Is The Fema Money A Loan? At money-central.com, we understand that navigating financial assistance programs can be complex, especially during times of crisis. The Federal Emergency Management Agency (FEMA) offers various forms of aid, and it’s crucial to differentiate between what needs to be repaid and what doesn’t. Let’s explore FEMA’s financial programs, focusing on the key distinctions and providing insights into managing your finances during and after a disaster, covering aid eligibility, application, and maximizing benefits.

1. Understanding FEMA’s Disaster Assistance Programs

The Federal Emergency Management Agency (FEMA) provides critical assistance to individuals and communities recovering from natural disasters. Understanding the types of financial aid FEMA offers is essential to navigate the recovery process effectively.

1.1. What Types of Assistance Does FEMA Offer?

FEMA offers several types of assistance, including grants and loans, each designed to address specific needs following a disaster.

- Grants: These are typically need-based and do not require repayment. They cover essential expenses like housing, medical care, and personal property replacement.

- Loans: These are offered through the Small Business Administration (SBA) and must be repaid with interest. They are designed to help businesses and homeowners repair or replace damaged property.

1.2. How FEMA Grants Work

FEMA grants are a vital component of disaster recovery, providing financial aid to help individuals and families get back on their feet.

1.2.1. Eligibility Criteria for FEMA Grants

To qualify for a FEMA grant, you must meet certain criteria, including:

- Registration: Register with FEMA after a disaster declaration.

- Identification: Provide proof of identity and residency.

- Damage Verification: Document the damage to your property and personal belongings.

- Insurance: Show that you have insurance coverage and the benefits you’ve received.

1.2.2. Types of Expenses Covered by FEMA Grants

FEMA grants can cover a range of expenses, including:

- Housing Assistance: Temporary housing, rental assistance, and home repairs.

- Medical Expenses: Uninsured medical bills related to the disaster.

- Personal Property Replacement: Replacing essential household items and clothing.

- Other Needs: Assistance with funeral expenses, transportation, and other disaster-related costs.

1.3. SBA Disaster Loans: An Overview

While FEMA primarily provides grants, the Small Business Administration (SBA) offers disaster loans that can be a crucial resource for long-term recovery.

1.3.1. Types of SBA Disaster Loans

The SBA offers several types of disaster loans, each tailored to different needs:

- Home Disaster Loans: Help homeowners repair or replace damaged property.

- Business Physical Disaster Loans: Assist businesses in repairing or replacing physical assets.

- Economic Injury Disaster Loans (EIDL): Provide financial assistance to businesses that have suffered economic losses due to the disaster.

1.3.2. Key Differences Between FEMA Grants and SBA Loans

It’s crucial to understand the differences between FEMA grants and SBA loans:

- Repayment: FEMA grants do not require repayment, while SBA loans must be repaid with interest.

- Purpose: FEMA grants cover immediate, essential needs, while SBA loans are for long-term recovery and rebuilding.

- Eligibility: FEMA grants are available to individuals and families, while SBA loans are primarily for homeowners and businesses.

1.4. FEMA’s Safeguarding Tomorrow Revolving Loan Fund (RLF) Program

FEMA’s Safeguarding Tomorrow Revolving Loan Fund (RLF) program is a new initiative designed to provide low-interest loans for hazard mitigation projects. Understanding how this program works is crucial for communities looking to build resilience against future disasters.

1.4.1. How the RLF Program Works

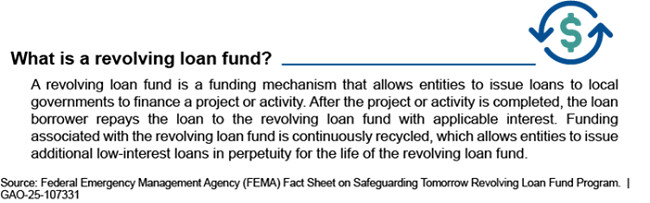

The RLF program operates by providing capitalization grants to eligible states, territories, tribes, and the District of Columbia. These entities then establish revolving loan funds that issue loans to localities for hazard mitigation projects. As these loans are repaid, the funds are recycled to finance additional projects, creating a sustainable source of funding.

