Withdrawing money from your Health Savings Account (HSA) is straightforward when you understand the rules. This comprehensive guide from money-central.com will walk you through the process, covering everything from eligible expenses to different withdrawal scenarios, ensuring you maximize the benefits of your HSA while staying compliant. Whether you’re planning for medical expenses, retirement, or simply seeking financial flexibility, mastering HSA withdrawals is key to effective financial management.

1. What Is a Health Savings Account (HSA) and How Does It Work?

An HSA is a tax-advantaged savings account specifically designed for individuals with a High Deductible Health Plan (HDHP). Contributions to an HSA are tax-deductible, the funds grow tax-free, and withdrawals for qualified medical expenses are also tax-free. It’s a triple tax advantage, making it a powerful tool for managing healthcare costs and saving for the future.

According to the IRS, for 2024, an HDHP is defined as a health plan with a deductible of at least $1,600 for an individual or $3,200 for a family. The annual out-of-pocket expenses (including deductibles, co-payments, and co-insurance) cannot exceed $8,050 for an individual or $16,100 for a family.

2. What Are the Key Benefits of Having an HSA?

HSAs offer several compelling benefits, including:

- Tax Advantages: As mentioned, HSAs provide a triple tax benefit: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

- Portability: The HSA is yours, even if you change jobs or health plans.

- Investment Opportunities: Many HSAs allow you to invest your contributions, providing the potential for growth over time.

- Flexibility: You can use the funds for current medical expenses or save them for future healthcare needs, even in retirement.

3. What Are Considered Qualified Medical Expenses for HSA Withdrawals?

Understanding what qualifies as a medical expense is crucial for avoiding penalties. Qualified medical expenses include costs for the diagnosis, cure, mitigation, treatment, or prevention of disease, and for treatments affecting any part or function of the body.

Examples of qualified medical expenses include:

- Copays

- Coinsurance

- Deductibles

- Prescriptions

- Dental Care

- Eye Care

- Medical equipment

- Mental health services

- Transportation costs to receive medical care

The IRS Publication 502 provides a comprehensive list of qualified medical expenses. Keep detailed records of your medical expenses to ensure compliance.

4. What Happens If I Use HSA Funds for Non-Qualified Expenses?

If you withdraw funds from your HSA for non-qualified expenses before age 65, the withdrawn amount is subject to income tax and a 20% penalty. After age 65, withdrawals for non-qualified expenses are subject to income tax but not the 20% penalty.

For example, if you withdraw $1,000 for a vacation before age 65, you’ll pay income tax on the $1,000 and an additional $200 penalty.

5. How Can I Withdraw Money From My HSA?

Most HSAs offer multiple ways to access your funds:

- Debit Card: Many HSAs provide a debit card that you can use to pay for qualified medical expenses directly at the point of sale.

- Checks: Some HSAs supply checks that you can use to pay for medical expenses.

- Online Payment Systems: Many HSAs have online payment systems that allow you to pay bills directly from your account.

- Reimbursement: You can pay for expenses out-of-pocket and then reimburse yourself from your HSA.

Regardless of the method you choose, keep detailed records of all transactions and expenses.

6. What Is the Process for Reimbursing Myself From My HSA?

To reimburse yourself from your HSA, follow these steps:

- Pay for the Qualified Medical Expense: Pay for the expense out-of-pocket.

- Gather Documentation: Collect the receipt and any other required documentation.

- Submit a Claim: Submit a claim to your HSA administrator, along with the documentation.

- Receive Reimbursement: The HSA administrator will either mail you a check or deposit the amount into your checking or savings account.

Ensure that you submit your claim promptly and keep copies of all documentation for your records.

7. How Does Age Affect HSA Withdrawals?

Age plays a significant role in how HSA withdrawals are taxed and penalized.

- Under Age 65: Withdrawals for qualified medical expenses are tax-free. Withdrawals for non-qualified expenses are subject to income tax and a 20% penalty.

- Age 65 and Older: Withdrawals for qualified medical expenses are tax-free. Withdrawals for non-qualified expenses are subject to income tax but are not subject to the 20% penalty. At this age, the HSA functions more like a traditional retirement account.

