The time value of money, a fundamental concept in finance, dictates that money available today is worth more than the same amount in the future due to its potential earning capacity. At money-central.com, we’ll break down how to calculate TVM, empowering you to make informed financial decisions. Understanding these financial concepts is crucial for effective money management, investment strategies, and financial planning.

1. What is the Time Value of Money (TVM)?

The time value of money (TVM) is the concept that money you have now is worth more than the identical sum in the future due to its potential to earn. This core principle highlights the advantage of having money sooner rather than later. Money-central.com is dedicated to providing accessible explanations and tools to help you grasp this essential idea. The TVM concept is vital in financial planning, investment decisions, and understanding interest rates.

The time value of money (TVM) stems from two primary factors:

- Opportunity Cost: Money in hand today can be invested to generate returns, leading to a higher value in the future. This potential gain is the opportunity cost of waiting for future money.

- Inflation and Risk: The purchasing power of money erodes over time due to inflation. Additionally, future payments carry a risk of not being received due to unforeseen circumstances.

Because of these factors, money received today is more valuable than the same amount promised in the future. This forms the basis of financial decision-making, enabling you to compare options and choose the most beneficial one. Learning about the time value of money is crucial for anyone looking to enhance their financial literacy, manage their investments wisely, and plan for long-term financial security.

2. Why is the Time Value of Money Important?

The time value of money is important because it is the foundation of many financial decisions, including investment analysis, capital budgeting, and retirement planning. By understanding TVM, individuals and businesses can make informed choices about when to spend, save, and invest money. Money-central.com offers the resources needed to master this vital financial concept. The role of TVM is significant in assessing investments, understanding loan terms, and planning for long-term financial goals.

Here’s a closer look at why TVM is so important:

- Investment Decisions: TVM helps investors evaluate the potential profitability of different investment opportunities. By discounting future cash flows to their present value, investors can compare investments with varying payout schedules and choose the ones that offer the highest returns relative to their risk.

- Capital Budgeting: Businesses use TVM to decide whether to invest in new projects or assets. By calculating the net present value (NPV) of a project’s expected cash flows, companies can determine if the project is likely to be profitable and create value for shareholders.

- Loan Analysis: TVM is essential for understanding the true cost of borrowing money. By calculating the present value of future loan payments, borrowers can compare different loan offers and choose the one that best fits their needs and budget.

- Retirement Planning: TVM plays a crucial role in retirement planning. By projecting future savings and investment returns, individuals can estimate how much money they will need to save to achieve their retirement goals. TVM also helps retirees make informed decisions about how to withdraw their savings over time.

Understanding the time value of money empowers you to make sound financial decisions that can significantly impact your long-term financial well-being. Whether you’re saving for retirement, evaluating investment opportunities, or simply trying to manage your finances more effectively, TVM is an indispensable tool.

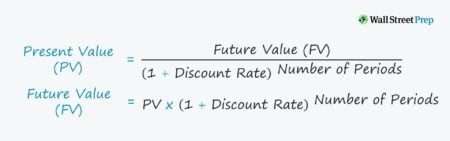

3. What is the Formula for Calculating the Time Value of Money?

The time value of money can be calculated using formulas for present value (PV) and future value (FV), considering factors like interest rate, compounding periods, and time. Here at money-central.com, we provide easy-to-use calculators and detailed explanations to help you apply these formulas effectively. The formulas are fundamental in financial analysis, investment planning, and understanding the impact of interest and inflation on your money.

The basic formulas are as follows:

-

Present Value (PV): This formula calculates the current worth of a future sum of money, discounted by an appropriate interest rate.

PV = FV / (1 + r)^nWhere:

- PV = Present Value

- FV = Future Value

- r = Discount Rate (interest rate)

- n = Number of periods (years)

-

Future Value (FV): This formula calculates the value of an asset at a specified date in the future based on an assumed rate of growth.

FV = PV * (1 + r)^nWhere:

- FV = Future Value

- PV = Present Value

- r = Interest Rate

- n = Number of periods (years)

These formulas can be adapted for different compounding frequencies (e.g., monthly, quarterly, annually). For example, if interest is compounded more than once a year, the formulas become:

PV = FV / (1 + r/k)^(n*k)FV = PV * (1 + r/k)^(n*k)

Where:

- k = Number of compounding periods per year

Understanding and using these formulas allows you to accurately assess the value of money across time, make informed financial decisions, and effectively plan for your future.

4. How Do You Calculate Present Value?

To calculate present value, you need to discount a future sum of money back to its current worth, considering the interest rate and the time period. Money-central.com offers user-friendly present value calculators and tutorials to simplify this process. The present value calculation is essential for investment analysis, comparing financial options, and determining the current value of future cash flows.