1.4.2. Eligibility and Application Process

To participate in the RLF program, states and other eligible entities must apply to FEMA for capitalization grants. The application process involves submitting potential projects and demonstrating the hazard mitigation needs of their communities. FEMA reviews these applications and selects awardees based on their ability to effectively manage and administer the revolving loan funds.

FEMA's Revolving Loan Fund

FEMA's Revolving Loan Fund

Alt text: FEMA’s definition of a Revolving Loan Fund as a sustainable source of funding for hazard mitigation projects, showcasing how initial grants lead to loans, project implementation, and fund repayment for future projects.

2. Is FEMA Money a Loan?

One of the most common questions people have after a disaster is, “Is the FEMA money a loan?” Understanding the types of assistance provided by FEMA is crucial. Generally, FEMA assistance comes in the form of grants, which do not need to be repaid. However, there are situations where FEMA might refer you to the Small Business Administration (SBA) for a disaster loan, which does require repayment.

2.1. Understanding FEMA Grants

FEMA grants are designed to help individuals and families recover from disasters without the burden of additional debt.

2.1.1. Types of FEMA Grants Available

FEMA offers several types of grants, each designed to cover specific needs:

- Housing Assistance: Provides funds for temporary housing, rental assistance, and necessary home repairs.

- Other Needs Assistance (ONA): Covers essential personal property, medical expenses, dental expenses, and other disaster-related needs not covered by insurance.

- Disaster Unemployment Assistance (DUA): Provides unemployment benefits to individuals who lost their jobs due to the disaster.

2.1.2. Key Features of FEMA Grants

FEMA grants have several key features that make them beneficial for disaster survivors:

- No Repayment Required: The funds do not need to be paid back.

- Tax-Free: FEMA grants are not considered taxable income.

- Specific Use: The funds must be used for disaster-related expenses as outlined by FEMA.

2.2. SBA Disaster Loans: A Closer Look

While FEMA provides grants, the Small Business Administration (SBA) offers disaster loans, which are a different form of assistance.

2.2.1. Types of SBA Disaster Loans

The SBA offers several types of disaster loans:

- Home Disaster Loans: Help homeowners repair or replace damaged property.

- Business Physical Disaster Loans: Assist businesses in repairing or replacing physical assets.

- Economic Injury Disaster Loans (EIDL): Provide financial assistance to businesses that have suffered economic losses due to the disaster.

2.2.2. When FEMA Refers You to the SBA

FEMA may refer you to the SBA for a disaster loan if:

- Your Damage Exceeds Grant Limits: The damage to your property is significant, and the FEMA grant is not sufficient to cover all necessary repairs.

- You Need Long-Term Recovery Assistance: You require assistance beyond immediate needs, such as rebuilding your home or business.

- You Are a Business Owner: Businesses often require loans to recover from disaster-related losses.

2.2.3. Repayment Terms and Interest Rates

SBA disaster loans come with specific repayment terms and interest rates:

- Repayment Terms: Typically, loans have terms up to 30 years.

- Interest Rates: Interest rates are usually low and determined by the SBA based on the applicant’s ability to repay.

- Collateral: Loans over $25,000 may require collateral.

2.3. Understanding the Application Process

Navigating the application process for FEMA grants and SBA loans can be challenging.

2.3.1. Applying for FEMA Assistance

To apply for FEMA assistance:

- Register with FEMA: You can register online at DisasterAssistance.gov, by phone, or in person at a disaster recovery center.

- Provide Documentation: You will need to provide proof of identity, residency, and documentation of damages.

- Inspection: FEMA may conduct an inspection of your damaged property.

2.3.2. Applying for SBA Disaster Loans

If referred to the SBA, you will need to apply separately for a disaster loan:

- Complete the Application: Fill out the SBA loan application form.

- Provide Financial Information: Submit financial statements, tax returns, and other relevant documents.

- Credit Check: The SBA will conduct a credit check to assess your ability to repay the loan.