This change at age 65 provides added flexibility, allowing you to use the funds for any purpose, albeit with income tax implications for non-medical expenses.

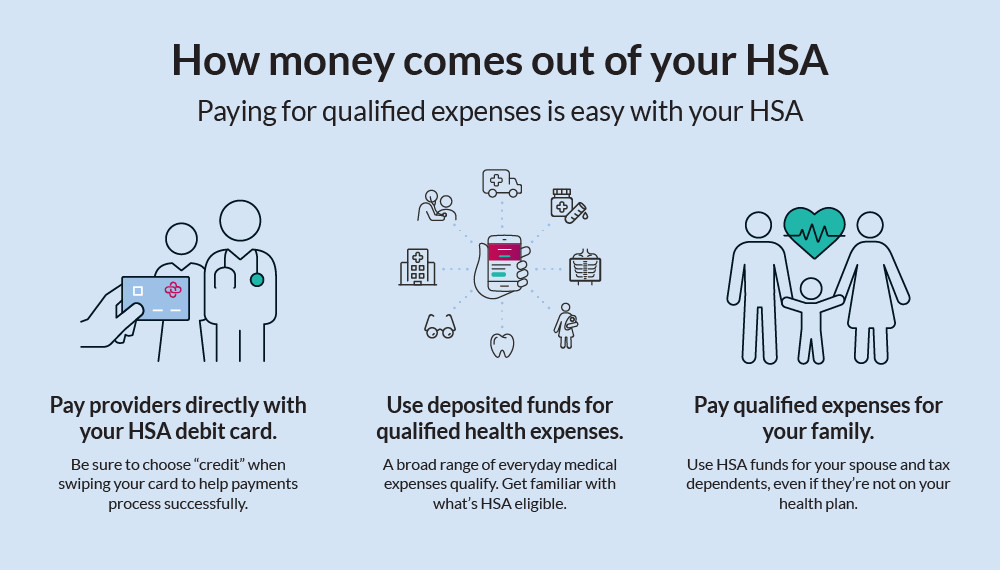

8. Can I Use My HSA to Pay for My Spouse’s or Dependents’ Medical Expenses?

Yes, you can use your HSA to pay for qualified medical expenses for yourself, your spouse, and your dependents, even if they are not covered by your HDHP. A dependent is defined as someone who qualifies as your dependent under IRS rules.

This flexibility allows you to use your HSA to cover healthcare costs for your entire family, making it a valuable tool for family financial planning.

9. What Happens to My HSA If I No Longer Have a High Deductible Health Plan (HDHP)?

If you no longer have an HDHP, you can no longer contribute to your HSA, but you can still use the funds in your account for qualified medical expenses. The HSA remains yours, and the funds continue to grow tax-free.

If you later re-enroll in an HDHP, you can resume making contributions to your HSA, provided you meet all other eligibility requirements.

10. How Do Self-Directed and Investment HSAs Affect Withdrawals?

Self-directed and investment HSAs allow you to invest your contributions in various assets, such as stocks, bonds, and mutual funds. This can provide the potential for higher growth but also adds complexity to the withdrawal process.

To withdraw funds from an investment HSA:

- Transfer Funds to Cash Account: If the funds are invested, you must first transfer them from your investment account to your cash account.

- Sell Investments (If Necessary): If you don’t have enough cash in your investment account, you may need to sell some of your investments.

- Withdraw Funds: Once the funds are in your cash account, you can withdraw them using a debit card, check, or online payment system, or reimburse yourself.

Keep in mind that selling investments may have tax implications, and the transfer process can take a few days.

11. What Are the Rules for Transferring or Rolling Over HSA Funds?

There may be situations where you want to move your HSA funds to a different provider. You can do this through either a rollover or a transfer.

- Rollover: The HSA provider sends you a check, and you have 60 days to deposit the funds into a new HSA. You can only do one rollover per 12-month period.

- Transfer: The HSA provider sends the funds directly to the new HSA. There are no limits on the number of transfers you can make.

Transfers are generally simpler and more convenient, as you don’t have to handle the funds yourself.

