Is 10 Million A Lot Of Money? Absolutely, $10 million represents a significant amount of wealth, positioning you in the top 1% of net worth in America and providing a solid foundation for financial security and potential early retirement. At money-central.com, we help you understand how to manage such wealth, explore investment options, and ensure a comfortable and fulfilling lifestyle. Discover strategies for wealth management, financial planning, and investment diversification to make the most of your financial resources.

1. Understanding the Significance of $10 Million

Ten million dollars is a substantial amount of money. Having a net worth of $10 million or higher places you among the top 1% of wealthiest individuals in America. If you find yourself wondering whether $10 million is sufficient for a comfortable retirement, it’s essential to recognize the financial freedom and opportunities this level of wealth provides. Many individuals who amass significant wealth face the challenge of managing it effectively and ensuring it lasts throughout their retirement years.

1.1. How Does $10 Million Compare to the Average Net Worth?

The median net worth in the United States is significantly lower than $10 million. According to the Federal Reserve, the median net worth of U.S. households was $192,900 in 2023. This stark contrast highlights the substantial advantage that $10 million provides in terms of financial security and lifestyle options.

- Median Net Worth: $192,900

- Top 1% Net Worth: Over $13 million (as of 2024)

- Your Net Worth: $10 million

Reaching a $10 million net worth is an incredible achievement. The key is understanding how to make that wealth work for you and how to plan for long-term financial well-being.

1.2. What Lifestyle Can $10 Million Afford?

With $10 million, you can afford a comfortable and luxurious lifestyle, depending on your spending habits and financial goals. Some possibilities include:

- Luxurious Living: Owning a high-end home, traveling extensively, and enjoying premium experiences.

- Financial Security: Covering healthcare costs, education for children or grandchildren, and unexpected expenses without financial strain.

- Philanthropy: Supporting charitable causes and making a significant impact on your community.

- Early Retirement: Retiring early and pursuing passions without worrying about income.

The lifestyle $10 million can afford varies greatly based on individual priorities and location. The cost of living in New York City differs significantly from that in Des Moines, Iowa. Understanding your priorities and planning accordingly is crucial.

2. Retirement Planning with $10 Million

Retiring with $10 million requires careful planning to ensure your wealth lasts throughout your retirement. Key considerations include investment strategy, withdrawal rates, and managing expenses.

2.1. Assessing Your Retirement Needs

Before making any decisions, evaluate your retirement needs and goals. This includes estimating your annual expenses, accounting for inflation, and planning for healthcare costs.

- Estimate Annual Expenses: Determine how much you need to cover your living expenses each year.

- Account for Inflation: Factor in the rising cost of goods and services over time.

- Plan for Healthcare Costs: Healthcare expenses can be significant in retirement, so it’s crucial to have a plan.

Understanding your needs is the first step in creating a sustainable retirement plan. Resources like the AARP Retirement Calculator can help you estimate your expenses and plan accordingly.

2.2. Investment Strategies for Retirement Income

Investing your $10 million wisely is essential for generating a sustainable income stream. Diversification is key to managing risk and maximizing returns.

- Diversify Investments: Allocate your assets across various investment types, including stocks, bonds, and real estate.

- Consider Income-Producing Assets: Focus on investments that generate regular income, such as dividend stocks, REITs, and bonds.

- Rebalance Portfolio Regularly: Adjust your asset allocation periodically to maintain your desired risk level and investment goals.

A well-diversified portfolio can provide a steady income stream while preserving your capital. Financial advisors at money-central.com can help you create a customized investment strategy tailored to your needs.

Diversified investment portfolio

Diversified investment portfolio

2.3. Safe Withdrawal Rates

The withdrawal rate is the percentage of your savings you withdraw each year for living expenses. A safe withdrawal rate ensures you don’t outlive your money.

- The 4% Rule: A commonly cited guideline suggests withdrawing 4% of your savings each year, adjusted for inflation.

- Adjust for Your Situation: Consider your life expectancy, risk tolerance, and other income sources when determining your withdrawal rate.

- Monitor and Adjust: Regularly review your withdrawal rate and adjust as needed based on market conditions and your financial situation.

A prudent withdrawal strategy is crucial for long-term financial security. Studies by financial institutions like Vanguard provide insights into sustainable withdrawal rates based on historical market data.

3. Maximizing Your $10 Million: Investment Options

To make the most of your $10 million, consider various investment options that offer growth potential and income generation.

3.1. Real Estate Investments

Real estate can be a valuable addition to your investment portfolio, providing both income and appreciation potential.

- Rental Properties: Investing in rental properties can provide a steady stream of income and potential capital appreciation.

- REITs (Real Estate Investment Trusts): REITs allow you to invest in a portfolio of real estate assets without directly owning properties.

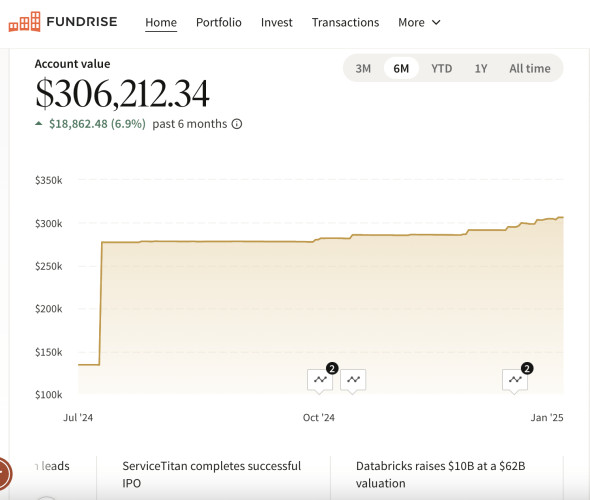

- Real Estate Crowdfunding: Platforms like Fundrise and CrowdStreet offer opportunities to invest in real estate projects with lower minimum investments.