2.4. Tips for Managing Disaster Assistance

Managing disaster assistance effectively can help you maximize your recovery efforts.

2.4.1. Documenting Expenses

Keep detailed records of all disaster-related expenses:

- Receipts: Save all receipts for repairs, replacements, and other expenses.

- Photos: Take photos of the damage before and after repairs.

- Invoices: Keep copies of all invoices and bills.

2.4.2. Avoiding Scams

Be cautious of scams and fraud during the recovery process:

- Verify Credentials: Always verify the credentials of contractors and other service providers.

- Don’t Pay Upfront: Avoid paying large sums of money upfront.

- Report Suspicious Activity: Report any suspicious activity to FEMA or local authorities.

2.4.3. Seeking Additional Support

Don’t hesitate to seek additional support from other organizations:

- Non-Profits: Many non-profit organizations offer disaster relief services.

- Local Charities: Local charities can provide food, clothing, and other essential items.

- Government Agencies: Other government agencies may offer additional assistance programs.

2.5. FEMA’s Ongoing Efforts to Improve Assistance

FEMA is continuously working to improve its disaster assistance programs to better serve affected communities.

2.5.1. Addressing Incomplete or Unclear Guidance

FEMA is aware of the challenges some awardees have faced due to incomplete or unclear guidance. According to a report by the Government Accountability Office (GAO), FEMA is working to develop more comprehensive and consistent guidance for the RLF program. This includes clarifying the responsibilities of awardees in managing and reporting on their revolving loan funds.

2.5.2. Systematic Collection and Evaluation of Information

To better assess the effectiveness of the RLF program, FEMA is developing a process for systematically collecting and evaluating information across all phases of the program. This will help FEMA ensure that the program goals are met in both the short and long term.

2.5.3. Collaborating with Stakeholders

FEMA is collaborating with stakeholders, including state and local governments, to gather feedback and improve the RLF program. This collaborative approach ensures that the program meets the needs of the communities it serves.

Navigating FEMA’s disaster assistance programs can be complex, but understanding the different types of assistance available and how to apply for them is crucial for a successful recovery. At money-central.com, we are committed to providing you with the information and resources you need to manage your finances and rebuild your life after a disaster.

3. Maximizing FEMA Assistance and Financial Recovery

Following a disaster, obtaining and maximizing FEMA assistance is crucial for financial recovery. Here’s a detailed guide on how to navigate the process effectively.

3.1. Preparing for the Application Process

Before applying for FEMA assistance, preparation is key.

3.1.1. Gathering Necessary Documentation

Collect all necessary documents to support your application:

- Proof of Identity: Driver’s license, passport, or other government-issued ID.

- Proof of Residency: Utility bills, lease agreements, or mortgage statements.

- Insurance Information: Policies covering your property and belongings.

- Damage Documentation: Photos and videos of the damage, repair estimates, and receipts.

3.1.2. Understanding Eligibility Requirements

Ensure you meet the eligibility requirements for FEMA assistance:

- Disaster Declaration: The disaster must be declared by the President.

- Registration: You must register with FEMA.

- Primary Residence: The damaged property must be your primary residence.

- Insurance Coverage: You must have insurance coverage and report any settlements.

3.2. Navigating the FEMA Application Process

The FEMA application process involves several steps.

3.2.1. Registering with FEMA

Register with FEMA as soon as possible after the disaster:

- Online: Visit DisasterAssistance.gov.

- Phone: Call FEMA’s helpline.

- In Person: Visit a Disaster Recovery Center (DRC).

3.2.2. Completing the Application Form

Fill out the application form accurately and completely:

- Provide Accurate Information: Ensure all information is correct and up-to-date.

- Describe Damages in Detail: Provide a detailed description of the damages to your property.

- Include All Necessary Documents: Attach all required documents to support your application.

3.2.3. FEMA Inspection Process

FEMA may conduct an inspection of your damaged property:

- Schedule the Inspection: Cooperate with FEMA to schedule the inspection.

- Be Present During the Inspection: Be present to answer questions and provide additional information.

- Provide Access: Ensure the inspector has access to all damaged areas.

