Want to get rich?

The conventional wisdom often points towards simply buying a diverse set of income-producing assets. While straightforward in theory, the challenge lies in pinpointing the right income-producing assets for your portfolio.

Many investors limit themselves to stocks and bonds, understandable given their popularity and effectiveness in wealth accumulation. However, these are merely the entry points to a vast investment universe. For those truly committed to wealth growth, exploring the full spectrum of investment opportunities is crucial.

This article presents 9 exceptional assets for building wealth, extending beyond the usual stocks and bonds. It’s important to note this is a starting point for your personal research, not financial advice. As a money expert at money-central.com, I understand that individual circumstances vary greatly, and the suitability of each asset class depends on your unique situation.

Personally, I incorporate 4 of these 9 asset classes into my portfolio, as some are not currently aligned with my financial strategy. Thorough evaluation of each asset class is recommended before making any portfolio adjustments.

Let’s begin with the cornerstone of many portfolios…

1. Stocks/Equities: The Foundation of Money Building Assets

If I were to select a single, dominant asset class, stocks would be my choice. Representing equity (ownership) in businesses, stocks are a proven and reliable avenue for long-term wealth creation. Investment literature like Triumph of the Optimists, Stocks for the Long Run, and Wealth, War, & Wisdom consistently highlight the power of equities as wealth building assets.

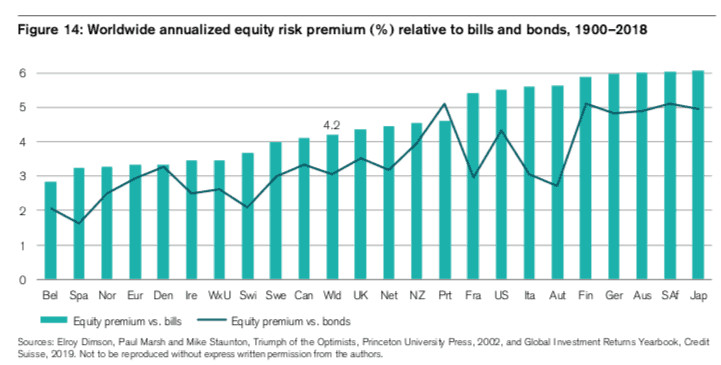

This isn’t limited to U.S. equities. Historical data confirms that stocks globally have delivered consistent long-term returns, typically 3%-6% above safer assets like treasury bills.

Worldwide annualized equity risk premium relative to bonds and bills by country from 1900-2018

Worldwide annualized equity risk premium relative to bonds and bills by country from 1900-2018

Alt text: Chart showing global equity risk premiums compared to bonds and bills from 1900-2018, illustrating the historical performance of stocks as money building assets across different countries.

While past performance doesn’t guarantee future returns, the historical strength of equities as Money Building Assets is compelling. Furthermore, stocks offer a significant advantage: minimal ongoing maintenance. As a shareholder, you benefit from business profits while professional management handles day-to-day operations.

How to invest in stocks? Individual stock picking is generally discouraged for most investors. Instead, broad diversification through funds is recommended. An S&P 500 index fund provides exposure to U.S. equities, while a Total World Stock Index Fund offers global equity diversification.

Investment strategies within stocks vary. Some favor size (small-cap stocks), others valuation (value stocks), and some price trends (momentum stocks). Dividend-paying stocks are also popular, offering regular income payouts from company profits. Dividends are direct distributions of a company’s earnings to its shareholders. For example, owning 5% of a company distributing $1 million in dividends would yield $50,000 for you.

Regardless of your specific stock strategy, including equities in your portfolio is essential for long-term wealth building. My personal approach involves U.S., developed market, and emerging market stocks through diverse ETFs, with some allocation to smaller, value-oriented stocks. While not necessarily optimal, this strategy aligns with my risk tolerance and long-term financial goals.

However, it’s crucial to acknowledge the inherent volatility of stocks. As previously noted, significant market downturns are a part of equity investing:

Expect to see a 50%+ stock market decline a couple of times per century, a 30% decline roughly every 4-5 years, and a 10% correction at least every other year.

This volatility can be emotionally challenging, especially when market sentiment shifts independent of underlying business fundamentals. Witnessing substantial portfolio value erosion can be unsettling, even for experienced investors.

