Withdrawing money from a Capital One credit card can offer a quick solution when you need cash, but it’s essential to understand the process, fees, and interest implications. At money-central.com, we provide clear, actionable insights to help you make informed financial decisions. This comprehensive guide will walk you through everything you need to know about Capital One cash advances, ensuring you’re well-prepared to manage your finances effectively and avoid unnecessary costs. Let’s explore the options available to you, so you can make the best choice for your financial situation, with information about financial products and cash flow management.

1. What is a Cash Advance and How Does it Work?

A cash advance is a service offered by most credit cards, including Capital One cards, that allows you to borrow cash from your available credit limit. Instead of using your card to make purchases, you can withdraw cash at an ATM or bank branch. While convenient, cash advances typically come with higher fees and interest rates compared to regular purchases.

1.1 How Cash Advances Work

With a cash advance, you’re essentially borrowing cash against your credit line. Here’s a breakdown of how it works:

- Accessing Funds: You can withdraw cash from an ATM using your credit card and PIN or visit a bank branch for assistance.

- Fees and Interest: Cash advances usually have transaction fees and higher interest rates that start accruing immediately.

- No Grace Period: Unlike regular purchases, cash advances don’t have a grace period, meaning interest charges begin from the moment you withdraw the money.

1.2 Reasons for Using a Cash Advance

Cash advances can be useful in specific situations:

- Cash-Only Transactions: When you need to pay for something with cash and don’t have other options.

- Emergencies: Unexpected expenses when you don’t have sufficient funds in your checking account.

However, it’s generally better to avoid cash advances if possible due to the associated costs. According to a study by the Federal Reserve, Americans paid over $120 billion in credit card interest and fees in 2023, highlighting the importance of understanding these costs.

1.3 Alternatives to Cash Advances

Before opting for a cash advance, consider these alternatives:

- Debit Card: Using your debit card to withdraw cash from your checking account.

- Personal Loan: If you need a larger sum of money, a personal loan may offer lower interest rates and more favorable terms.

- Emergency Fund: Tapping into your emergency fund to cover unexpected expenses.

2. Which Capital One Cards Offer Cash Advances?

All Capital One credit cards offer cash advances, but the fees and APRs can vary slightly. Here’s a detailed look at some popular Capital One cards and their cash advance terms:

2.1 Capital One Card Options

| Card Name | Cash Advance Offered? | Cash Advance Fee | Cash Advance APR (Variable) |

|---|---|---|---|

| Capital One Platinum Credit Card | Yes | $5 or 5% (whichever is greater) | 29.74% |

| Capital One Platinum Secured Credit Card | Yes | $5 or 5% (whichever is greater) | 29.74% |

| Capital One VentureOne Rewards Credit Card | Yes | $5 or 5% (whichever is greater) | 29.24% |

| Capital One Venture Rewards Credit Card | Yes | $5 or 5% (whichever is greater) | 29.24% |

| Capital One Venture X Rewards Credit Card | Yes | $5 or 5% (whichever is greater) | 29.24% |

| Capital One Quicksilver Cash Rewards Credit Card | Yes | $5 or 5% (whichever is greater) | 29.24% |

| Capital One Savor Cash Rewards Credit Card | Yes | $5 or 5% (whichever is greater) | 29.24% |

2.2 Understanding the Fees and APRs

- Cash Advance Fee: Typically, Capital One charges a fee of $5 or 5% of the transaction amount, whichever is greater. For example, if you withdraw $100, the fee would be $5. If you withdraw $500, the fee would be $25.

- Cash Advance APR: The Annual Percentage Rate (APR) for cash advances is generally higher than the APR for regular purchases. It can range from 29.24% to 31.24%, depending on the card.

2.3 Charge Cards vs. Credit Cards

Some Capital One cards, like the Capital One Spark Cash Plus, are charge cards. Charge cards don’t have an APR because you must pay the balance in full each month. While they still allow cash advances, they don’t accrue interest as long as you pay on time.

3. How to Get a Cash Advance with Capital One: Step-by-Step Guide

Getting a cash advance from your Capital One credit card is a straightforward process. Here’s how to do it:

3.1 At an ATM

- Find an ATM: You can use any ATM that accepts your credit card’s network (Visa or Mastercard). You don’t need to use a Capital One ATM, but using ATMs outside the Capital One or Allpoint networks may incur additional fees.