3.3. Understanding FEMA’s Determination

After reviewing your application, FEMA will make a determination.

3.3.1. Types of FEMA Determinations

FEMA may approve or deny your application:

- Approval: If approved, you will receive a grant for eligible expenses.

- Denial: If denied, you will receive a letter explaining the reasons for the denial.

3.3.2. Appealing a FEMA Decision

If you disagree with FEMA’s decision, you have the right to appeal:

- Submit an Appeal Letter: Write a letter explaining why you disagree with the decision.

- Include Supporting Documentation: Provide any additional documentation to support your appeal.

- Meet the Deadline: Submit your appeal within the specified timeframe.

3.4. Coordinating with Other Assistance Programs

Coordinate with other assistance programs to maximize your recovery:

3.4.1. Insurance Claims

File insurance claims promptly:

- Notify Your Insurer: Contact your insurance company to report the damage.

- Document the Damage: Take photos and videos of the damage for your insurance claim.

- Work with Your Adjuster: Cooperate with your insurance adjuster to assess the damage.

3.4.2. SBA Disaster Loans

Consider applying for an SBA disaster loan:

- Assess Your Needs: Determine if you need additional funds for long-term recovery.

- Apply for a Loan: Complete the SBA loan application.

- Understand the Terms: Review the loan terms and repayment schedule carefully.

3.4.3. Non-Profit and Charitable Organizations

Seek assistance from non-profit and charitable organizations:

- Identify Local Organizations: Find local organizations that provide disaster relief services.

- Apply for Assistance: Apply for assistance from these organizations.

- Coordinate Efforts: Coordinate efforts to avoid duplication of benefits.

3.5. Managing Funds and Preventing Fraud

Manage your disaster assistance funds wisely and protect yourself from fraud.

3.5.1. Creating a Budget

Create a budget to track your disaster-related expenses:

- List All Expenses: List all expenses related to the disaster.

- Prioritize Needs: Prioritize essential expenses.

- Track Spending: Track your spending to ensure you stay within your budget.

3.5.2. Protecting Against Fraud

Protect yourself from fraud and scams:

- Verify Credentials: Verify the credentials of contractors and other service providers.

- Don’t Pay Upfront: Avoid paying large sums of money upfront.

- Report Suspicious Activity: Report any suspicious activity to FEMA or local authorities.

3.6. Long-Term Financial Recovery Strategies

Develop long-term financial recovery strategies to rebuild your financial stability.

3.6.1. Reviewing Your Financial Situation

Assess your overall financial situation:

- Evaluate Assets and Liabilities: Evaluate your assets and liabilities.

- Review Credit Report: Check your credit report for any errors or inaccuracies.

- Identify Financial Goals: Set financial goals for the future.

3.6.2. Creating a Financial Plan

Create a financial plan to guide your recovery:

- Set Realistic Goals: Set realistic financial goals.

- Develop a Savings Plan: Develop a savings plan to rebuild your savings.

- Seek Professional Advice: Seek advice from a financial advisor.

3.6.3. Building a Financial Safety Net

Build a financial safety net to protect yourself from future disasters:

- Emergency Fund: Build an emergency fund to cover unexpected expenses.

- Insurance Coverage: Maintain adequate insurance coverage.

- Disaster Preparedness Plan: Develop a disaster preparedness plan to minimize the impact of future disasters.

Maximizing FEMA assistance and implementing effective financial recovery strategies are essential for rebuilding your life after a disaster. At money-central.com, we are here to provide you with the resources and support you need to navigate this challenging process.

4. Case Studies: Real-Life Examples of FEMA Assistance

Examining real-life examples of FEMA assistance can provide valuable insights into how the program works and its impact on individuals and communities.

4.1. Case Study 1: Housing Assistance After a Hurricane

Background:

- Disaster: Hurricane devastates a coastal community, causing widespread damage to homes.

- Impact: Many residents are displaced and in need of temporary housing.

FEMA Assistance:

- Temporary Housing: FEMA provides temporary housing assistance to displaced residents, including hotel vouchers and rental assistance.

