Is Social Security running out of money, and what does that mean for you? Yes, Social Security faces financial challenges, but money-central.com is here to break down the complexities and offer clear insights. We’ll explore the reasons behind these challenges and discuss potential solutions to secure your financial future, offering financial security. Stay informed with our expert guidance on social insurance, retirement planning, and government benefits.

1. What’s Happening with Social Security’s Finances?

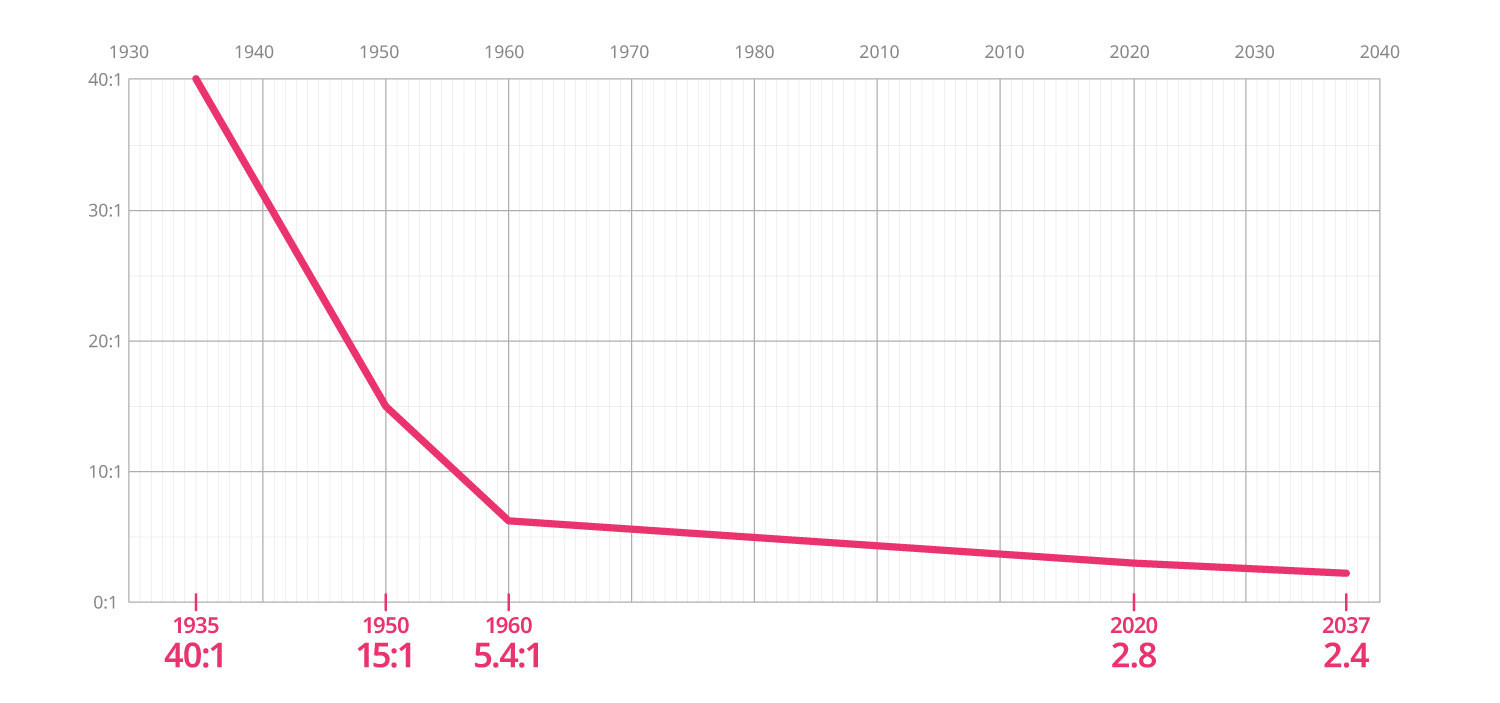

Is Social Security really facing a shortfall? Yes, Social Security is facing a projected shortfall in the coming years. Social Security operates as a “pay-as-you-go” system, where current workers’ payroll taxes fund the benefits of current retirees. Demographic shifts, including declining birth rates and increasing life expectancy, are creating a strain on the system, as fewer workers support a growing number of beneficiaries. This imbalance is projected to lead to the depletion of Social Security’s trust fund reserves in the coming years. According to the Social Security Administration, if no action is taken, the trust fund reserves are projected to be depleted by the mid-2030s.

