases: You can make purchases without incurring interest charges during the promotional period.

- Budgeting: This allows you to budget and pay off the balance within the promotional period.

- Credit Score Boost: Responsible use of a 0% APR card can help improve your credit score.

How to Use a 0% APR Card Effectively:

- Find a 0% APR Card: Look for credit cards offering 0% APR on purchases for an extended period.

- Apply for the Card: Apply for the card and get approved.

- Make Purchases: Use the card for necessary purchases, keeping track of your spending.

- Pay Off the Balance: Make sure to pay off the balance before the promotional period ends to avoid accruing interest.

Savings and Emergency Funds

Using your savings or emergency fund is often the most cost-effective way to cover unexpected expenses.

- No Interest or Fees: You don’t have to pay interest or fees when using your own savings.

- Financial Security: Having an emergency fund provides financial security and reduces reliance on credit.

- Peace of Mind: Knowing you have funds available can reduce stress during financial emergencies.

How to Build an Emergency Fund:

- Set a Goal: Determine how much you want to save in your emergency fund (e.g., 3-6 months of living expenses).

- Budget: Create a budget to track your income and expenses.

- Automate Savings: Set up automatic transfers from your checking account to your savings account.

- Start Small: Begin with small, manageable amounts and gradually increase your savings over time.

Other Alternatives

- Payday Loans: Payday loans are short-term, high-interest loans that should be avoided due to their exorbitant costs.

- Title Loans: Title loans require you to use your vehicle as collateral and can lead to repossession if you can’t repay the loan.

- Pawn Shop Loans: Pawn shop loans involve pawning items for cash and can result in losing your valuables if you can’t redeem them.

By considering these alternatives, you can find more affordable and manageable ways to address your financial needs without resorting to high-cost cash advances.

5. Tips for Managing Your Capital One Credit Card Responsibly

Managing your Capital One credit card responsibly is crucial for maintaining a healthy financial life. Here are some practical tips to help you use your credit card effectively and avoid common pitfalls.

Understand Your Credit Limit and Available Credit

- Know Your Limit: Be fully aware of your credit limit, which is the maximum amount you can charge on your card.

- Monitor Available Credit: Regularly check your available credit to avoid exceeding your limit, which can lead to over-limit fees and a negative impact on your credit score.

- Credit Utilization Ratio: Keep your credit utilization ratio below 30%. This means using no more than 30% of your available credit. For example, if your credit limit is $10,000, try to keep your balance below $3,000.

Pay Your Bills on Time

- Payment Due Date: Always pay at least the minimum amount due by the payment due date to avoid late fees and negative marks on your credit report.

- Set Reminders: Set up payment reminders through your bank or credit card account to ensure you don’t miss a payment.

- Automatic Payments: Enroll in automatic payments to have the minimum payment or the full balance automatically deducted from your bank account each month.

Pay More Than the Minimum

- Minimize Interest: Paying more than the minimum amount due can significantly reduce the amount of interest you pay and help you pay off your balance faster.

- Snowball or Avalanche Method: Consider using the debt snowball or debt avalanche method to prioritize paying off your credit card debt. The snowball method focuses on paying off the smallest balances first, while the avalanche method focuses on the highest interest rates.

Review Your Credit Card Statements Regularly

- Check for Errors: Review your credit card statements each month to identify any unauthorized charges or billing errors.

- Track Spending: Monitor your spending habits to ensure you’re staying within your budget.

- Report Discrepancies: Report any discrepancies or unauthorized charges to Capital One immediately.

Avoid Cash Advances

- High Costs: Cash advances come with high fees and interest rates, making them an expensive way to borrow money.

- No Grace Period: Interest accrues immediately on cash advances, with no grace period.

- Alternatives: Explore alternative options such as personal loans, balance transfers, or lines of credit, which may offer lower interest rates and fees.

Use Credit Monitoring Tools

- Capital One CreditWise: Use Capital One’s CreditWise tool to monitor your credit score and track your credit report for any changes or potential fraud.

- Third-Party Services: Consider using third-party credit monitoring services to receive alerts about changes to your credit report and potential identity theft.

Create a Budget and Stick to It

- Track Income and Expenses: Create a budget to track your income and expenses, ensuring you’re not overspending.

