Understanding the money factor is essential for anyone considering a lease, and at money-central.com, we’re here to help you navigate the complexities of vehicle leasing with confidence by breaking down what constitutes a favorable money factor in 2024, and how it impacts your monthly payments. We’ll clarify how it relates to the annual percentage rate (APR), and provide insights on securing the best possible lease terms. In addition to the money factor, we’ll also explore the importance of residual value, lease term, and other factors that affect the overall cost of your lease.

1. What Is a Money Factor in Leasing?

The money factor, also known as the lease factor or lease rate, is a key component in calculating your monthly lease payment; in essence, it’s the interest rate you’re charged on the vehicle’s depreciated value during the lease term. Think of the money factor as the interest rate you pay on the borrowed portion of the car’s value during the lease.

1.1 Decoding the Money Factor Formula

The money factor is a small decimal number that represents the interest rate. The basic formula for calculating the monthly lease payment includes the money factor:

Monthly Lease Payment = (Depreciation + Rent Charge) + Sales Tax

Where:

- Depreciation = (Capitalized Cost – Residual Value) / Lease Term

- Rent Charge = (Capitalized Cost + Residual Value) * Money Factor

- Sales Tax = (Depreciation + Rent Charge) * Sales Tax Rate

1.2 Money Factor vs. APR: Unveiling the Connection

To understand the money factor better, you can convert it to an annual percentage rate (APR), which is a more familiar way to view interest rates; multiply the money factor by 2,400 to get the approximate APR. For example, a money factor of 0.00125 is equivalent to an APR of 3%.

APR = Money Factor * 2400 Money Factor to APR Conversion

Money Factor to APR Conversion

Alternative text: Conversion formula example from Money Factor to APR

1.3 Factors Influencing the Money Factor

Several factors can influence the money factor offered to you by a leasing company:

- Credit Score: A higher credit score typically results in a lower money factor, as you’re seen as a lower-risk borrower.

- Lease Term: Shorter lease terms might have lower money factors compared to longer terms.

- Vehicle Type: The popularity and depreciation rate of the vehicle can affect the money factor. High-demand vehicles with good residual values may have lower money factors.

- Lender: Different lenders may offer varying money factors based on their internal policies and risk assessment.

- Market Conditions: Economic factors, such as interest rate trends and competition among leasing companies, can influence money factors.

2. What Is Considered a Good Money Factor in 2024?

Determining a “good” money factor depends on prevailing market conditions and your creditworthiness; generally, a lower money factor is always better because it translates to a lower APR and, consequently, lower monthly payments.

2.1 Benchmarking Against Average Rates

To gauge whether a money factor is good, compare it to the average interest rates for car loans or leases in 2024; you can find this information from financial websites, credit unions, or banks. If the APR (calculated from the money factor) is lower than the average, it’s generally a good rate.

Here is a table showing example calculations:

| Money Factor | APR (Money Factor x 2400) | Assessment |

|---|---|---|

| 0.00080 | 1.92% | Excellent |

| 0.00125 | 3.00% | Good |

| 0.00170 | 4.08% | Average |

| 0.00220 | 5.28% | Above Average |

| 0.00270 | 6.48% | Potentially High |

2.2 Factors That Affect What Is Considered a Good Money Factor

- Credit Score: A credit score in the “excellent” range (750+) will typically qualify for the best money factors.

- Market Conditions: Interest rates are constantly fluctuating. Stay informed about current trends to assess whether the offered money factor is competitive.

- Vehicle Residual Value: Vehicles with high residual values (meaning they depreciate less) often have lower money factors because the leasing company anticipates recouping more of the car’s value at the end of the lease.

2.3 How to Negotiate a Lower Money Factor

Negotiating a lower money factor can save you a significant amount of money over the term of your lease. Here are some effective strategies:

- Improve Your Credit Score: Before you start negotiating, check your credit score and address any issues. A higher credit score gives you more leverage.

- Shop Around: Get quotes from multiple dealerships and leasing companies. This allows you to compare offers and use them to negotiate better terms.