To understand the situation better, let’s delve into the core mechanisms of Social Security:

- Payroll Taxes: The primary funding source for Social Security is payroll taxes. A percentage of workers’ earnings is deducted and contributed to the Social Security trust funds.

- Trust Funds: Social Security has two trust funds: the Old-Age and Survivors Insurance (OASI) trust fund, which pays retirement and survivor benefits, and the Disability Insurance (DI) trust fund, which pays disability benefits.

- Benefit Payments: Social Security benefits are paid to eligible retirees, survivors, and disabled individuals. The amount of benefits is determined by factors such as earnings history, age at retirement, and family status.

The financial health of Social Security depends on the balance between the inflow of payroll taxes and the outflow of benefit payments. When the inflow exceeds the outflow, the surplus is added to the trust fund reserves. However, when the outflow exceeds the inflow, the trust fund reserves are drawn down to cover the shortfall.

Workers to Beneficiaries Ratio demonstrating social security concerns

Workers to Beneficiaries Ratio demonstrating social security concerns

2. Why Are There Fewer Workers Contributing to Social Security?

Why is the worker-to-beneficiary ratio declining? The decline in the worker-to-beneficiary ratio is primarily due to two key demographic trends: declining birth rates and increasing life expectancy.

-

Declining Birth Rates:

- Historical Context: In the mid-20th century, particularly during the baby boom era (1946-1964), birth rates were significantly higher. The average number of children born per woman was over 3.

- Current Trends: Since then, birth rates have steadily declined. By 2019, the average number of children born per woman had dropped to around 1.7, according to the Social Security Administration.

- Immigration Impact: Immigration has helped to offset some of the decline in the working-age population, but it has not been enough to fully compensate for the drop in birth rates.

-

Rising Life Expectancy:

- Historical Data: In 1940, when Social Security checks were first mailed out, the average life expectancy was about 63.5 years.

- Current Data: By 2019, the average life expectancy had increased to 78.75 years.

- Impact on Benefits: This means that people are now receiving Social Security benefits for a significantly longer period than originally anticipated.

These demographic changes have created a “perfect storm” for Social Security. With fewer workers contributing and more retirees receiving benefits for longer, the system is facing a growing financial strain.

| Factor | 1940 | 2019 | Change |

|---|---|---|---|

| Life Expectancy | 63.5 years | 78.75 years | +15.25 years |

| Birth Rate | Over 3 children/woman | Around 1.7 children/woman | Significant decrease |

3. What Happens When the Social Security Trust Fund Is Depleted?

What will happen to Social Security benefits if the trust fund runs out? If the Social Security trust fund is depleted, it doesn’t mean that benefits will stop entirely, but it does mean that benefits will be reduced. Continuing payroll taxes would still be collected and used to pay benefits, but the amount of benefits that can be paid would be limited to the amount of payroll taxes coming in.

According to the Social Security Administration, if no action is taken to address the shortfall, benefits could be reduced by around 20-25%. This would have a significant impact on retirees and other beneficiaries who rely on Social Security as a major source of income.

The Bipartisan Policy Center estimates that without reform, Social Security could only pay about 80% of promised benefits starting in the mid-2030s. This highlights the urgency of addressing the financial challenges facing Social Security to ensure that benefits can be maintained at current levels.

4. What Are Some Potential Solutions to Save Social Security?

How can we fix Social Security’s funding problems? There are several potential solutions to address the financial challenges facing Social Security. These solutions generally fall into two categories: increasing revenue and reducing benefits. Many experts suggest a combination of both approaches to achieve a balanced and sustainable solution.

-

Increasing Revenue:

- Raising the Payroll Tax Rate: One option is to increase the payroll tax rate, which is currently 12.4% (split equally between employers and employees). Even a small increase in the tax rate could generate significant additional revenue for Social Security.