- Prioritize Needs vs. Wants: Distinguish between needs and wants to make informed spending decisions.

- Use Budgeting Apps: Utilize budgeting apps or software to help you track your spending and stay within your budget.

Avoid Maxing Out Your Credit Card

- High Credit Utilization: Maxing out your credit card can negatively impact your credit score and make it difficult to pay off your balance.

- Financial Stress: It can also lead to financial stress and difficulty managing your debt.

- Responsible Spending: Practice responsible spending habits to avoid maxing out your credit card.

Be Cautious with Credit Card Offers

- Read the Fine Print: Carefully review the terms and conditions of any credit card offers before applying, paying attention to interest rates, fees, and rewards programs.

- Avoid Unnecessary Cards: Avoid opening multiple credit cards that you don’t need, as this can lead to overspending and difficulty managing your debt.

Stay Informed About Credit Card Policies

- Capital One Website: Stay informed about Capital One’s credit card policies, including changes to interest rates, fees, and rewards programs.

- Customer Service: Contact Capital One’s customer service if you have any questions or concerns about your credit card account.

By following these tips, you can manage your Capital One credit card responsibly, maintain a healthy credit score, and avoid unnecessary debt.

6. Capital One Credit Cards That Offer Cash Advances

Most Capital One credit cards offer cash advances, providing cardholders with access to cash when needed. Here’s a breakdown of some popular Capital One cards that permit cash advances, along with their associated fees and APRs.

Capital One Platinum Credit Card

- Cash Advance Offered: Yes

- Cash Advance Fee: $5 or 5% of the amount of the cash advance, whichever is greater

- Cash Advance APR (Variable): 29.74%

The Capital One Platinum Credit Card is designed for individuals looking to build or rebuild their credit. It offers cash advance options, but it’s essential to be aware of the high APR.

Capital One Platinum Secured Credit Card

- Cash Advance Offered: Yes

- Cash Advance Fee: $5 or 5% of the amount of the cash advance, whichever is greater

- Cash Advance APR (Variable): 29.74%

The Capital One Platinum Secured Credit Card is a secured card that requires a security deposit. It also allows cash advances, but like the Platinum card, it comes with a high APR.

Capital One VentureOne Rewards Credit Card

- Cash Advance Offered: Yes

- Cash Advance Fee: $5 or 5% of the amount of the cash advance, whichever is greater

- Cash Advance APR (Variable): 29.24%

The Capital One VentureOne Rewards Credit Card is a travel rewards card that earns miles on every purchase. It offers cash advances, but the APR is relatively high, so it’s best to use them sparingly.

Capital One Venture Rewards Credit Card

- Cash Advance Offered: Yes

- Cash Advance Fee: $5 or 5% of the amount of the cash advance, whichever is greater

- Cash Advance APR (Variable): 29.24%

The Capital One Venture Rewards Credit Card offers more travel rewards than the VentureOne card. It also permits cash advances with the same fee structure and APR.

Capital One Venture X Rewards Credit Card

- Cash Advance Offered: Yes

- Cash Advance Fee: $5 or 5% of the amount of the cash advance, whichever is greater

- Cash Advance APR (Variable): 29.24%

The Capital One Venture X Rewards Credit Card is a premium travel card with enhanced rewards and benefits. It includes cash advance options with a similar APR.

Capital One Quicksilver Cash Rewards Credit Card

- Cash Advance Offered: Yes

- Cash Advance Fee: $5 or 5% of the amount of the cash advance, whichever is greater

- Cash Advance APR (Variable): 29.24%

The Capital One Quicksilver Cash Rewards Credit Card earns cash back on every purchase. It also allows cash advances, but the high APR makes it a costly option.

Capital One QuicksilverOne Cash Rewards Credit Card

- Cash Advance Offered: Yes

- Cash Advance Fee: $5 or 5% of the amount of the cash advance, whichever is greater

- Cash Advance APR (Variable): 29.74%

The Capital One QuicksilverOne Cash Rewards Credit Card is designed for individuals with fair credit. It offers cash advances with a higher APR compared to the standard Quicksilver card.

Capital One Quicksilver Secured Cash Rewards Credit Card

- Cash Advance Offered: Yes

- Cash Advance Fee: $5 or 5% of the amount of the cash advance, whichever is greater

- Cash Advance APR (Variable): 29.74%

The Capital One Quicksilver Secured Cash Rewards Credit Card is a secured card that earns cash back rewards. It also permits cash advances with the same high APR.