12. Are There Limits to the Number of Withdrawals I Can Make From My HSA?

No, there are no limits to the number of withdrawals you can make from your HSA. However, it’s essential to ensure that all withdrawals are for qualified medical expenses to avoid taxes and penalties.

Be mindful of your contribution limits, which are set by the IRS each year. For 2024, the contribution limits are $4,150 for individuals and $8,300 for families, with an additional $1,000 catch-up contribution for those age 55 and older.

13. What Records Should I Keep for HSA Withdrawals?

Maintaining detailed records is crucial for justifying your HSA withdrawals and avoiding tax issues. Keep the following records:

- Receipts: Keep all receipts for medical expenses, including the date, amount, and description of the service.

- Explanation of Benefits (EOB): Obtain an EOB from your insurance provider for each medical service.

- HSA Statements: Keep your HSA statements to track contributions, withdrawals, and investment activity.

Store these records securely and keep them for at least three years, in case of an audit.

14. How Do I Handle HSA Withdrawals on My Tax Return?

When filing your taxes, you’ll need to report your HSA contributions and withdrawals on Form 8889, Health Savings Accounts (HSAs). This form helps you calculate your HSA deduction, report any taxable withdrawals, and determine if you owe any penalties.

Follow the instructions on Form 8889 carefully and consult with a tax professional if you have any questions.

15. What Are Some Common Mistakes to Avoid When Making HSA Withdrawals?

To avoid costly mistakes, keep the following points in mind:

- Incorrectly Classifying Expenses: Make sure that all withdrawals are for qualified medical expenses.

- Failing to Keep Records: Maintain detailed records of all expenses and withdrawals.

- Exceeding Contribution Limits: Stay within the annual contribution limits set by the IRS.

- Not Understanding Investment Options: If you have an investment HSA, understand the risks and potential tax implications of your investment choices.

By avoiding these common mistakes, you can maximize the benefits of your HSA and avoid unnecessary taxes and penalties.

16. How Can I Use My HSA as a Retirement Savings Tool?

One of the most attractive features of an HSA is its potential as a retirement savings tool. Because withdrawals for qualified medical expenses are tax-free, you can use your HSA to cover healthcare costs in retirement, when medical expenses tend to be higher.

Even if you don’t use the funds for medical expenses, after age 65, you can withdraw the money for any purpose, subject to income tax. This makes the HSA a flexible and tax-advantaged way to save for retirement.

17. What Happens to My HSA When I Die?

What happens to your HSA depends on who inherits it:

- Spouse: If your spouse inherits your HSA, it becomes their HSA, and they can continue to use the funds for qualified medical expenses.

- Non-Spouse Beneficiary: If a non-spouse beneficiary inherits your HSA, the account ceases to be an HSA, and the beneficiary must include the fair market value of the HSA in their gross income for the year. The amount is subject to income tax but not to the 20% penalty.

It’s essential to designate a beneficiary for your HSA to ensure that the funds are distributed according to your wishes.

18. How Does Medicare Enrollment Affect My HSA?

Once you enroll in Medicare, you can no longer contribute to your HSA. However, you can still use the funds in your HSA for qualified medical expenses, including Medicare premiums (excluding Medigap premiums).

It’s important to plan your Medicare enrollment carefully to maximize your HSA benefits.

19. What Are the Best Strategies for Managing My HSA?

To make the most of your HSA, consider these strategies:

- Contribute Regularly: Maximize your contributions each year to take full advantage of the tax benefits.

- Invest Wisely: If your HSA allows investments, choose investments that align with your risk tolerance and time horizon.

- Pay for Medical Expenses Strategically: Consider paying for medical expenses out-of-pocket and saving your HSA funds for future healthcare needs.

- Keep Detailed Records: Maintain thorough records of all contributions, withdrawals, and medical expenses.

- Review Your HSA Regularly: Periodically review your HSA to ensure it meets your needs and that you are taking full advantage of its benefits.

20. Where Can I Find More Information and Resources About HSAs?

For more information and resources about HSAs, consider these sources:

- IRS Publications: Consult IRS Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans, and IRS Publication 502, Medical and Dental Expenses.

- HSA Administrators: Contact your HSA administrator for information about your account and eligible expenses.