- Home Repair Grants: FEMA provides grants to homeowners to repair their damaged homes, allowing them to return to safe and habitable conditions.

Outcome:

- Immediate Relief: Displaced residents receive immediate relief through temporary housing.

- Long-Term Recovery: Home repair grants enable homeowners to rebuild their homes and return to their community.

4.2. Case Study 2: Small Business Recovery After a Flood

Background:

- Disaster: Severe flooding impacts a downtown area, causing significant damage to small businesses.

- Impact: Many businesses are forced to close, resulting in job losses and economic hardship.

FEMA Assistance:

- SBA Disaster Loans: FEMA refers business owners to the SBA for disaster loans to repair or replace damaged property and equipment.

- Economic Injury Disaster Loans (EIDL): The SBA provides EIDLs to help businesses cover operating expenses and other financial obligations.

Outcome:

- Business Recovery: SBA loans enable businesses to repair and reopen, restoring jobs and economic activity.

- Community Resilience: The recovery of small businesses contributes to the overall resilience of the community.

4.3. Case Study 3: Individual Assistance After a Wildfire

Background:

- Disaster: A destructive wildfire sweeps through a rural area, destroying homes and personal property.

- Impact: Residents lose their homes, belongings, and sense of security.

FEMA Assistance:

- Individual Assistance Grants: FEMA provides grants to individuals and families to cover essential needs, such as clothing, household items, and medical expenses.

- Crisis Counseling: FEMA offers crisis counseling services to help survivors cope with the emotional trauma of the disaster.

Outcome:

- Essential Needs Met: Individuals receive assistance to meet their immediate needs.

- Emotional Support: Crisis counseling helps survivors cope with the emotional impact of the disaster.

4.4. Case Study 4: Public Assistance for Infrastructure Repair

Background:

- Disaster: A major earthquake damages critical infrastructure, including roads, bridges, and utilities.

- Impact: The community faces significant challenges in accessing essential services and resources.

FEMA Assistance:

- Public Assistance Grants: FEMA provides grants to state and local governments to repair or replace damaged infrastructure.

- Emergency Protective Measures: FEMA reimburses costs for emergency protective measures, such as debris removal and temporary repairs.

Outcome:

- Infrastructure Restoration: FEMA grants enable the repair and restoration of critical infrastructure.

- Community Recovery: The restoration of infrastructure supports the overall recovery of the community.

4.5. Case Study 5: Mitigation Projects Funded by the RLF Program

Background:

- Disaster: A coastal community faces repeated flooding, causing damage to homes and businesses.

- Impact: The community seeks to implement mitigation projects to reduce the risk of future flooding.

FEMA Assistance:

- Safeguarding Tomorrow Revolving Loan Fund (RLF): The community receives a loan from the RLF program to fund the construction of flood control measures, such as levees and drainage systems.

Outcome:

- Reduced Flood Risk: The mitigation projects reduce the risk of future flooding, protecting homes and businesses.

- Community Resilience: The community becomes more resilient to future disasters.

These case studies illustrate the diverse ways in which FEMA assistance can support individuals, businesses, and communities in recovering from disasters. By understanding these real-life examples, you can better navigate the FEMA application process and maximize your recovery efforts.

5. Common Misconceptions About FEMA Assistance

There are several common misconceptions about FEMA assistance that can lead to confusion and frustration. Let’s clarify some of these myths.

5.1. Myth: FEMA Covers All Disaster-Related Losses

Reality: FEMA assistance is not designed to cover all disaster-related losses. It is intended to provide basic needs and help jumpstart the recovery process. FEMA typically covers essential expenses like housing, medical care, and personal property replacement, but it may not cover all damages or losses.

5.2. Myth: You Don’t Need Insurance if FEMA is Available

Reality: Insurance is crucial, even when FEMA is available. FEMA assistance is often limited and may not cover all your losses. Insurance can provide more comprehensive coverage and help you recover more fully from a disaster. FEMA requires applicants to file insurance claims first before receiving assistance.

5.3. Myth: FEMA Assistance is Taxable Income

Reality: FEMA assistance is not considered taxable income. Grants and other forms of assistance provided by FEMA are tax-free, meaning you don’t have to report them on your tax return.