Capital One Quicksilver Student Cash Rewards Credit Card

- Cash Advance Offered: Yes

- Cash Advance Fee: $5 or 5% of the amount of the cash advance, whichever is greater

- Cash Advance APR (Variable): 29.24%

The Capital One Quicksilver Student Cash Rewards Credit Card is designed for students and offers cash back rewards. It includes cash advance options with a typical APR.

Capital One Savor Cash Rewards Credit Card

- Cash Advance Offered: Yes

- Cash Advance Fee: $5 or 5% of the amount of the cash advance, whichever is greater

- Cash Advance APR (Variable): 29.24%

The Capital One Savor Cash Rewards Credit Card earns cash back on dining and entertainment purchases. It also allows cash advances, but the high APR makes it less appealing.

Capital One SavorOne Cash Rewards Credit Card

- Cash Advance Offered: Yes

- Cash Advance Fee: $5 or 5% of the amount of the cash advance, whichever is greater

- Cash Advance APR (Variable): 29.24%

The Capital One SavorOne Cash Rewards Credit Card is a variation of the Savor card with slightly different rewards. It includes cash advance options with a similar APR.

Capital One Spark Cash Plus

- Cash Advance Offered: Yes

- Cash Advance Fee: $5 or 5% of the amount of the cash advance, whichever is greater

- Cash Advance APR (Variable): N/A (this is a charge card)

The Capital One Spark Cash Plus is a business charge card that offers cash back rewards. It also allows cash advances.

Capital One Spark Miles for Business

- Cash Advance Offered: Yes

- Cash Advance Fee: $5 or 5% of the amount of the cash advance, whichever is greater

- Cash Advance APR (Variable): 31.24%

The Capital One Spark Miles for Business earns miles on business purchases. It permits cash advances with a very high APR.

Summary Table

| Card Name | Cash Advance Offered? | Cash Advance Fee | Cash Advance APR (Variable) |

|---|---|---|---|

| Capital One Platinum Credit Card | Yes | $5 or 5%, whichever is greater | 29.74% |

| Capital One Platinum Secured Credit Card | Yes | $5 or 5%, whichever is greater | 29.74% |

| Capital One VentureOne Rewards Credit Card | Yes | $5 or 5%, whichever is greater | 29.24% |

| Capital One Venture Rewards Credit Card | Yes | $5 or 5%, whichever is greater | 29.24% |

| Capital One Venture X Rewards Credit Card | Yes | $5 or 5%, whichever is greater | 29.24% |

| Capital One Quicksilver Cash Rewards Credit Card | Yes | $5 or 5%, whichever is greater | 29.24% |

| Capital One QuicksilverOne Cash Rewards Credit Card | Yes | $5 or 5%, whichever is greater | 29.74% |

| Capital One Quicksilver Secured Cash Rewards Credit Card | Yes | $5 or 5%, whichever is greater | 29.74% |

| Capital One Quicksilver Student Cash Rewards Credit Card | Yes | $5 or 5%, whichever is greater | 29.24% |

| Capital One Savor Cash Rewards Credit Card | Yes | $5 or 5%, whichever is greater | 29.24% |

| Capital One SavorOne Cash Rewards Credit Card | Yes | $5 or 5%, whichever is greater | 29.24% |

| Capital One Spark Cash Plus | Yes | $5 or 5%, whichever is greater | N/A (charge card) |

| Capital One Spark Miles for Business | Yes | $5 or 5%, whichever is greater | 31.24% |

Key Considerations

- High APRs: Be aware that cash advances on Capital One credit cards typically come with high APRs, which can make them an expensive way to borrow money.

- Fees: In addition to high APRs, there are also cash advance fees to consider.

- Alternatives: Before taking out a cash advance, explore alternative options such as personal loans or balance transfers, which may offer lower interest rates and fees.

7. Impact of Cash Advances on Your Credit Score

Taking a cash advance on your Capital One credit card can have several implications for your credit score. While the act of taking a cash advance itself doesn’t directly lower your score, the associated behaviors and financial impacts can affect your creditworthiness. Here’s a detailed look at how cash advances can impact your credit score:

Increased Credit Utilization

- Definition: Credit utilization is the amount of credit you’re using compared to your total available credit. It’s a significant factor in determining your credit score.