- Financial Advisors: Seek advice from a qualified financial advisor.

- money-central.com: Explore our website for articles, tools, and resources on HSAs and other financial topics.

By staying informed and proactive, you can effectively manage your HSA and achieve your financial goals.

HSA distribution infographic illustrating how money is withdrawn

HSA distribution infographic illustrating how money is withdrawn

21. How to Withdraw Funds From Your HSA

Withdrawing funds from your HSA is a crucial aspect of managing your healthcare finances effectively. The method you use will depend on your HSA provider and the resources available to you. Here’s a detailed look at the common ways to withdraw funds, ensuring you stay compliant with IRS regulations.

22. Using an HSA Debit Card

Many HSA providers offer a debit card linked directly to your HSA. This card can be used at pharmacies, doctor’s offices, and other healthcare providers to pay for qualified medical expenses.

Benefits of Using an HSA Debit Card:

- Convenience: It’s a straightforward way to pay for eligible expenses at the point of sale.

- Real-Time Access: Funds are immediately available, making it easier to manage your healthcare costs.

How to Use an HSA Debit Card:

- Verify Eligibility: Ensure the expense is a qualified medical expense according to IRS guidelines.

- Swipe the Card: Use the card just like any other debit card at the healthcare provider.

- Keep Records: Save the receipt as proof of the qualified medical expense for tax purposes.

Using an HSA debit card simplifies the payment process, but maintaining accurate records is critical for tax compliance.

23. Writing a Check From Your HSA

Some HSA providers offer check-writing privileges, allowing you to write checks directly from your HSA to pay for qualified medical expenses.

Benefits of Writing a Check:

- Flexibility: Useful for paying providers who may not accept debit cards.

- Record Keeping: Provides a clear paper trail of your transactions.

How to Write a Check From Your HSA:

- Ensure Funds are Available: Verify that you have sufficient funds in your HSA to cover the expense.

- Write the Check: Fill out the check with the payee’s name, the amount, and a memo indicating the purpose of the payment (e.g., “Medical Expense”).

- Keep a Copy: Retain a copy of the check for your records.

Writing checks from your HSA provides flexibility, especially when dealing with providers who have limited payment options.

24. Online Bill Payment Through Your HSA Portal

Many HSA administrators offer online portals that allow you to pay bills directly from your HSA. This feature is particularly useful for managing healthcare expenses efficiently.

Benefits of Online Bill Payment:

- Efficiency: Streamlines the bill payment process.

- Tracking: Provides a digital record of all transactions.

How to Use Online Bill Payment:

- Log Into Your HSA Portal: Access your HSA account through the online portal provided by your administrator.

- Add Payee: Enter the healthcare provider’s information as a payee.

- Make Payment: Schedule or make a one-time payment from your HSA to the provider.

- Save Confirmation: Save a confirmation of the payment for your records.

Online bill payment enhances the convenience of managing your HSA funds and provides a clear audit trail.

25. Reimbursing Yourself for Out-of-Pocket Expenses

You can also pay for qualified medical expenses out-of-pocket and then reimburse yourself from your HSA. This strategy can be beneficial if you want to keep your HSA funds invested for a longer period.

Benefits of Reimbursement:

- Investment Growth: Allows your HSA funds to continue growing tax-free.

- Flexibility: Provides the option to pay expenses now and reimburse yourself later.

How to Reimburses Yourself:

- Pay Out-of-Pocket: Pay for the qualified medical expense using your personal funds.

- Gather Documentation: Collect all receipts and Explanation of Benefits (EOB) statements.

- Submit a Claim: Submit a reimbursement claim through your HSA portal, including the necessary documentation.

- Receive Funds: The HSA administrator will deposit the funds into your designated bank account.

Reimbursing yourself requires careful documentation but can be a strategic way to maximize the growth potential of your HSA.

26. What Happens if You Withdraw Funds in Error?

Even with careful planning, you might occasionally withdraw funds from your HSA in error. It’s important to rectify these situations quickly to avoid tax penalties.

Steps to Take if You Withdraw Funds in Error:

- Notify Your HSA Administrator: Contact your HSA administrator as soon as possible to report the error.