- Insert Your Card: Place your Capital One credit card into the ATM.

- Enter Your PIN: Enter your credit card’s PIN. If you don’t have a PIN, you’ll need to request one (see instructions below).

- Select “Cash Advance”: Choose the “Cash Advance” option. You may need to select “Credit” first.

- Enter the Amount: Follow the prompts to enter the amount you wish to withdraw.

- Confirm and Withdraw: Confirm the transaction and withdraw your cash.

3.2 At a Bank Branch

- Visit a Bank: Go to a bank branch that displays the Visa or Mastercard logo.

- Speak to a Teller: Present your Capital One credit card and a government-issued photo ID, such as a driver’s license.

- Request Cash Advance: Ask the teller for a cash advance.

- Receive Cash: After the transaction is approved, you’ll receive your cash from the teller.

3.3 How to Request a Cash Advance PIN Online

If you don’t have a PIN for your Capital One credit card, you can request one online:

- Log in to Your Account: Go to the Capital One website and log in to your account.

- Select Your Card: Choose the credit card you want to use for the cash advance.

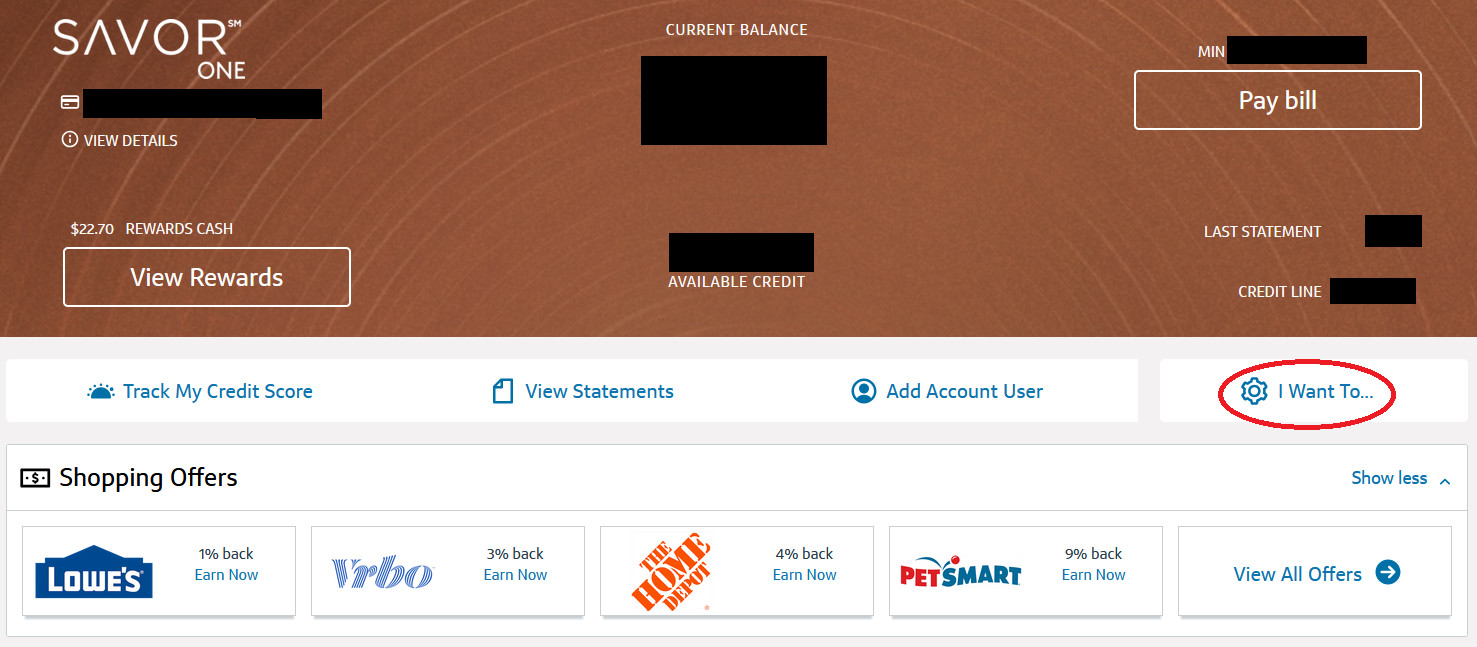

Screenshot of Capital One account showing the gear icon menu

Screenshot of Capital One account showing the gear icon menu - Navigate to “I Want To…”: Look for the “I Want To…” menu button, which usually has a gear icon next to it.