The key to navigating stock market volatility is a long-term perspective. While no investment guarantees returns (consider Japan’s lost decades), history suggests that time is a stock investor’s ally, making stocks powerful money building assets over the long run.

Stocks/Equities Summary for Money Building Assets

- Average Compounded Annual Return: 6%-10%

- Pros: Historically high returns; easy to buy and sell; low maintenance.

- Cons: High volatility; valuations susceptible to sentiment shifts.

2. Bonds: Balancing Risk in Your Asset Portfolio

Transitioning from the dynamic world of stocks, bonds offer a more stable and predictable investment option.

Bonds represent loans from investors to borrowers (governments, corporations, or municipalities). The borrower agrees to repay the principal over a defined period (maturity), often with periodic interest payments (coupons) throughout the loan term.

Government bonds, particularly U.S. Treasury bonds, are frequently discussed in investment contexts. U.S. Treasuries are categorized by maturity:

- Treasury bills: 1-12 months maturity

- Treasury notes: 2-10 years maturity

- Treasury bonds: 10-30 years maturity

Current interest rates for U.S. Treasury bonds across different maturities are readily available online. Choosing between short-term, medium-term, or long-term Treasury bonds depends on your investment strategy and risk tolerance.

Beyond U.S. Treasuries, options include foreign government bonds, corporate bonds, and municipal bonds. These typically offer higher interest rates but come with increased risk.

The higher risk stems from the unmatched creditworthiness of the U.S. Treasury. The U.S. government’s ability to print currency effectively guarantees repayment, a security not always present with other borrowers.

My personal bond portfolio primarily consists of U.S. Treasury bonds. I view bonds not primarily for high returns, but for their crucial portfolio balancing properties. Bonds, especially Treasuries, as money building assets, offer:

- Countercyclical behavior: Tend to appreciate when stocks and other riskier assets decline.

- “Dry powder” for rebalancing: Provide liquid assets to re-invest when riskier assets are down.

- Consistent income stream: Offer more predictable income compared to volatile assets.

Bonds exhibit lower volatility than stocks, providing stability during market turbulence. During the 2020 coronavirus crash, portfolios with a higher allocation to bonds (especially Treasuries) demonstrated greater resilience.

Alt text: Chart comparing the performance of different portfolio allocations (Permanent, 60/40, 80/20, and S&P 500) during the 2020 market crash, highlighting the stabilizing role of bonds in asset portfolios.

Rebalancing during market downturns, facilitated by bond holdings, can significantly enhance long-term returns. My Treasury bond allocation enabled me to rebalance at the 2020 market bottom, a move driven by strategy, not just luck.

Investing in bonds is most easily done through bond funds. While direct individual bond purchases are possible, bond funds offer greater convenience and diversification. Concerns about differences between individual bonds and bond funds are largely unfounded.

Bonds play a vital role beyond just growth in a portfolio. As the saying goes:

We buy stocks so we can eat well, but we buy bonds so we can sleep well.

Bonds Summary for Money Building Assets

- Average Compounded Annual Return: 2%-4%

- Pros: Lower volatility; ideal for rebalancing; principal safety.

- Cons: Lower returns; less attractive income in low-interest rate environments.

3. Investment/Vacation Properties: Tangible Wealth Building Assets

Moving beyond traditional financial instruments, investment or vacation properties offer a popular avenue for wealth building.

These properties provide dual benefits: personal enjoyment and income generation. Effective property management allows rental income to offset mortgage costs while benefiting from long-term property value appreciation. Leverage through mortgage financing can further amplify returns.

However, the allure of vacation rentals comes with responsibilities. Managing renters, property listings, maintenance, and the financial obligations of a mortgage demand significant effort. The perceived “passive income” can quickly become active management.

While returns from investment properties can exceed stocks and bonds, they require considerably more active involvement. For investors seeking greater control and the tangible nature of real estate, investment/vacation properties can be valuable money building assets.

However, market downturns, like the 2020 pandemic, can severely impact vacation rental income, highlighting the risks involved.

Investment/Vacation Property Summary for Money Building Assets

- Average Compounded Annual Return: 12%-15% (highly variable based on specific circumstances)

- Pros: Higher potential returns, especially with leverage; tangible asset.

- Cons: Demanding property and tenant management; lower diversification.