- Return the Funds: Return the withdrawn amount to your HSA promptly.

- Document the Correction: Keep a record of the error and the correction for tax purposes.

Correcting errors promptly helps maintain compliance and ensures you continue to benefit from the tax advantages of your HSA.

27. Common HSA Withdrawal Scenarios and How to Handle Them

Understanding various withdrawal scenarios can help you manage your HSA effectively and avoid common pitfalls.

28. Scenario 1: Paying for Routine Medical Appointments

Using your HSA to pay for routine medical appointments, such as check-ups and vaccinations, is straightforward.

How to Handle It:

- Use Your HSA Debit Card: Pay directly at the doctor’s office with your HSA debit card.

- Keep the Receipt: Save the receipt as proof of the qualified medical expense.

- Consider Reimbursement: If you prefer, pay out-of-pocket and reimburse yourself later through the HSA portal.

Paying for routine medical appointments with your HSA ensures you’re using your tax-advantaged funds for eligible expenses.

29. Scenario 2: Managing Prescription Costs

Prescription costs can be a significant healthcare expense. Your HSA can be an invaluable tool for managing these costs effectively.

How to Handle It:

- Pay at the Pharmacy: Use your HSA debit card at the pharmacy to pay for prescriptions.

- Submit a Claim: If you pay out-of-pocket, submit a claim with the prescription receipt through your HSA portal.

- Consider Mail-Order Pharmacies: Some mail-order pharmacies may offer cost savings and accept HSA payments.

Managing prescription costs through your HSA helps you leverage the tax benefits for ongoing medical needs.

30. Scenario 3: Dealing with Emergency Medical Expenses

Emergency medical expenses can arise unexpectedly. Knowing how to use your HSA in these situations can provide financial relief.

How to Handle It:

- Pay with HSA Funds: If possible, use your HSA debit card or online bill payment to cover emergency medical expenses.

- Reimburse Yourself: If you use personal funds, gather all documentation and submit a reimbursement claim promptly.

- Prioritize Documentation: In stressful situations, ensure you collect and retain all necessary receipts and EOB statements.

Having an HSA can provide peace of mind when dealing with unexpected medical emergencies.

31. Scenario 4: Paying for Dental and Vision Care

Dental and vision expenses are often significant and may not be fully covered by your health insurance. Your HSA can help offset these costs.

How to Handle It:

- Use HSA Funds: Pay for dental and vision appointments and procedures with your HSA debit card or online bill payment.

- Submit Claims: If you pay out-of-pocket, submit claims with the necessary documentation through your HSA portal.

- Keep Detailed Records: Ensure you keep detailed records of all dental and vision expenses for tax purposes.

Leveraging your HSA for dental and vision care allows you to maximize the tax advantages for comprehensive healthcare needs.

32. Key Takeaways for Managing HSA Withdrawals

Effectively managing your HSA withdrawals involves understanding the rules, keeping detailed records, and utilizing the available resources. Here are the key takeaways:

- Know the Rules: Understand what constitutes a qualified medical expense according to IRS guidelines.

- Keep Detailed Records: Maintain thorough records of all contributions, withdrawals, and medical expenses.

- Utilize Available Resources: Take advantage of the tools and resources provided by your HSA administrator.

- Plan Strategically: Consider the long-term benefits of your HSA and plan your withdrawals accordingly.

By following these guidelines, you can maximize the benefits of your HSA and achieve your financial and healthcare goals.

33. Optimizing Your HSA for Long-Term Financial Health

Your HSA is more than just a tool for managing current healthcare expenses; it’s a powerful vehicle for long-term financial health. By optimizing your HSA, you can leverage its tax advantages to build a secure financial future.

34. Maximize Contributions

One of the most effective ways to optimize your HSA is to contribute the maximum amount each year. The more you contribute, the more you benefit from the tax advantages.

Benefits of Maximizing Contributions:

- Tax Savings: Reduces your taxable income, providing immediate tax relief.

- Investment Growth: Allows your funds to grow tax-free over time.

- Future Healthcare Needs: Builds a substantial nest egg for future healthcare expenses.