- Negotiate the Vehicle Price First: Negotiate the capitalized cost (the vehicle’s price) separately from the money factor. Dealers sometimes inflate the vehicle’s price to offset a lower money factor.

- Be Informed: Research the average money factors for the vehicle you want to lease. Websites like Edmunds and Leasehackr often provide this information.

- Challenge the Money Factor: Politely question the money factor if it seems high compared to market rates. Ask the dealer to justify the rate.

- Consider Multiple Security Deposits (MSDs): Some leasing companies allow you to lower the money factor by paying multiple security deposits upfront. These deposits are typically refundable at the end of the lease.

- Time Your Lease: Lease in months when dealerships are trying to meet quotas (end of the month, quarter, or year). They may be more willing to offer better terms.

- Walk Away: Be prepared to walk away if you’re not satisfied with the offer. This can be a powerful negotiating tactic.

2.4 Red Flags to Watch Out For

- Hidden Fees: Be wary of leasing companies that try to hide fees or inflate other charges to compensate for a seemingly low money factor.

- High Down Payments: A large down payment might lower your monthly payments but can be a waste of money if the car is totaled or stolen.

- Unwillingness to Disclose: If a leasing company is hesitant to disclose the money factor or other lease terms, it could be a sign of dishonesty.

3. Understanding Lease Payments: Beyond the Money Factor

While the money factor is important, it’s not the only factor determining your monthly lease payment.

3.1 Capitalized Cost: What You’re Paying For

The capitalized cost is the agreed-upon value of the vehicle at the start of the lease. It includes the vehicle’s price, taxes, fees, and any add-ons or services you choose to include.

- Negotiating the Capitalized Cost: Just like buying a car, you can negotiate the capitalized cost. Aim to lower this value to reduce your monthly payments.

- Capitalized Cost Reduction: This refers to any down payment, trade-in value, or rebates that reduce the capitalized cost. While a capitalized cost reduction can lower your monthly payments, be cautious about putting too much money down, as you could lose it if the car is totaled.

3.2 Residual Value: The Car’s Worth at Lease End

The residual value is an estimate of the vehicle’s worth at the end of the lease term, expressed as a percentage of the MSRP (Manufacturer’s Suggested Retail Price).

- Impact on Lease Payments: A higher residual value means the car is expected to depreciate less, resulting in lower monthly payments.

- Factors Affecting Residual Value: The vehicle’s make, model, popularity, and the lease term all affect residual value.

3.3 Lease Term: Short vs. Long-Term Leases

The lease term is the length of the lease, typically expressed in months (e.g., 24, 36, or 48 months).

- Shorter Terms: May have lower money factors but higher monthly payments due to faster depreciation.

- Longer Terms: Result in lower monthly payments but may have higher money factors and more overall interest paid over the lease term.

3.4 Other Fees and Charges

Leases often come with various fees and charges, which can significantly impact the overall cost.

- Acquisition Fee: A fee charged by the leasing company to cover the cost of setting up the lease.

- Disposition Fee: A fee charged at the end of the lease to cover the cost of preparing the vehicle for resale.

- Early Termination Fee: A fee charged if you end the lease early.

- Excess Mileage Fee: A fee charged for each mile driven over the agreed-upon mileage limit.

- Excess Wear and Tear Fee: A fee charged for damage to the vehicle beyond normal wear and tear.

4. Real-World Examples of Good Money Factors

Examining real-world scenarios can provide a clearer understanding of what constitutes a good money factor in 2024.

4.1 Example 1: Luxury Sedan Lease

Imagine you are leasing a luxury sedan with an MSRP of $60,000. After negotiation, the capitalized cost is $55,000, and the residual value after 36 months is 55% ($33,000). The money factor offered is 0.00100 (2.4% APR).

- Depreciation: ($55,000 – $33,000) / 36 = $611.11

- Rent Charge: ($55,000 + $33,000) * 0.00100 = $88.00

- Monthly Payment (before tax): $611.11 + $88.00 = $699.11

In this case, a money factor of 0.00100 (2.4% APR) would be considered excellent, especially for a luxury vehicle.