5.4. Myth: Only Homeowners Can Receive FEMA Assistance

Reality: Both homeowners and renters can receive FEMA assistance. Renters may be eligible for assistance to cover expenses like temporary housing, personal property replacement, and other disaster-related needs.

5.5. Myth: Applying for FEMA Assistance Will Affect Your Social Security Benefits

Reality: Applying for FEMA assistance will not affect your Social Security benefits or other government benefits. FEMA assistance is separate from these programs and does not impact your eligibility for them.

5.6. Myth: FEMA Assistance is Available for Any Type of Disaster

Reality: FEMA assistance is only available for disasters that have been declared by the President. A disaster declaration triggers FEMA’s ability to provide assistance to affected individuals and communities.

5.7. Myth: If You Are Denied Assistance, There is Nothing You Can Do

Reality: If you are denied FEMA assistance, you have the right to appeal the decision. You can submit an appeal letter explaining why you disagree with the decision and provide any additional documentation to support your case.

5.8. Myth: FEMA Assistance is Only for Low-Income Individuals

Reality: FEMA assistance is available to anyone who meets the eligibility requirements, regardless of income. FEMA’s primary focus is on providing assistance to those who have suffered losses due to a disaster, regardless of their financial situation.

5.9. Myth: FEMA Will Pay Contractors Directly to Repair Your Home

Reality: FEMA does not pay contractors directly. FEMA provides assistance to individuals and families, who are then responsible for hiring contractors and managing the repair process. It’s crucial to verify the credentials of contractors and ensure they are licensed and insured.

5.10. Myth: FEMA Assistance is Unlimited

Reality: FEMA assistance is not unlimited. There are limits to the amount of assistance you can receive, and FEMA may not cover all your losses. It’s essential to understand the scope of FEMA’s assistance and coordinate with other resources to maximize your recovery efforts.

Clearing up these common misconceptions about FEMA assistance can help you navigate the disaster recovery process more effectively and avoid unnecessary confusion. At money-central.com, we are committed to providing you with accurate information and resources to help you make informed decisions during this challenging time.

6. Navigating FEMA’s Future: Innovations and Improvements

FEMA is continuously evolving and innovating to improve its disaster assistance programs and better serve communities in need. Understanding these future directions can help you anticipate changes and plan for your recovery.

6.1. Enhancing Technology and Communication

FEMA is investing in technology and communication tools to streamline the application process and improve communication with disaster survivors:

6.1.1. Online Application Portal

FEMA is enhancing its online application portal to make it more user-friendly and accessible. This includes features like mobile-friendly design, multilingual support, and real-time application status updates.

6.1.2. Mobile App

FEMA is developing a mobile app to provide disaster survivors with access to information, resources, and assistance on their smartphones. The app will include features like real-time alerts, damage reporting tools, and a directory of local resources.

6.1.3. Social Media Engagement

FEMA is increasing its engagement on social media platforms to disseminate information, answer questions, and combat misinformation during disasters.

6.2. Improving Coordination and Collaboration

FEMA is working to improve coordination and collaboration with other federal agencies, state and local governments, and non-profit organizations:

6.2.1. Interagency Coordination

FEMA is strengthening its partnerships with other federal agencies, such as the Small Business Administration (SBA) and the Department of Housing and Urban Development (HUD), to provide a more coordinated and comprehensive response to disasters.

6.2.2. State and Local Partnerships

FEMA is working closely with state and local governments to develop disaster preparedness plans, conduct training exercises, and improve response capabilities.

6.2.3. Non-Profit Partnerships

FEMA is collaborating with non-profit organizations to provide disaster relief services, such as food, shelter, and counseling, to affected communities.

6.3. Investing in Mitigation and Resilience

FEMA is prioritizing investments in mitigation and resilience to reduce the impact of future disasters:

6.3.1. Hazard Mitigation Grants

FEMA provides hazard mitigation grants to state and local governments to fund projects that reduce the risk of damage from natural disasters, such as flood control measures and earthquake retrofitting.