- Select “Get a Cash Advance PIN”: Scroll down to the “Control Your Card” section and choose “Get a Cash Advance PIN.”

Screenshot of Capital One website showing the Get a Cash Advance PIN option

Screenshot of Capital One website showing the Get a Cash Advance PIN option - Choose Delivery Method: Decide whether to receive your PIN in the mail or get it immediately via a security code and your phone.

Screenshot of Capital One website showing options for receiving a PIN

Screenshot of Capital One website showing options for receiving a PIN - Follow Instructions: Select “Get a PIN” and follow the remaining instructions to complete the process.

4. Key Considerations Before Getting a Cash Advance

Before you decide to get a cash advance, consider these important factors:

4.1 High Costs

Cash advances are one of the most expensive ways to borrow money due to high fees and APRs.

4.2 Immediate Interest Accrual

Interest on cash advances starts accruing immediately, without a grace period. This means you’ll start paying interest from the moment you withdraw the cash.

4.3 Impact on Credit Score

While getting a cash advance itself won’t directly impact your credit score, it can indirectly affect it. For instance, if the cash advance increases your credit utilization ratio (the amount of credit you’re using compared to your total available credit), it could negatively impact your score. According to Experian, keeping your credit utilization below 30% is ideal.

4.4 Lower Credit Limit

Cash advances reduce your available credit limit, which can affect your ability to make purchases on your credit card until you pay back the advance.

4.5 Prioritizing Payments

Payments made on your credit card may not automatically go toward the cash advance balance. Credit card companies often apply payments to balances with lower interest rates first. This means it may take longer to pay off the cash advance and reduce the accruing interest.

5. Strategies to Minimize the Cost of Cash Advances

If you must take out a cash advance, here are some strategies to minimize the costs:

5.1 Pay it Off Quickly

Since interest accrues immediately, the faster you pay off the cash advance, the less you’ll pay in interest charges. Try to pay it off within a few days or weeks, if possible.

5.2 Make Extra Payments

Make extra payments specifically targeted toward the cash advance balance. Contact Capital One to ensure your payments are applied correctly.

5.3 Consider Balance Transfers

If you have another credit card with a lower APR, consider transferring the cash advance balance to that card. Keep in mind that balance transfer fees may apply.

5.4 Review Your Spending Habits

Analyze why you needed the cash advance in the first place. Adjust your budget to avoid relying on cash advances in the future. Consider using budgeting apps like Mint or YNAB (You Need A Budget) to track your expenses and manage your finances more effectively.

6. Understanding Cash Advance Limits

Your Capital One credit card has a specific cash advance limit, which is usually lower than your overall credit limit.

6.1 How to Find Your Cash Advance Limit

- Check Your Statement: Your cash advance limit is usually listed on your monthly credit card statement.

- Online Account: Log in to your Capital One account online and view your card details.

- Call Customer Service: Contact Capital One customer service at +1 (212) 998-0000, and they can provide you with your cash advance limit.

6.2 Factors Affecting Your Cash Advance Limit

- Creditworthiness: Your credit score and credit history play a significant role in determining your cash advance limit.

- Income: Your income is also considered, as it indicates your ability to repay the borrowed funds.

- Payment History: A good payment history with Capital One can lead to a higher cash advance limit.

6.3 Requesting a Higher Limit

If you need a higher cash advance limit, you can request one from Capital One. However, approval is not guaranteed and depends on your creditworthiness and other factors.

7. Impact of Cash Advances on Credit Utilization

Credit utilization is the amount of credit you’re using compared to your total available credit. It’s a significant factor in your credit score.

7.1 How Cash Advances Affect Utilization

A cash advance increases your credit utilization, which can negatively impact your credit score if it pushes you over the recommended threshold (below 30%).

7.2 Example of Credit Utilization

Let’s say you have a credit card with a $5,000 credit limit. If you take out a cash advance of $1,500, your credit utilization is 30% ($1,500 / $5,000). If you already had a balance of $500, your total utilization would be 40% (($1,500 + $500) / $5,000), which could negatively impact your credit score.

7.3 Strategies to Manage Credit Utilization

- Pay Down Balances: Reduce your outstanding balances as quickly as possible.

- Request a Credit Limit Increase: A higher credit limit can lower your utilization ratio, even if your spending remains the same.