4.2 Example 2: SUV Lease

Consider leasing an SUV with an MSRP of $45,000. The capitalized cost is $42,000, and the residual value after 36 months is 60% ($27,000). The money factor offered is 0.00150 (3.6% APR).

- Depreciation: ($42,000 – $27,000) / 36 = $416.67

- Rent Charge: ($42,000 + $27,000) * 0.00150 = $103.50

- Monthly Payment (before tax): $416.67 + $103.50 = $520.17

A money factor of 0.00150 (3.6% APR) might be considered average to good, depending on your credit score and prevailing market conditions.

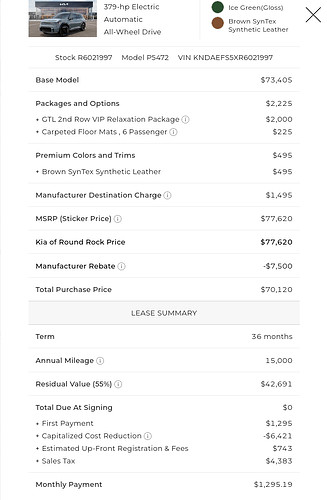

4.3 Case Study: Kia EV9 Lease

The Kia EV9 is a popular electric vehicle, and leasing can be an attractive option due to tax credit incentives. Let’s analyze a hypothetical lease scenario:

- MSRP: $77,620

- Sales Price: $77,620

- Residual Value (55% for 36 months): $42,691

- Money Factor: 0.00269 (6.46% APR)

- Lease Payment: $1,295.19

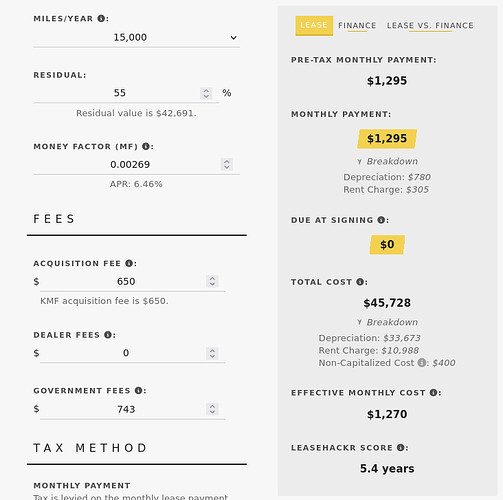

In this scenario, the money factor of 0.00269 (6.46% APR) seems high compared to the interest rate, as this results in substantial finance charges over the lease term. As the initial request mentions, this appears a bit high. The initial request also explores the “zero down” lease, where taxes and fees are financed. Using a Leasehackr calculator, the money factor needed to match the lease payment comes out to 0.00269. This works out to an APR of 6.46%, which is comparable to bank interest rates, as if the vehicle was financed instead.

Total amount financed= $32,555 (3 years of depreciation + taxes and fees)Doing a standard 3-year loan at 6.46%, the payment would be $997.19. To get a payment amount of $1,295 on a 3-year loan of $32,555, the interest rate would need to be about 25%. Therefore, this shows how a money factor of 0.00269 = 6.46% APR results in nearly $11k in finance charges from a $33,500 “loan” over 3 years.

Leasehackr Calculator

Leasehackr Calculator

Alternative text: Leasehackr calculator shows discrepancy between quoted lease payment and money factor for Kia EV9

4.4 Additional Tips for Evaluating Lease Offers

- Compare Total Cost: Don’t focus solely on the monthly payment. Calculate the total cost of the lease, including all fees and charges, to compare offers accurately.

- Read the Fine Print: Understand all the terms and conditions of the lease, including mileage limits, wear and tear policies, and early termination fees.

- Seek Professional Advice: If you’re unsure about any aspect of the lease, consult a financial advisor or leasing expert.

5. How to Find the Best Lease Deals in 2024

Finding the best lease deals requires research, negotiation, and a good understanding of the leasing process.