Tips for Maximizing Contributions:

- Budgeting: Review your budget and identify areas where you can save money to contribute to your HSA.

- Payroll Deductions: Set up automatic payroll deductions to ensure consistent contributions.

- Catch-Up Contributions: If you’re age 55 or older, take advantage of the additional catch-up contributions.

35. Invest Wisely

Many HSAs offer investment options, allowing you to grow your funds tax-free. Choosing the right investments is crucial for maximizing the long-term potential of your HSA.

Benefits of Investing Wisely:

- Tax-Free Growth: Investments grow tax-free, providing a significant advantage over taxable investment accounts.

- Potential for Higher Returns: Investments can generate higher returns than traditional savings accounts.

- Inflation Hedge: Investments can help your HSA funds keep pace with inflation, preserving their purchasing power.

Tips for Investing Wisely:

- Assess Your Risk Tolerance: Determine your risk tolerance and choose investments that align with your comfort level.

- Diversify Your Portfolio: Diversify your portfolio to reduce risk and maximize potential returns.

- Consider Low-Cost Index Funds: Low-cost index funds can provide broad market exposure with minimal fees.

- Rebalance Regularly: Rebalance your portfolio periodically to maintain your desired asset allocation.

36. Pay for Current Medical Expenses Strategically

While it may be tempting to use your HSA to pay for all current medical expenses, consider paying for some expenses out-of-pocket and saving your HSA funds for future healthcare needs.

Benefits of Strategic Spending:

- Long-Term Growth: Allows your HSA funds to continue growing tax-free.

- Future Healthcare Needs: Builds a larger nest egg for future healthcare expenses, especially in retirement.

- Tax-Free Reimbursement: You can reimburse yourself for past medical expenses at any time, as long as you have the documentation.

Tips for Strategic Spending:

- Prioritize Essential Expenses: Use your HSA for essential medical expenses, such as prescriptions and doctor visits.

- Pay for Routine Expenses Out-of-Pocket: Consider paying for routine expenses, such as over-the-counter medications, out-of-pocket.

- Keep Detailed Records: Maintain detailed records of all medical expenses, even those you pay out-of-pocket.

37. Review and Adjust Your HSA Regularly

Your financial situation and healthcare needs may change over time. It’s important to review your HSA regularly and make adjustments as needed.

Benefits of Regular Review:

- Alignment with Goals: Ensures your HSA continues to align with your financial and healthcare goals.

- Optimization: Identifies opportunities to optimize your HSA, such as adjusting your investment allocation or contribution level.

- Compliance: Helps you stay compliant with IRS regulations.

Tips for Regular Review:

- Annual Review: Conduct an annual review of your HSA, ideally during tax season.

- Assess Your Needs: Assess your current and future healthcare needs and adjust your HSA accordingly.

- Consult with a Financial Advisor: Seek advice from a qualified financial advisor to ensure you’re making the most of your HSA.

By optimizing your HSA for long-term financial health, you can build a secure financial future and ensure you have the resources you need to manage your healthcare expenses effectively.

38. How money-central.com Can Help You Manage Your HSA

Managing your HSA effectively requires knowledge, tools, and resources. money-central.com is dedicated to providing you with the information and support you need to make the most of your HSA.

39. Comprehensive Articles and Guides

money-central.com offers a wealth of articles and guides on HSAs, covering everything from the basics to advanced strategies.

Topics Covered Include:

- What is an HSA and how does it work?

- The benefits of having an HSA

- How to choose the right HSA

- How to contribute to an HSA

- How to withdraw funds from an HSA

- How to invest your HSA funds

- How to use your HSA for retirement savings

- Common HSA mistakes to avoid

- HSA FAQs

Our articles are written by experienced financial professionals and are regularly updated to reflect the latest IRS regulations and industry best practices.

40. HSA Calculators and Tools

money-central.com provides a range of calculators and tools to help you manage your HSA effectively.

Tools Available Include:

- HSA Contribution Calculator: Calculate how much you can contribute to your HSA each year.

- HSA Withdrawal Calculator: Estimate the tax implications of withdrawing funds from your HSA.

- HSA Investment Calculator: Project the potential growth of your HSA investments.