- Increasing the Taxable Wage Base: Currently, Social Security taxes are only applied to earnings up to a certain limit, known as the taxable wage base. In 2024, this limit is $168,600. Increasing or eliminating the taxable wage base would subject more earnings to Social Security taxes, generating additional revenue.

- Taxing Investment Income: Another option is to tax investment income, such as capital gains and dividends, and dedicate the revenue to Social Security.

- Adjusting the Cost-of-Living Adjustment (COLA): The COLA is an annual adjustment to Social Security benefits to account for inflation. Some proposals suggest using a different measure of inflation, such as the chained CPI, which tends to grow more slowly than the traditional CPI, to reduce the annual COLA.

-

Reducing Benefits:

- Raising the Retirement Age: The full retirement age (FRA) is currently 67 for those born in 1960 or later. Raising the FRA would reduce the number of years that people receive Social Security benefits, lowering the overall cost of the program.

- Reducing Benefit Amounts: Another option is to reduce the amount of benefits that are paid out. This could be done by changing the formula used to calculate benefits or by reducing benefits for certain groups of beneficiaries.

- Means Testing: Some proposals suggest means testing Social Security benefits, which would reduce or eliminate benefits for higher-income individuals.

Each of these solutions has its own advantages and disadvantages, and there is no easy answer. Finding a solution that is both effective and politically feasible will require compromise and leadership from both parties.

5. How Would Raising the Retirement Age Impact Future Retirees?

Would raising the retirement age really solve the problem? Raising the retirement age is one of the proposed solutions to address Social Security’s financial challenges. It would involve increasing the age at which individuals can claim full retirement benefits. While this approach could help reduce the long-term costs of the program, it also has potential implications for future retirees.

-

Potential Benefits of Raising the Retirement Age:

- Reduced Program Costs: By increasing the retirement age, individuals would need to work longer before claiming full benefits, reducing the overall number of years that Social Security pays out benefits.

- Increased Workforce Participation: Raising the retirement age could encourage individuals to remain in the workforce for a longer period, which could boost economic growth and increase tax revenues.

-

Potential Drawbacks of Raising the Retirement Age:

- Impact on Low-Income Workers: Some argue that raising the retirement age would disproportionately affect low-income workers who may have physically demanding jobs and may not be able to work longer.

- Health Concerns: Not everyone can work until an older age due to health issues or disabilities. Raising the retirement age could create challenges for individuals who are unable to work longer but are not yet eligible for full benefits.

- Unemployment Risks: Older workers may face challenges finding employment, and raising the retirement age could exacerbate unemployment rates among older age groups.

The impact of raising the retirement age would depend on various factors, such as the specific age increase, the availability of job opportunities for older workers, and the provision of support for individuals who are unable to work longer due to health or economic reasons.

6. What Role Does Immigration Play in Social Security’s Future?

How does immigration affect the Social Security system? Immigration plays a significant role in Social Security’s financial health. Immigrants contribute to the economy and the Social Security system through payroll taxes and other forms of taxation.

-

Positive Impacts of Immigration on Social Security:

- Increased Workforce: Immigrants add to the labor force, increasing the number of workers who contribute to Social Security through payroll taxes.

- Younger Population: Immigrants tend to be younger than the native-born population, which helps to offset the aging of the U.S. population and improve the worker-to-beneficiary ratio.

- Economic Growth: Immigrants contribute to economic growth by starting businesses, creating jobs, and increasing consumption. This economic growth generates additional tax revenue, which can help to support Social Security.

-

Potential Challenges Related to Immigration:

- Strain on Resources: High levels of immigration can put a strain on resources, such as schools, hospitals, and social services.

- Wage Effects: Some studies suggest that immigration can have a negative impact on the wages of low-skilled workers.

Overall, the impact of immigration on Social Security is complex and depends on various factors, such as the number of immigrants, their skills and education levels, and their integration into the U.S. economy. However, most studies suggest that immigration has a net positive impact on Social Security’s financial health.