5.1 Online Resources and Tools

- Lease Comparison Websites: Use websites like Edmunds, Kelley Blue Book, and Leasehackr to research lease deals and compare offers.

- Lease Calculators: Utilize online lease calculators to estimate monthly payments and evaluate the financial implications of different lease terms and money factors.

- Dealer Websites: Check the websites of local dealerships for special lease offers and incentives.

5.2 Timing Your Lease

- End of the Month/Quarter/Year: Dealerships often offer better deals at the end of the month, quarter, or year to meet sales quotas.

- New Model Year Releases: As dealerships clear out old inventory to make room for new models, you may find attractive lease deals on the outgoing models.

- Holiday Sales: Take advantage of holiday sales events, such as Memorial Day, Labor Day, and Black Friday, when dealerships offer special incentives.

5.3 Leveraging Incentives and Rebates

Many manufacturers and dealerships offer incentives and rebates that can lower the cost of your lease.

- Manufacturer Incentives: Check for manufacturer-sponsored lease deals, which may include lower money factors, cash rebates, or special lease terms.

- Federal and State Incentives: Research federal and state incentives for electric vehicles and other fuel-efficient cars, which can be applied to your lease.

- Loyalty Programs: If you’re a repeat customer of a particular brand, you may qualify for loyalty discounts or incentives.

- Affiliate Programs: Some companies offer discounts to their employees through affiliate programs with car manufacturers or dealerships.

5.4 Working with Leasing Brokers

A leasing broker can help you find the best lease deals by leveraging their industry connections and expertise.

- Benefits of Using a Broker: Leasing brokers can save you time and effort by shopping around for the best offers and negotiating on your behalf. They also have access to deals that may not be available to the general public.

- How to Find a Reputable Broker: Look for brokers with a proven track record, positive reviews, and transparent fee structures.

5.5 Staying Informed

- Monitor Interest Rates: Keep an eye on interest rate trends and economic news, which can impact money factors and lease deals.

- Follow Industry News: Stay informed about new vehicle releases, manufacturer incentives, and leasing trends by following automotive industry news and blogs.

6. Common Leasing Mistakes to Avoid

Avoiding common leasing mistakes can save you money and prevent headaches down the road.

6.1 Focusing Solely on the Monthly Payment

- The Trap: Dealers may lower the monthly payment by extending the lease term, increasing the money factor, or adding hidden fees.

- The Solution: Focus on the total cost of the lease, including all fees, charges, and interest, to compare offers accurately.

6.2 Ignoring the Mileage Limit

- The Trap: Exceeding the mileage limit can result in hefty charges at the end of the lease.

- The Solution: Estimate your annual mileage needs accurately and choose a lease with a sufficient mileage allowance. If you anticipate driving more, negotiate a higher mileage limit upfront.

6.3 Neglecting Wear and Tear

- The Trap: Damage to the vehicle beyond normal wear and tear can result in expensive charges at the end of the lease.

- The Solution: Maintain the vehicle properly and address any damage promptly. Consider purchasing a wear and tear protection plan to cover minor damage.

6.4 Skipping the Test Drive

- The Trap: Leasing a car without test-driving it can result in dissatisfaction with the vehicle’s performance, features, or comfort.

- The Solution: Always test-drive the car before committing to a lease to ensure it meets your needs and preferences.

6.5 Failing to Negotiate

- The Trap: Accepting the first offer without negotiation can result in paying more than necessary.

- The Solution: Negotiate the capitalized cost, money factor, and other lease terms to get the best possible deal.

7. The Future of Leasing in 2024 and Beyond

The leasing landscape is constantly evolving, with new trends and technologies shaping the future of car ownership.

7.1 The Rise of Electric Vehicle Leases

Electric vehicles (EVs) are becoming increasingly popular, and leasing can be an attractive option due to tax incentives and rapidly evolving technology.

- Tax Credits: Leasing an EV may allow you to take advantage of federal tax credits that are not available when purchasing.