Here’s a step-by-step explanation:

-

Identify the Future Value (FV): Determine the amount of money you will receive in the future.

-

Determine the Discount Rate (r): Choose an appropriate discount rate, which represents the rate of return you could earn on an investment with similar risk. This rate accounts for the opportunity cost of money.

-

Determine the Number of Periods (n): Identify the number of periods (usually years) between the present and the date when you will receive the future value.

-

Apply the Present Value Formula: Use the formula:

PV = FV / (1 + r)^n- PV = Present Value

- FV = Future Value

- r = Discount Rate

- n = Number of periods

Example:

Suppose you are promised to receive $1,000 in 5 years, and the appropriate discount rate is 8%. To calculate the present value:

-

FV = $1,000

-

r = 8% or 0.08

-

n = 5 years

PV = $1,000 / (1 + 0.08)^5

PV = $1,000 / (1.08)^5

PV = $1,000 / 1.4693

PV ≈ $680.58

Therefore, the present value of receiving $1,000 in 5 years, with an 8% discount rate, is approximately $680.58. This means that $680.58 today is equivalent to receiving $1,000 in 5 years, considering the time value of money.

5. How Do You Calculate Future Value?

Future value is calculated by projecting the growth of a present sum of money into the future, based on a specified interest rate and time period. At money-central.com, we provide intuitive future value calculators and educational resources to help you understand and apply this concept effectively. This calculation is crucial for financial planning, retirement savings projections, and understanding the potential growth of investments.

Here’s a detailed breakdown:

-

Identify the Present Value (PV): Determine the amount of money you have today.

-

Determine the Interest Rate (r): Choose an appropriate interest rate, which represents the rate of return you expect to earn on your investment.

-

Determine the Number of Periods (n): Identify the number of periods (usually years) over which the money will grow.

-

Apply the Future Value Formula: Use the formula:

FV = PV * (1 + r)^n- FV = Future Value

- PV = Present Value

- r = Interest Rate

- n = Number of periods

Example:

Suppose you invest $500 today in an account that earns an annual interest rate of 6%, and you want to know how much it will be worth in 10 years.

-

PV = $500

-

r = 6% or 0.06

-

n = 10 years

FV = $500 * (1 + 0.06)^10

FV = $500 * (1.06)^10

FV = $500 * 1.7908

FV ≈ $895.42

Therefore, the future value of your $500 investment after 10 years, with a 6% annual interest rate, is approximately $895.42. This calculation helps you understand the potential growth of your investment over time, making it a crucial tool for financial planning and investment decisions.

6. What is a Discount Rate and How Does It Affect TVM?

A discount rate is the interest rate used to determine the present value of future cash flows; a higher discount rate reduces the present value, reflecting increased risk or opportunity cost. Money-central.com offers detailed explanations of discount rates and their impact on financial decisions. The discount rate is critical in investment analysis, capital budgeting, and evaluating the profitability of future projects.

Here’s a more detailed explanation:

- Definition of Discount Rate: The discount rate is the rate of return required by an investor to compensate for the time value of money and the risk associated with receiving future cash flows. It represents the opportunity cost of investing in a particular project or asset compared to other available investments.

- Factors Influencing the Discount Rate:

- Risk: Higher risk investments require higher discount rates to compensate for the increased uncertainty of receiving future cash flows.

- Opportunity Cost: The return that could be earned on alternative investments influences the discount rate. If other investments offer higher returns, investors will demand a higher discount rate for the investment being evaluated.

- Inflation: Expected inflation rates can also affect the discount rate. Investors typically demand a higher discount rate to compensate for the erosion of purchasing power due to inflation.

- Impact on TVM Calculations:

- Present Value: The discount rate is inversely related to the present value of future cash flows. A higher discount rate results in a lower present value, as future cash flows are discounted more heavily to reflect the increased risk or opportunity cost.

- Investment Decisions: When evaluating investment opportunities, a higher discount rate makes it more difficult for a project to achieve a positive net present value (NPV), as the present value of future cash flows is reduced. This means that projects with higher risk or longer payback periods may be less attractive when using a higher discount rate.

Example:

Consider two investment opportunities:

- Investment A: Expected to generate $1,000 in 5 years with a discount rate of 8%.

- Investment B: Expected to generate $1,000 in 5 years with a discount rate of 12%.

Using the present value formula:

PV of Investment A = $1,000 / (1 + 0.08)^5 ≈ $680.58PV of Investment B = $1,000 / (1 + 0.12)^5 ≈ $567.43

As shown, the higher discount rate in Investment B results in a lower present value, making Investment A more attractive if all other factors are equal.

7. What are the Applications of the Time Value of Money?

The time value of money has wide-ranging applications in financial planning, investment analysis, loan evaluations, and business decisions. Money-central.com provides tools and resources to help you apply TVM principles in various real-world scenarios. These applications are essential for making informed financial decisions and achieving long-term financial goals.