- Impact: Cash advances increase your credit utilization ratio. For example, if you have a credit limit of $10,000 and you take a $3,000 cash advance, your credit utilization becomes 30%.

- Recommendations: Experts recommend keeping your credit utilization below 30%. Exceeding this threshold can negatively impact your credit score. According to a study from New York University’s Stern School of Business, individuals with credit utilization ratios above 30% are more likely to see a decrease in their credit scores.

- Example:

- Credit Limit: $10,000

- Cash Advance: $3,000

- Credit Utilization: 30%

High Interest Rates and Debt Burden

- APR: Cash advances typically come with higher APRs than regular purchases. This means you’ll accrue interest charges more quickly.

- Debt Burden: If you’re unable to pay off the cash advance and its associated fees and interest promptly, it can lead to a higher debt burden.

- Impact: A high debt burden can make it difficult to manage your finances and can negatively impact your credit score. Lenders view individuals with high debt burdens as riskier borrowers.

- Recommendations: Prioritize paying off the cash advance as quickly as possible to minimize interest charges and reduce your debt burden.

- Example: If you have a $3,000 cash advance with a 29.74% APR, the interest charges can quickly add up if you only make the minimum payments.

Payment History

- Importance: Payment history is the most important factor in determining your credit score.

- Impact: If you’re unable to pay off the cash advance and its associated fees and interest on time, it can lead to missed payments.

- Consequences: Missed payments can significantly harm your credit score and stay on your credit report for up to seven years.

- Recommendations: Set up automatic payments or payment reminders to ensure you never miss a payment.

- Example: A single missed payment can lower your credit score by dozens of points, especially if you have a thin credit file.

Credit Mix

- Diversity: Having a mix of different types of credit accounts (e.g., credit cards, loans) can positively impact your credit score.

- Impact: While taking a cash advance doesn’t directly diversify your credit mix, it can indirectly affect it if you’re relying on cash advances instead of other types of credit.

- Recommendations: Focus on building a diverse credit mix by responsibly managing different types of credit accounts.

- Example: Having a mix of credit cards, a mortgage, and a car loan can demonstrate to lenders that you’re capable of managing different types of credit.

New Credit

- Opening New Accounts: Opening multiple new credit accounts in a short period can lower your credit score, especially if you have a short credit history.

- Impact: While taking a cash advance doesn’t involve opening a new account, it can indirectly affect your credit score if you’re opening new credit cards to transfer the balance from the cash advance.

- Recommendations: Avoid opening multiple new credit cards in a short period.

- Example: Opening several new credit cards within a few months can lower your credit score by making you appear to be a riskier borrower.

Public Records and Collections

- Severe Financial Distress: If you’re unable to pay off the cash advance and it goes into collections, it can lead to negative marks on your credit report.

- Impact: Collections accounts and public records such as bankruptcies can severely damage your credit score.

- Recommendations: Take steps to manage your debt and avoid collections or legal judgments.

- Example: A collections account or bankruptcy can lower your credit score by hundreds of points and stay on your credit report for up to seven years.

Strategies to Minimize Negative Impact

- Pay Off Quickly: Pay off the cash advance as quickly as possible to minimize interest charges and reduce your debt burden.

- Prioritize Repayment: Focus on paying off the cash advance before making new purchases on your credit card.

- Create a Budget: Create a budget to manage your finances and avoid the need for cash advances.

- Consider Alternatives: Explore alternative options such as personal loans, balance transfers, or lines of credit, which may offer lower interest rates and fees.

Example Scenario

Let’s say you take a $1,000 cash advance on your Capital One credit card. Here’s how it could impact your credit score:

- Initial Impact: Your credit utilization increases, which could slightly lower your score if it exceeds 30%.

- Short-Term Impact: If you pay off the cash advance within a month, the impact on your credit score will likely be minimal.

- Long-Term Impact: If you carry the balance for several months and only make minimum payments, the high interest charges and increased debt burden could negatively impact your credit score.

By understanding how cash advances can impact your credit score, you can take steps to manage your credit card responsibly and maintain a healthy credit profile.