- Technology Advancements: Leasing allows you to upgrade to the latest EV technology every few years as battery technology and charging infrastructure improve.

7.2 Subscription Services

Car subscription services are emerging as an alternative to traditional leasing, offering flexibility and convenience.

- Benefits of Subscription Services: Subscription services typically include insurance, maintenance, and repairs in the monthly fee, providing a hassle-free car ownership experience.

- Drawbacks of Subscription Services: Subscription services can be more expensive than leasing or buying a car, and they may have limited vehicle options.

7.3 Online Leasing Platforms

Online leasing platforms are making it easier to shop for and secure lease deals from the comfort of your home.

- Convenience: Online platforms allow you to compare offers from multiple dealerships, negotiate prices, and complete the leasing process online.

- Transparency: Online platforms often provide more transparent pricing and lease terms than traditional dealerships.

8. Money-Central.com: Your Partner in Financial Empowerment

At money-central.com, we’re committed to providing you with the information and resources you need to make informed financial decisions; our comprehensive articles, tools, and expert advice can help you navigate the complexities of leasing and achieve your financial goals.

8.1 Explore Our Resources

- Financial Calculators: Use our lease calculators to estimate monthly payments and evaluate different lease scenarios.

- Expert Articles: Browse our library of articles on leasing, car buying, and other financial topics.

- Financial Advice: Get personalized financial advice from our team of experts.

8.2 Stay Connected

- Subscribe to Our Newsletter: Stay up-to-date on the latest financial news, tips, and insights by subscribing to our newsletter.

- Follow Us on Social Media: Connect with us on social media for daily financial tips and inspiration.

8.3 Contact Us

- Address: 44 West Fourth Street, New York, NY 10012, United States

- Phone: +1 (212) 998-0000

- Website: money-central.com

9. FAQs: Understanding the Money Factor

Here are some frequently asked questions to further clarify the concept of the money factor and its impact on leasing:

9.1 What exactly does the money factor represent?

The money factor is a decimal number that represents the interest rate charged on the depreciated value of the vehicle during the lease term. It’s used to calculate the rent charge, which is a component of your monthly lease payment.

9.2 How is the money factor different from the APR?

The money factor is a smaller number that needs to be converted to APR to be easily comparable to interest rates on loans. You can convert the money factor to APR by multiplying it by 2,400.

9.3 Is a lower money factor always better?

Yes, a lower money factor always translates to a lower APR, resulting in lower monthly lease payments and less overall interest paid over the lease term.

9.4 How can I find out the money factor on a lease offer?

Ask the dealer or leasing company to disclose the money factor. They are legally required to provide this information.

9.5 Can I negotiate the money factor?

Yes, you can negotiate the money factor, especially if you have a good credit score and have researched average rates for the vehicle you want to lease.

9.6 What credit score do I need to get a good money factor?

A credit score in the “excellent” range (750+) will typically qualify for the best money factors. However, even with a lower credit score, you may still be able to negotiate a reasonable rate.

9.7 Are money factors the same for all vehicles?

No, money factors can vary depending on the vehicle’s make, model, popularity, and residual value.

9.8 How does the lease term affect the money factor?

Shorter lease terms may have lower money factors, but higher monthly payments due to faster depreciation. Longer lease terms may have higher money factors, but lower monthly payments.

9.9 What other factors should I consider besides the money factor?

In addition to the money factor, consider the capitalized cost, residual value, lease term, fees, and mileage limits to evaluate the overall cost of the lease.

9.10 Where can I find more information about leasing and money factors?

You can find more information about leasing and money factors on websites like money-central.com, Edmunds, Kelley Blue Book, and Leasehackr.

10. Take Control of Your Financial Future

Understanding the money factor is just one step towards taking control of your financial future; by educating yourself, researching your options, and seeking expert advice, you can make informed decisions that align with your financial goals. Whether you’re considering leasing a car, buying a home, or investing for retirement, money-central.com is here to help you every step of the way. Visit our website today to explore our resources and start your journey towards financial empowerment.