Here are some key applications:

- Investment Analysis: TVM is used to evaluate the profitability and attractiveness of investment opportunities by calculating the present value of future cash flows.

- Capital Budgeting: Businesses use TVM to decide whether to invest in new projects or assets by calculating the net present value (NPV) of expected cash flows.

- Loan Evaluations: TVM is essential for understanding the true cost of borrowing money and comparing different loan offers by calculating the present value of future loan payments.

- Retirement Planning: TVM plays a crucial role in projecting future savings and investment returns, helping individuals estimate how much money they need to save to achieve their retirement goals.

- Insurance Decisions: TVM is used to evaluate the costs and benefits of insurance policies by comparing the present value of premiums paid to the expected future payouts.

- Real Estate Investments: TVM is applied to analyze the potential returns from real estate investments by calculating the present value of rental income and future property appreciation.

Examples:

- Deciding between two job offers: One offer pays a higher salary now, while the other offers better long-term benefits. TVM can help you determine which offer is more financially advantageous by calculating the present value of all future income and benefits.

- Evaluating a home mortgage: TVM can help you understand the total cost of a mortgage, including interest payments, and compare different loan options to find the one that best fits your budget and financial goals.

- Planning for college savings: TVM can help you estimate how much you need to save each year to reach your college savings goal, taking into account the time value of money and expected investment returns.

- Assessing a business expansion: A company can use TVM to determine if expanding into a new market will be profitable by forecasting future revenues and expenses and discounting them back to their present value.

By mastering the applications of the time value of money, you can make more informed financial decisions that align with your goals and priorities, whether you’re an individual, a business owner, or an investor.

8. How Does Inflation Affect the Time Value of Money?

Inflation erodes the purchasing power of money over time, reducing the real value of future cash flows and impacting TVM calculations by necessitating higher discount rates. At money-central.com, we help you understand how to account for inflation in your financial planning and investment decisions. Understanding the impact of inflation is essential for accurate financial analysis and long-term financial health.

Here’s a more detailed explanation:

-

Inflation’s Impact on Purchasing Power: Inflation is the rate at which the general level of prices for goods and services is rising, and subsequently, purchasing power is falling. This means that a dollar today can buy more goods and services than a dollar in the future.

-

Inflation and Discount Rates: To account for inflation in TVM calculations, it’s important to use a discount rate that reflects the expected rate of inflation. The real discount rate can be calculated as:

Real Discount Rate = Nominal Discount Rate - Inflation RateThe nominal discount rate is the stated interest rate, while the real discount rate is the rate adjusted for inflation.

-

Impact on Investment Decisions: When evaluating investment opportunities, it’s crucial to consider the impact of inflation on future cash flows. If inflation is expected to be high, the future cash flows will be worth less in real terms, and a higher discount rate should be used to reflect this.

-

Impact on Retirement Planning: Inflation can significantly impact retirement planning, as it erodes the purchasing power of savings over time. To ensure that your retirement savings will be sufficient to cover your expenses, it’s important to factor in expected inflation rates and adjust your savings goals accordingly.

Example:

Suppose you are evaluating an investment that is expected to generate $1,000 in 5 years. The nominal discount rate is 10%, and the expected inflation rate is 3%.

Real Discount Rate = 10% - 3% = 7%

Using the real discount rate to calculate the present value:

PV = $1,000 / (1 + 0.07)^5 ≈ $712.99

If you used the nominal discount rate:

PV = $1,000 / (1 + 0.10)^5 ≈ $620.92

As shown, using the real discount rate provides a more accurate assessment of the present value of future cash flows, taking into account the impact of inflation.

9. What is Compounding and How Does It Affect TVM?

Compounding refers to earning returns on both the principal and accumulated interest, significantly enhancing the growth of investments over time and impacting future value calculations. Money-central.com offers resources and calculators to illustrate the power of compounding and its effects on long-term financial growth. Understanding compounding is vital for maximizing investment returns and achieving financial goals.

Here’s a more detailed explanation:

-

Definition of Compounding: Compounding is the process of earning returns on both the initial principal and the accumulated interest from previous periods. This means that your money grows exponentially over time, as you earn interest on your interest.

-

Frequency of Compounding: The frequency of compounding can have a significant impact on the future value of an investment. The more frequently interest is compounded, the faster your money will grow. For example, daily compounding will result in a higher future value than annual compounding, assuming the same interest rate.

-

Compounding Formula: The formula for calculating future value with compounding is:

FV = PV * (1 + r/n)^(n*t)Where:

- FV = Future Value

- PV = Present Value

- r = Annual Interest Rate

- n = Number of Compounding Periods per Year

- t = Number of Years

-

Impact on Investment Growth: Compounding can significantly enhance the growth of investments over time, especially over long periods. Even small differences in interest rates or compounding frequency can result in substantial differences in future value.