According to research from the National Academy of Sciences, in 2016, immigrants contributed $223 billion more to government revenues than they consumed in public services. This surplus helps to support Social Security and other government programs.

7. What Can Younger People Do to Prepare for Potential Social Security Changes?

What should young people do to plan for Social Security’s future? Given the uncertainty surrounding the future of Social Security, it’s important for younger people to take steps to prepare for potential changes. While Social Security may still be a part of their retirement income, relying solely on it may not be sufficient.

-

Start Saving Early:

- Compound Interest: The earlier you start saving, the more time your money has to grow through the power of compound interest.

- Retirement Accounts: Take advantage of tax-advantaged retirement accounts, such as 401(k)s and IRAs, to save for retirement.

- Employer Matching: If your employer offers a 401(k) match, be sure to contribute enough to take full advantage of it.

-

Diversify Investments:

- Asset Allocation: Diversify your investments across different asset classes, such as stocks, bonds, and real estate, to reduce risk.

- Long-Term Growth: Focus on investments that have the potential for long-term growth, such as stocks.

-

Consider Alternative Retirement Plans:

- Annuities: Annuities can provide a guaranteed stream of income in retirement.

- Real Estate: Investing in real estate can provide rental income and potential appreciation.

-

Stay Informed:

- Social Security Updates: Stay informed about potential changes to Social Security and how they may affect you.

- Financial Planning: Seek advice from a qualified financial advisor to develop a personalized retirement plan.

-

Increase Earning Potential:

- Education and Skills: Invest in your education and skills to increase your earning potential throughout your career.

- Career Development: Seek opportunities for career advancement and professional development.

By taking these steps, younger people can increase their financial security and reduce their reliance on Social Security in retirement.

8. How Does Social Security Affect Different Income Groups?

How does Social Security impact different income levels? Social Security has different effects on various income groups due to its progressive benefit structure. While it provides a safety net for lower-income individuals, it also serves as a significant source of retirement income for middle- and upper-income earners.

-

Lower-Income Individuals:

- Safety Net: Social Security provides a crucial safety net for lower-income individuals who may have limited savings and other retirement resources.

- Higher Replacement Rate: Social Security replaces a higher percentage of pre-retirement earnings for lower-income individuals compared to higher-income individuals.

- Poverty Reduction: Social Security helps to reduce poverty among seniors, particularly those with limited income and assets.

-

Middle-Income Individuals:

- Significant Income Source: Social Security serves as a significant source of retirement income for middle-income individuals, supplementing their savings and pensions.

- Adequate Replacement Rate: Social Security replaces an adequate percentage of pre-retirement earnings for middle-income individuals, helping them maintain their standard of living in retirement.

-

Upper-Income Individuals:

- Lower Replacement Rate: Social Security replaces a lower percentage of pre-retirement earnings for upper-income individuals compared to lower- and middle-income individuals.

- Additional Income Sources: Upper-income individuals typically have additional sources of retirement income, such as savings, investments, and pensions, which reduce their reliance on Social Security.

- Tax Implications: Social Security benefits may be subject to income taxes for upper-income individuals, further reducing their net benefit from the program.

Overall, Social Security plays an important role in providing retirement income for individuals across different income groups. However, its impact varies depending on income level, with lower-income individuals relying more heavily on Social Security as a primary source of income.

9. What Happens If Congress Does Nothing to Address the Shortfall?

What are the consequences of inaction on Social Security? If Congress fails to take action to address the projected shortfall in Social Security, the consequences could be significant for current and future retirees.

-

Benefit Cuts:

- Across-the-Board Reductions: If the Social Security trust fund is depleted and Congress does not act, benefits will be automatically reduced across the board.

- Magnitude of Cuts: The magnitude of the benefit cuts could be substantial, potentially reducing benefits by around 20-25%.

- Impact on Retirees: Benefit cuts would have a significant impact on retirees who rely on Social Security as a major source of income, potentially leading to financial hardship.

-

Economic Consequences:

- Reduced Consumer Spending: Benefit cuts would reduce the amount of money that retirees have to spend, leading to a decline in consumer spending.