4. Real Estate Investment Trusts (REITs): Passive Real Estate Exposure

For those attracted to real estate but averse to direct management, Real Estate Investment Trusts (REITs) offer a compelling alternative. REITs are companies that own and manage income-generating real estate and distribute profits to shareholders. A legal mandate requires REITs to distribute at least 90% of their taxable income as dividends, making them reliable income-producing assets.

REITs are diverse, encompassing residential (apartments, student housing, etc.) and commercial (office buildings, retail spaces, etc.) properties. They are categorized as:

- Publicly-traded REITs: Listed on stock exchanges, accessible to all investors. Broad stock index funds often include publicly-traded REITs, making direct REIT investment necessary only for increased real estate exposure. REIT index funds offer diversified exposure to publicly-traded REITs.

- Private REITs: Not exchange-traded, available primarily to accredited investors (high net worth or income). Typically involve brokers, potentially higher fees, less regulatory oversight, lower liquidity, but potentially higher returns.

- Publicly non-traded REITs: Not exchange-traded, but open to public investors. More regulated than private REITs, may have investment minimums, lower liquidity, but potentially higher returns than publicly traded REITs.

While I personally prefer publicly-traded REIT index funds, platforms like Fundrise offer non-traded REIT alternatives potentially yielding higher long-term returns. Further research into publicly-traded versus non-traded REITs is recommended.

REITs generally exhibit stock-like returns, often with slightly lower correlation (0.5-0.7) during favorable market conditions. However, during stock market crashes, publicly-traded REITs tend to decline alongside stocks, limiting diversification benefits in downturns.

REITs Summary for Money Building Assets

- Average Compounded Annual Return: 10%-12%

- Pros: Real estate exposure without management responsibilities.

- Cons: Higher volatility; lower liquidity in non-traded REITs; correlation with stocks during market downturns.

5. Farmland: A Historically Stable Asset for Wealth Building

Beyond real estate, farmland represents another historically significant asset for building wealth. Its low correlation with stocks and bonds is a key advantage, as farm income is largely independent of financial market fluctuations.

Farmland also offers lower volatility than stocks and serves as an inflation hedge. Its inherent value makes it less susceptible to complete value loss compared to individual stocks or bonds. However, long-term climate change impacts must be considered.

Farmland returns are projected to be in the high single digits, with roughly half from farm yields and half from land appreciation, according to experts like Jay Girotto.

Investing in farmland can be done through publicly-traded REITs or crowdsourced platforms like FarmTogether and FarmFundr. Crowdsourcing offers more control over specific farmland investments.

However, crowdsourced farmland platforms are typically limited to accredited investors and may involve higher fees. For example, FarmTogether charges a 1% initial investment fee and a 1% ongoing management fee. FarmFundr structures deals with equity stakes or management and sponsor fees. While these fees reflect the complexity of farmland investment, they are a factor to consider.

Farmland Summary for Money Building Assets

- Average Compounded Annual Return: 7%-9%

- Pros: Low correlation with stocks; inflation hedge; lower downside risk.

- Cons: Lower liquidity; potentially higher fees; accredited investor requirement for some platforms.

6. Small Businesses/Franchises/Angel Investing: High-Growth Potential Assets

Venturing into small businesses offers another avenue for building wealth, either through direct ownership and operation or through investment.

Owner + Operator: Running a small business or franchise demands significant dedication. The operational complexity is often underestimated. While potentially highly rewarding, it’s a hands-on, labor-intensive path to wealth building.

Owner Only (Angel Investing): Angel investing, or passive ownership in small businesses, can yield substantial returns. Studies indicate average internal rates of return in the 20%-25% range for angel investments.

However, these high average returns are skewed by a high failure rate. Only a small percentage of angel investments generate positive returns. Success in angel investing often relies on identifying and investing in the rare high-growth companies.

Angel investing is also time-intensive, requiring network building and deal sourcing to access promising opportunities. It’s not a passive side activity for casual investors seeking significant returns.

Platforms like Microventures provide retail investor access to small business investments, with more opportunities for accredited investors. However, accessing the most promising, high-growth startups often requires deeper community involvement and dedicated effort.

Small business investing, therefore, demands more than just capital; it may necessitate a lifestyle shift for those seeking substantial returns.

Small Business Summary for Money Building Assets

- Average Compounded Annual Return: 20%-25%, but with high variability and failure rates.

- Pros: Potential for extremely high returns; increased opportunities with greater involvement.

- Cons: Significant time commitment; high failure rate; can be discouraging.