- Monitor Your Credit Score: Regularly check your credit score to see how your financial habits are affecting it.

8. Cash Advances vs. Other Borrowing Options

When you need cash, it’s essential to consider all your borrowing options to choose the most cost-effective one.

8.1 Personal Loans

- Pros: Lower interest rates, fixed repayment terms, larger borrowing amounts.

- Cons: Requires a credit check, may take time to get approved.

8.2 Home Equity Loans

- Pros: Lower interest rates, secured by your home.

- Cons: Requires equity in your home, risk of foreclosure if you can’t repay.

8.3 Payday Loans

- Pros: Quick access to cash, no credit check.

- Cons: Extremely high interest rates and fees, short repayment terms.

8.4 Comparing Options

| Borrowing Option | Interest Rates | Fees | Repayment Terms |

|---|---|---|---|

| Cash Advance | High | Transaction | Flexible |

| Personal Loan | Moderate | Origination | Fixed |

| Home Equity Loan | Low | Appraisal | Fixed |

| Payday Loan | Very High | High Fees | Very Short |

9. Tips for Managing Your Capital One Credit Card Effectively

To avoid the need for cash advances and manage your credit card responsibly, follow these tips:

9.1 Create a Budget

Develop a budget to track your income and expenses. This will help you identify areas where you can save money and avoid overspending.

9.2 Set Up Payment Reminders

Set up payment reminders to ensure you never miss a due date. Late payments can result in late fees and negatively impact your credit score.

9.3 Use Automatic Payments

Enroll in automatic payments to have your credit card bill paid automatically each month. This can help you avoid late payments and maintain a good credit history.

9.4 Monitor Your Credit Card Activity

Regularly check your credit card statements and online account for any unauthorized transactions or errors. Report any discrepancies to Capital One immediately.

9.5 Avoid Maxing Out Your Credit Card

Keep your credit utilization low by not maxing out your credit card. Aim to use less than 30% of your available credit.

10. Frequently Asked Questions (FAQs) About Capital One Cash Advances

10.1 Can I Get a Cash Advance with Any Capital One Credit Card?

Yes, all Capital One credit cards currently offer cash advances.

10.2 What is the Cash Advance Fee for Capital One Cards?

The cash advance fee is typically $5 or 5% of the transaction amount, whichever is greater.

10.3 What is the Interest Rate on Capital One Cash Advances?

The interest rate (APR) ranges from 29.24% to 31.24%, depending on the card.

10.4 How Can I Find My Cash Advance Limit?

You can find your cash advance limit on your credit card statement, online account, or by calling Capital One customer service.

10.5 Can I Use a Capital One ATM for Cash Advances?

Yes, you can use a Capital One ATM, but it’s not required. Any ATM that accepts your card’s network (Visa or Mastercard) will work.

10.6 How Do I Request a PIN for My Capital One Credit Card?

You can request a PIN online through your Capital One account or by calling customer service.

10.7 Do Cash Advances Affect My Credit Score?

Yes, indirectly. Cash advances can increase your credit utilization, which can negatively impact your credit score if it exceeds the recommended threshold.

10.8 Are There Alternatives to Cash Advances?

Yes, alternatives include using a debit card, personal loans, or tapping into your emergency fund.

10.9 How Can I Minimize the Cost of a Cash Advance?

Pay it off quickly, make extra payments, consider balance transfers, and review your spending habits.

10.10 What Happens If I Can’t Repay My Cash Advance?

If you can’t repay your cash advance, you’ll incur late fees and continue to accrue interest, which can damage your credit score and lead to debt accumulation.

Conclusion

While withdrawing money from a Capital One credit card through a cash advance can provide quick access to funds, it’s important to be aware of the high costs involved. By understanding the fees, interest rates, and potential impact on your credit score, you can make informed decisions about your financial needs. At money-central.com, we strive to provide you with the knowledge and tools necessary to manage your finances effectively.

If you’re facing financial challenges or need advice on managing your credit card debt, we encourage you to explore our resources and seek professional financial guidance. Visit money-central.com for more articles, tools, and expert advice to help you achieve your financial goals. Our address is 44 West Fourth Street, New York, NY 10012, United States. You can also contact us at Phone: +1 (212) 998-0000 or visit our website at money-central.com for further assistance and personalized financial solutions. Take control of your financial future today and make informed decisions that lead to long-term financial stability and success.