- Slower Economic Growth: Reduced consumer spending could slow down economic growth and potentially lead to a recession.

- Increased Poverty: Benefit cuts could increase poverty rates among seniors, particularly those with limited income and assets.

-

Political Consequences:

- Public Outcry: Failure to address the Social Security shortfall could lead to public outcry and political backlash.

- Erosion of Trust: It could erode public trust in government and undermine confidence in the Social Security system.

Addressing the Social Security shortfall is a complex and challenging issue, but inaction is not an option. Congress needs to act to ensure that Social Security can continue to provide benefits to current and future retirees.

10. Where Can I Learn More About Social Security and Financial Planning?

Where can I find reliable information on Social Security? For comprehensive information on Social Security and financial planning, money-central.com is your trusted resource. We offer a wide range of articles, tools, and resources to help you understand Social Security, plan for retirement, and manage your finances effectively.

-

Social Security Administration (SSA):

- Website: The SSA website (ssa.gov) provides detailed information on Social Security benefits, eligibility requirements, and how to apply.

- Publications: The SSA offers a variety of publications on Social Security topics, such as retirement planning, disability benefits, and survivor benefits.

- Online Tools: The SSA website includes online tools, such as the Retirement Estimator and the Benefit Eligibility Screening Tool, to help you estimate your benefits and determine your eligibility.

-

Financial Planning Resources at money-central.com:

- Articles and Guides: money-central.com offers a comprehensive collection of articles and guides on financial planning topics, such as budgeting, saving, investing, and retirement planning.

- Financial Calculators: Use our financial calculators to estimate your retirement savings needs, calculate your investment returns, and plan for other financial goals.

- Expert Advice: Get personalized financial advice from our team of experienced financial advisors.

-

Other Resources:

- National Council on Aging (NCOA): The NCOA (ncoa.org) provides resources and advocacy for older adults, including information on Social Security and other benefits programs.

- AARP: AARP (aarp.org) offers a variety of resources and services for older adults, including information on Social Security, Medicare, and financial planning.

By utilizing these resources, you can stay informed about Social Security and financial planning and make informed decisions about your financial future.

At money-central.com, we understand the challenges you face in managing your finances. Whether it’s understanding complex financial concepts, creating an effective budget, finding safe investment options, managing debt, or saving for retirement, we’re here to help.

Ready to take control of your financial future? Visit money-central.com today to explore our articles, use our financial tools, and connect with our experts. Let us help you achieve your financial goals. Our address is 44 West Fourth Street, New York, NY 10012, United States, and our phone number is +1 (212) 998-0000. Visit money-central.com for more information.

FAQ About Social Security Finances

- Will Social Security really run out of money?

Yes, projections indicate that Social Security’s trust funds could be depleted in the coming years if no action is taken. However, this doesn’t mean benefits will stop completely; it means benefits may be reduced. - How can I prepare for potential Social Security changes?

Start saving early, diversify your investments, consider alternative retirement plans, and stay informed about Social Security updates. - What are some potential solutions to save Social Security?

Potential solutions include raising the payroll tax rate, increasing the taxable wage base, raising the retirement age, and reducing benefit amounts. - How does immigration affect Social Security?

Immigration generally has a positive impact on Social Security by increasing the workforce and contributing payroll taxes. - What happens if Congress does nothing to address the shortfall?

If Congress does nothing, benefits will likely be reduced across the board, leading to financial hardship for many retirees. - Is Social Security the only source of retirement income I should rely on?

No, it’s important to diversify your retirement income sources, including savings, investments, and pensions. - How does Social Security affect different income groups?

Social Security provides a safety net for lower-income individuals and serves as a significant source of retirement income for middle- and upper-income earners. - Where can I find reliable information on Social Security?

Visit the Social Security Administration website (ssa.gov) and money-central.com for comprehensive information. - What is the full retirement age for Social Security?

The full retirement age is currently 67 for those born in 1960 or later. - Can I still receive Social Security benefits if I continue to work?

Yes, you can still receive Social Security benefits while working, but your benefits may be reduced if you earn above a certain limit. However, money-central.com can help you understand these stipulations and how they impact your personal financial planning.