Example:

Suppose you invest $1,000 in an account that earns an annual interest rate of 8%, compounded annually. After 10 years, the future value of your investment would be:

FV = $1,000 * (1 + 0.08/1)^(1*10) ≈ $2,158.92

If the interest were compounded quarterly, the future value would be:

FV = $1,000 * (1 + 0.08/4)^(4*10) ≈ $2,208.04

As shown, more frequent compounding results in a higher future value, highlighting the power of compounding over time.

10. How Can I Use TVM to Make Better Financial Decisions?

You can use TVM to make informed financial decisions by evaluating investment opportunities, comparing loan options, and planning for long-term goals, ensuring that you maximize the value of your money over time. Money-central.com provides the tools and knowledge you need to apply TVM principles to your personal finances and investments. The applications of TVM are crucial for financial planning, investment decisions, and achieving long-term financial security.

Here’s a detailed guide on how to use TVM in different financial scenarios:

- Evaluating Investment Opportunities:

- Calculate the present value of expected future cash flows from an investment.

- Compare the present value of different investment opportunities to determine which offers the highest return relative to the risk.

- Consider the impact of inflation and taxes on investment returns.

- Comparing Loan Options:

- Calculate the present value of future loan payments for different loan options.

- Compare the total cost of borrowing money under different loan terms.

- Choose the loan option that best fits your needs and budget.

- Planning for Retirement:

- Estimate how much money you need to save to achieve your retirement goals.

- Project future savings and investment returns using TVM calculations.

- Adjust your savings goals as needed to account for inflation and changes in your financial situation.

- Making Purchasing Decisions:

- Evaluate the long-term cost of purchasing decisions, such as buying a car or a home.

- Consider the opportunity cost of spending money today versus saving it for the future.

- Make informed decisions that align with your financial goals and priorities.

Examples:

- Choosing between a lump sum payment and an annuity: TVM can help you determine which option is more financially advantageous by calculating the present value of the annuity payments and comparing it to the lump sum payment.

- Deciding whether to invest in a new business venture: TVM can help you evaluate the potential profitability of the venture by forecasting future revenues and expenses and discounting them back to their present value.

- Planning for your child’s education: TVM can help you estimate how much you need to save each year to cover the cost of your child’s education, taking into account the time value of money and expected tuition increases.

- Evaluating a lease versus buy decision: TVM can help you determine whether it’s more cost-effective to lease or buy an asset by calculating the present value of the lease payments and comparing it to the cost of purchasing the asset.

Time Value of Money Formula

Time Value of Money Formula

By understanding and applying TVM principles, you can take control of your finances and make informed decisions that help you achieve your long-term financial goals. Whether you’re saving for retirement, investing in the stock market, or simply trying to manage your budget more effectively, TVM is an indispensable tool.

Ready to take control of your financial future? Explore money-central.com for in-depth articles, user-friendly tools, and expert advice to help you master the time value of money and achieve your financial goals. From calculators to personalized guidance, we’re here to support you every step of the way. Contact us at Address: 44 West Fourth Street, New York, NY 10012, United States or Phone: +1 (212) 998-0000. Start your journey to financial success today.

Frequently Asked Questions (FAQ)

1. What is the simplest definition of the time value of money?

The simplest definition is that money available today is worth more than the same amount in the future due to its potential earning capacity.

2. How does the time value of money affect investment decisions?

It allows investors to evaluate the profitability and attractiveness of investments by calculating the present value of future cash flows.

3. What is the difference between present value and future value?

Present value is the current worth of a future sum of money, while future value is the value of an asset at a specified date in the future.

4. Why is the discount rate important in TVM calculations?

The discount rate represents the rate of return required to compensate for the time value of money and the risk associated with future cash flows.

5. How does inflation impact the time value of money?

Inflation erodes the purchasing power of money over time, reducing the real value of future cash flows.

6. What is compounding, and how does it affect investment growth?

Compounding is earning returns on both the principal and accumulated interest, enhancing the growth of investments over time.

7. Can TVM be used for personal financial planning?

Yes, TVM is used for various personal financial planning aspects, including retirement planning, savings, and loan evaluations.

8. How do I choose an appropriate discount rate for TVM calculations?

Consider factors such as the risk of the investment, opportunity cost, and expected inflation rates when choosing a discount rate.

9. What tools are available to help calculate the time value of money?

Financial calculators, spreadsheet software, and online TVM calculators are widely available.

10. Is understanding TVM essential for business decisions?

Yes, businesses use TVM for capital budgeting, investment analysis, and evaluating the potential profitability of projects.