7. CDs/Money Market Funds: Low-Risk, Stable Income Assets

Certificates of Deposit (CDs) and money market funds offer low-risk avenues for generating steady income.

CDs are time-deposit accounts offered by banks and credit unions. They provide a fixed interest rate for a fixed term (e.g., 6 months, 1 year, 5 years). CDs typically offer higher interest rates than savings accounts but restrict access to funds during the term.

Money market funds are mutual funds investing in short-term debt securities. They aim to maintain a stable $1 share value, appealing to risk-averse investors seeking short-term, liquid investments. Money market funds generally offer lower yields than CDs but higher yields than traditional savings accounts.

While CDs and money market accounts are FDIC-insured (up to $250,000 per depositor per insured bank), money market funds lack this protection. Money market funds are investment products and are not insured against loss.

CDs and money market funds are suitable for investors prioritizing steady income and low risk. However, their returns are generally lower than most other assets on this list.

CDs/Money Market Summary for Money Building Assets

- Average Compounded Annual Return: 1%-3%

- Pros: Lower risk than bonds for similar returns; principal safety.

- Cons: Lower returns; low income in low-interest rate environments.

8. Royalties: Investing in Culture for Income

For investors seeking alternatives to lending, royalties offer a culturally-linked income stream. Platforms like RoyaltyExchange facilitate buying and selling royalties from music, film, and trademarks. Royalties can provide income uncorrelated with financial markets.

For example, Jay-Z and Alicia Keys’ “Empire State of Mind” generated significant royalties. Royalties for this song’s next 10 years were recently sold for a price that, based on past earnings, could yield over 11% annually.

However, royalty income is subject to cultural shifts and changing tastes. The enduring popularity of cultural assets is uncertain.

RoyaltyExchange utilizes a “Dollar Age” metric to assess the longevity of royalty streams. Older assets with a longer history of earnings may represent more stable long-term investments, reflecting the Lindy Effect – the idea that longevity predicts future relevance.

Fees are a consideration with royalty investments, particularly for sellers on platforms like RoyaltyExchange, who may face significant selling fees.

Royalties Summary for Money Building Assets

- Average Compounded Annual Return: 5%-20% (variable, depending on the royalty asset)

- Pros: Uncorrelated to traditional financial assets; generally steady income.

- Cons: High seller fees on some platforms; income susceptible to changing tastes.

9. Your Own Products: Creating Assets and Controlling Your Income

Finally, investing in your own products represents a unique and potentially highly rewarding wealth building strategy. Creating digital or physical products offers maximum control over pricing and potential returns. As the product creator, you are the 100% owner.

Products can include ebooks, online courses, information guides, and more. Many individuals have achieved significant income by selling their own products online. Existing audiences (social media, email lists, websites) can be effectively monetized through product sales. Platforms like Shopify and Gumroad simplify online product sales.

The challenge lies in the upfront effort required to create successful products with no guaranteed immediate payoff. However, a successful product can establish a brand and create opportunities for subsequent product development and diversification.

Personal experience with blogging demonstrates this. Initial income streams can evolve from affiliate partnerships to ad sales and freelancing opportunities over time. Building a successful online presence and product portfolio is a long-term endeavor.

Your Own Product(s) Summary for Money Building Assets

- Average Compounded Annual Return: Highly variable, with a fat-tailed distribution (few products generate massive returns, many generate little).

- Pros: Full ownership; personal satisfaction; brand building; high personal leverage.

- Cons: Labor-intensive; no guaranteed payoff.

What About Gold, Crypto, Commodities, Art, Wine, and Other Non-Income Assets?

Certain asset classes, such as gold, cryptocurrency, commodities, art, and wine, were excluded from the primary list because they do not inherently generate income.

While these assets can appreciate in value and contribute to portfolio diversification, they lack a reliable income stream. Their allocation in a portfolio should generally be limited, perhaps to 10%-15%.