- HSA Comparison Tool: Compare different HSA providers and find the best option for your needs.

Our calculators and tools are designed to be user-friendly and provide you with valuable insights to help you make informed decisions.

41. Expert Advice and Support

money-central.com connects you with experienced financial advisors who can provide personalized advice and support for managing your HSA.

Benefits of Expert Advice:

- Personalized Guidance: Receive tailored advice based on your unique financial situation and healthcare needs.

- Strategic Planning: Develop a comprehensive HSA management plan to help you achieve your goals.

- Ongoing Support: Access ongoing support and guidance to ensure you’re making the most of your HSA.

Our financial advisors are knowledgeable about HSAs and can help you navigate the complexities of HSA management.

42. Stay Updated with the Latest News and Trends

money-central.com keeps you informed about the latest news and trends in the HSA industry.

Stay Informed About:

- IRS Regulations: Stay up-to-date on the latest IRS regulations and guidelines for HSAs.

- Industry News: Learn about the latest developments in the HSA industry.

- Investment Trends: Discover the latest investment trends and strategies for HSAs.

- Healthcare Reform: Understand how healthcare reform may impact your HSA.

Our team of experts monitors the HSA landscape and provides you with timely and relevant information to help you stay ahead of the curve.

Ready to Take Control of Your Financial Future?

Visit money-central.com today to explore our comprehensive resources on HSAs and other financial topics. Whether you’re just getting started with an HSA or looking to optimize your existing account, we have the tools and information you need to succeed.

Take the Next Step:

- Read our articles and guides on HSAs.

- Use our calculators and tools to manage your HSA effectively.

- Connect with a financial advisor for personalized advice and support.

- Stay updated with the latest news and trends in the HSA industry.

At money-central.com, we’re committed to helping you achieve your financial goals. Let us be your trusted resource for all things HSA.

FAQ: How To Withdraw Money From My Hsa Account

43. Can I withdraw money from my HSA for non-medical expenses?

Yes, but there are different implications depending on your age. Before age 65, withdrawals for non-qualified expenses are subject to income tax and a 20% penalty. After age 65, withdrawals for non-qualified expenses are subject to income tax but not the 20% penalty.

44. What are qualified medical expenses for HSA withdrawals?

Qualified medical expenses include costs for the diagnosis, cure, mitigation, treatment, or prevention of disease, and for treatments affecting any part or function of the body. Examples include doctor visits, prescriptions, dental care, and vision care.

45. How do I withdraw money from my HSA?

You can withdraw funds using an HSA debit card, writing a check, online bill payment through your HSA portal, or reimbursing yourself for out-of-pocket expenses.

46. What happens if I withdraw funds in error from my HSA?

Notify your HSA administrator as soon as possible, return the funds to your HSA promptly, and document the correction for tax purposes.

47. Can I use my HSA to pay for my spouse’s or dependents’ medical expenses?

Yes, you can use your HSA to pay for qualified medical expenses for yourself, your spouse, and your dependents, even if they are not covered by your HDHP.

48. What records should I keep for HSA withdrawals?

Keep receipts for medical expenses, Explanation of Benefits (EOB) statements, and HSA statements to track contributions, withdrawals, and investment activity.

49. How does age affect HSA withdrawals?

Before age 65, non-qualified withdrawals are subject to income tax and a 20% penalty. After age 65, non-qualified withdrawals are subject to income tax but not the penalty.

50. What happens to my HSA if I no longer have a High Deductible Health Plan (HDHP)?

You can no longer contribute to your HSA, but you can still use the funds in your account for qualified medical expenses.

51. How do self-directed and investment HSAs affect withdrawals?

You may need to transfer funds from your investment account to your cash account before withdrawing. Selling investments may have tax implications and can take a few days.

52. Are there limits to the number of withdrawals I can make from my HSA?

No, there are no limits to the number of withdrawals you can make, but all withdrawals must be for qualified medical expenses to avoid taxes and penalties.

Remember, money-central.com is here to help you navigate the complexities of HSA management. For more information and resources, visit our website today.

Address: 44 West Fourth Street, New York, NY 10012, United States.

Phone: +1 (212) 998-0000.

Website: money-central.com.