6.3.2. Building Codes and Standards

FEMA is promoting the adoption of stronger building codes and standards to ensure that new construction is more resilient to disasters.

6.3.3. Community Resilience Programs

FEMA is supporting community resilience programs that help communities prepare for, respond to, and recover from disasters.

6.4. Addressing Equity and Accessibility

FEMA is committed to addressing equity and accessibility issues to ensure that all disaster survivors have equal access to assistance:

6.4.1. Language Access

FEMA is providing language access services to ensure that non-English speakers can access information and assistance in their native language.

6.4.2. Accessibility for People with Disabilities

FEMA is working to ensure that its programs and services are accessible to people with disabilities, including providing accommodations and assistive technology.

6.4.3. Outreach to Underserved Communities

FEMA is conducting outreach to underserved communities to raise awareness of disaster assistance programs and help them prepare for disasters.

6.5. Strengthening the Workforce

FEMA is investing in its workforce to ensure that it has the skills and expertise needed to respond to disasters effectively:

6.5.1. Training and Development

FEMA provides training and development opportunities for its employees to enhance their skills and knowledge.

6.5.2. Recruitment and Retention

FEMA is working to recruit and retain a diverse and talented workforce to meet the challenges of disaster management.

6.5.3. Employee Wellness

FEMA is promoting employee wellness to ensure that its employees are healthy and resilient.

By staying informed about these future directions, you can better understand how FEMA is evolving to meet the changing needs of disaster-affected communities and plan for your recovery.

7. FEMA and the Safeguarding Tomorrow Revolving Loan Fund (RLF) Program

The Safeguarding Tomorrow Revolving Loan Fund (RLF) program, administered by FEMA, represents a significant step forward in hazard mitigation funding. Let’s explore this program in detail.

7.1. Overview of the RLF Program

The RLF program provides capitalization grants to eligible states, territories, tribes, and the District of Columbia to establish revolving loan funds for hazard mitigation assistance.

7.1.1. Purpose and Goals

The primary purpose of the RLF program is to provide a sustainable source of funding for hazard mitigation projects. The goals of the program include:

- Reducing community risks from natural disasters

- Promoting resilience and sustainability

- Supporting economic development

- Encouraging innovation in hazard mitigation

7.1.2. How the RLF Program Works

The RLF program operates through a revolving loan fund model:

- Capitalization Grants: FEMA provides capitalization grants to eligible entities.

- Revolving Loan Funds: The entities establish revolving loan funds that issue loans to localities for hazard mitigation projects.

- Loan Repayments: As the loans are repaid, the funds are recycled to finance additional projects.

7.2. Eligibility and Application Process

To participate in the RLF program, states and other eligible entities must apply to FEMA for capitalization grants.

7.2.1. Eligibility Requirements

Eligible entities include:

- States

- Territories

- Tribes

- The District of Columbia

7.2.2. Application Process

The application process involves several steps:

- Notice of Funding Opportunity (NOFO): FEMA publishes a NOFO announcing the availability of funding and providing guidance on how to apply.

- Application Submission: Applicants submit a proposal outlining their plans for establishing and managing a revolving loan fund.

- Project Identification: Applicants identify potential projects that could be funded through the RLF program.

- FEMA Review: FEMA reviews the applications and selects awardees based on their ability to effectively manage and administer the revolving loan funds.

7.3. Project Selection and Implementation

Awardees are responsible for selecting projects to fund through their revolving loan funds.

7.3.1. Project Selection Criteria

Awardees use a variety of criteria to select projects, including:

- Risk Reduction: The extent to which the project reduces the risk of damage from natural disasters.

- Cost-Effectiveness: The cost-effectiveness of the project in terms of dollars spent per dollar of damage avoided.

- Community Benefits: The benefits the project provides to the community, such as improved public safety and economic development.

- Sustainability: The long-term sustainability of the project.

7.3.2. Implementation and Monitoring

Awardees are responsible for overseeing the implementation of projects and monitoring their performance.