Final Summary of Money Building Assets

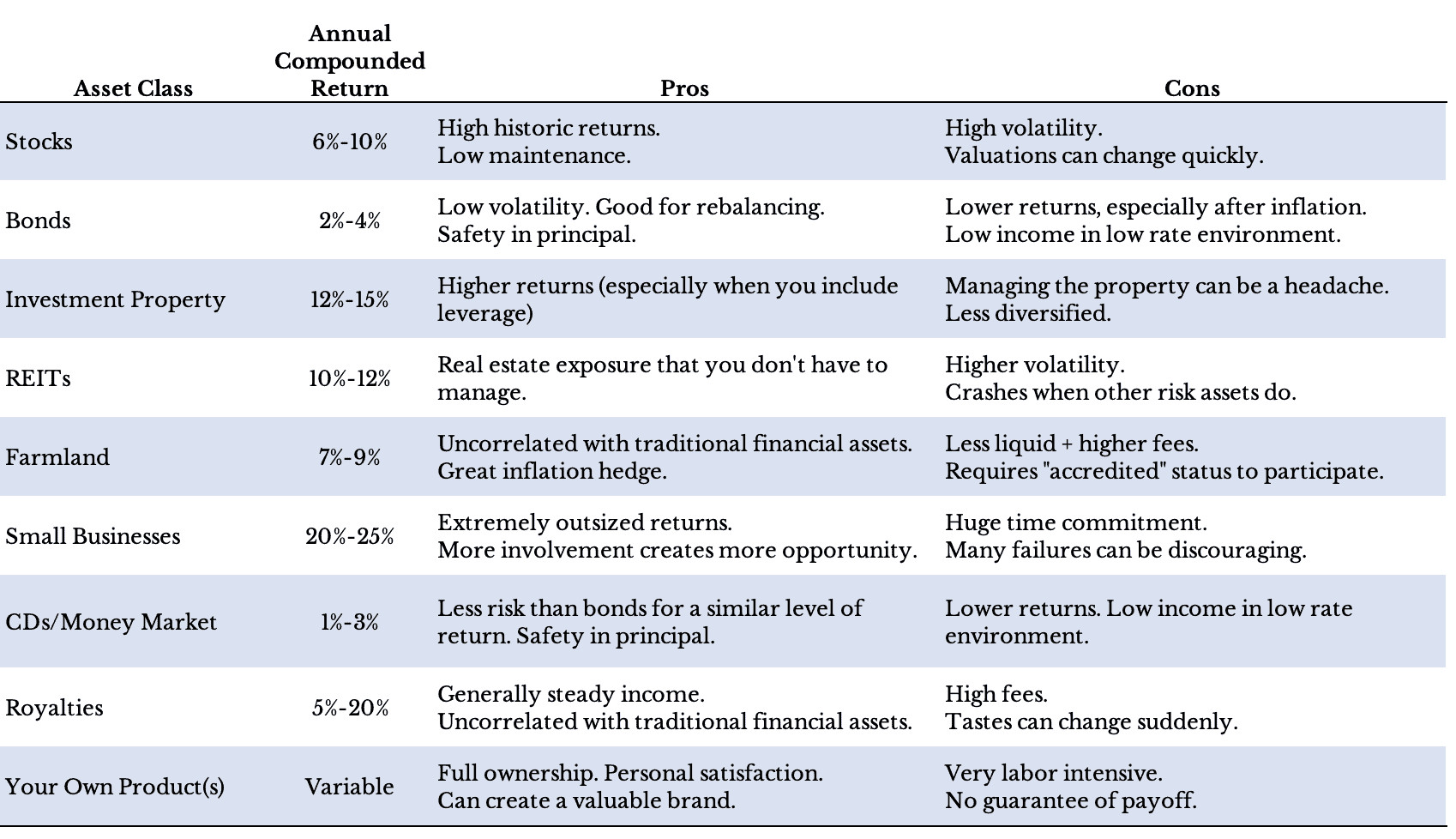

To facilitate comparison, here is a summary table of the 9 income-producing assets:

Summary table of 9 income producing assets, their annual compounded return, and their pros and cons.

Summary table of 9 income producing assets, their annual compounded return, and their pros and cons.

Alt text: Summary table outlining 9 money building assets, their average annual returns, advantages, and disadvantages for investors seeking diverse income streams.

The Bottom Line: Choosing the Right Assets for You

Ultimately, the optimal mix of money building assets is a personal decision. There are multiple paths to investment success. The key is not necessarily identifying the “best” assets, but selecting those that align with your individual circumstances, risk tolerance, and financial goals.

Personal experience has shown that diverse and valid investment strategies exist. Two well-informed individuals can adopt different approaches and both achieve positive outcomes. I wish you success in your investment journey and appreciate you taking the time to read this guide to money building assets.