7.4. Program Guidance and Technical Assistance

FEMA provides program guidance and technical assistance to help awardees manage their revolving loan funds effectively.

7.4.1. Program Guidance

FEMA provides program guidance on various aspects of the RLF program, including:

- Eligible Uses of Funds

- Loan Terms and Conditions

- Reporting Requirements

- Compliance

7.4.2. Technical Assistance

FEMA provides technical assistance to help awardees:

- Develop Loan Fund Management Plans

- Select and Implement Projects

- Comply with Program Requirements

7.5. GAO Findings and Recommendations

The Government Accountability Office (GAO) has conducted reviews of the RLF program and made recommendations for improvement.

7.5.1. GAO Findings

GAO found that:

- FEMA has developed some RLF program and policy guidance and technical assistance for program participants.

- The guidance was incomplete, unclear, and inconsistent.

- FEMA does not have a process for systematically collecting and evaluating information to assess program effectiveness across all phases of the program.

7.5.2. GAO Recommendations

GAO recommended that FEMA:

- Develop complete, clear, and consistent guidance for the RLF program.

- Document and implement a process to regularly assess RLF program effectiveness.

7.6. Future of the RLF Program

The RLF program has the potential to play a significant role in helping communities build resilience to natural disasters. As FEMA continues to refine the program and address the challenges identified by GAO, the RLF program is poised to become an even more effective tool for hazard mitigation.

8. Expert Advice on Financial Planning After a Disaster

Financial planning after a disaster can be overwhelming. Here is some expert advice to help you navigate this challenging time.

8.1. Assess Your Financial Situation

The first step in financial planning after a disaster is to assess your current financial situation.

8.1.1. Review Your Assets and Liabilities

Take stock of your assets and liabilities:

- Assets: List all your assets, including cash, savings, investments, and property.

- Liabilities: List all your debts, including mortgages, loans, and credit card balances.

8.1.2. Evaluate Your Insurance Coverage

Review your insurance policies to understand what is covered:

- Homeowners Insurance: Check your policy for coverage of damage to your home and personal property.

- Flood Insurance: If you live in a flood zone, check your flood insurance policy for coverage of flood damage.

- Auto Insurance: Check your auto insurance policy for coverage of damage to your vehicle.

8.1.3. Understand Your FEMA Eligibility

Understand your eligibility for FEMA assistance:

- Registration: Register with FEMA to determine your eligibility for assistance.

- Documentation: Gather the necessary documentation to support your application.

8.2. Create a Budget

Creating a budget is essential for managing your finances after a disaster.

8.2.1. List Your Income and Expenses

List all your sources of income and expenses:

- Income: List all sources of income, including wages, salaries, and government benefits.

- Expenses: List all expenses, including housing, food, transportation, and utilities.

8.2.2. Prioritize Essential Expenses

Prioritize essential expenses:

- Housing: Ensure you have safe and stable housing.

- Food: Ensure you have access to nutritious food.

- Transportation: Ensure you have transportation to work and other essential activities.

8.2.3. Track Your Spending

Track your spending to stay within your budget:

- Use a Budgeting App: Use a budgeting app to track your spending and identify areas where you can save money.

- Keep Receipts: Keep receipts for all your expenses to track your spending accurately.

8.3. Manage Your Debt

Managing your debt is crucial for maintaining your financial stability after a disaster.

8.3.1. Contact Your Creditors

Contact your creditors to discuss your situation:

- Mortgage Lender: Contact your mortgage lender to discuss options for forbearance or loan modification.

- Credit Card Companies: Contact your credit card companies to discuss options for reducing your interest rates or suspending payments.

- Loan Providers: Contact your loan providers to discuss options for deferring payments or refinancing your loans.

8.3.2. Prioritize High-Interest Debt

Prioritize paying off high-interest debt:

- Credit Cards: Pay off credit card balances with high interest rates as quickly as possible.

- Personal Loans: Pay off personal loans with high interest rates as quickly as possible.

8.3.3. Avoid Taking on New Debt

Avoid taking on new debt:

- Limit Credit Card Use: Limit your use of credit cards to essential purchases.

- **Avoid Pay