According to research, real estate investments have historically provided competitive returns and can act as a hedge against inflation.

3.2. Stock Market Investments

Investing in the stock market can provide long-term growth potential and dividend income.

- Diversified Stock Portfolio: Create a diversified portfolio of stocks across various sectors and industries.

- Dividend Stocks: Invest in companies that pay regular dividends, providing a steady income stream.

- ETFs (Exchange-Traded Funds): ETFs offer a convenient way to invest in a basket of stocks that track a specific index or sector.

Historical data shows that stocks have outperformed other asset classes over the long term. However, it’s essential to manage risk through diversification and consider your risk tolerance.

3.3. Bond Investments

Bonds are generally considered less risky than stocks and can provide a stable income stream.

- Government Bonds: Bonds issued by the U.S. government are considered low-risk and provide a fixed income stream.

- Corporate Bonds: Bonds issued by corporations can offer higher yields than government bonds but also carry more risk.

- Bond Funds: Bond funds offer diversification and professional management.

Bonds can provide stability to your portfolio and act as a hedge during economic downturns.

3.4. Alternative Investments

Consider alternative investments for diversification and potential higher returns.

- Private Equity: Investing in private companies can offer significant growth potential but also carries higher risk and illiquidity.

- Hedge Funds: Hedge funds employ various strategies to generate returns and may offer diversification benefits.

- Commodities: Investing in commodities like gold, oil, and agricultural products can provide a hedge against inflation.

Alternative investments can enhance portfolio returns but require careful due diligence and understanding of the risks involved.

4. Managing Your Wealth Effectively

Effective wealth management involves not only investing wisely but also managing taxes, estate planning, and protecting your assets.

4.1. Tax Planning

Minimize your tax liability through effective tax planning strategies.

- Tax-Advantaged Accounts: Utilize tax-advantaged retirement accounts like 401(k)s and IRAs to defer or avoid taxes on investment gains.

- Tax-Loss Harvesting: Sell investments that have declined in value to offset capital gains and reduce your tax bill.

- Charitable Giving: Donate to charitable organizations to receive tax deductions.

According to the IRS, understanding and utilizing available tax deductions and credits can significantly reduce your tax burden.

4.2. Estate Planning

Ensure your assets are distributed according to your wishes through proper estate planning.

- Will: Create a will to specify how your assets should be distributed after your death.

- Trust: Establish a trust to manage and distribute your assets, potentially avoiding probate and reducing estate taxes.

- Power of Attorney: Designate someone to manage your financial affairs if you become incapacitated.

Estate planning ensures your loved ones are taken care of and your assets are protected. Consulting with an estate planning attorney is crucial to create a comprehensive plan.

4.3. Asset Protection

Protect your assets from potential creditors and lawsuits.

- Insurance: Maintain adequate insurance coverage, including liability insurance, to protect against potential claims.

- Asset Protection Trusts: Consider establishing asset protection trusts to shield your assets from creditors.

- Limited Liability Companies (LLCs): Use LLCs to hold business assets and protect your personal assets from business liabilities.

Asset protection strategies can safeguard your wealth and provide peace of mind.

5. Common Financial Challenges and How to Overcome Them

Even with $10 million, it’s essential to be aware of potential financial challenges and how to address them.

5.1. Inflation Risk

Inflation can erode the purchasing power of your savings over time.

- Invest in Inflation-Resistant Assets: Consider investing in assets that tend to perform well during inflationary periods, such as real estate, commodities, and inflation-indexed bonds.

- Adjust Withdrawal Rate: Periodically review and adjust your withdrawal rate to account for inflation.

The Bureau of Labor Statistics provides data on inflation rates, allowing you to plan accordingly.

5.2. Market Volatility

The stock market can be volatile, and market downturns can impact your portfolio value.

- Diversify Your Portfolio: Diversification can help mitigate the impact of market volatility on your portfolio.

- Maintain a Long-Term Perspective: Avoid making rash decisions based on short-term market fluctuations.

- Rebalance Regularly: Rebalancing your portfolio can help you stay on track with your investment goals.

Historical data shows that the stock market tends to recover over the long term. Maintaining a long-term perspective is crucial.

5.3. Longevity Risk

Living longer than expected can deplete your savings.

- Plan for a Long Retirement: Estimate your life expectancy and plan accordingly.

- Consider Annuities: Annuities can provide a guaranteed income stream for life.

- Maintain a Healthy Lifestyle: Staying healthy can help you live longer and reduce healthcare costs.

The Social Security Administration provides life expectancy calculators to help you estimate how long you might live.

5.4. Healthcare Costs

Healthcare costs can be significant in retirement.

- Purchase Adequate Health Insurance: Ensure you have adequate health insurance coverage, including Medicare and supplemental policies.

- Consider Long-Term Care Insurance: Long-term care insurance can help cover the costs of nursing home care or in-home care.

- Plan for Healthcare Expenses: Set aside funds specifically for healthcare expenses.

According to Fidelity Investments, healthcare costs can be a significant expense in retirement. Planning accordingly is essential.

6. Seeking Professional Financial Advice

Navigating the complexities of managing $10 million can be challenging. Seeking professional financial advice can provide valuable guidance and support.

6.1. Benefits of Working with a Financial Advisor

- Expertise and Knowledge: Financial advisors have the expertise and knowledge to help you make informed decisions about your finances.

- Customized Financial Plan: A financial advisor can create a customized financial plan tailored to your specific needs and goals.

- Objective Advice: Financial advisors can provide objective advice without emotional biases.

- Ongoing Support: A financial advisor can provide ongoing support and guidance as your financial situation changes.

A study by Vanguard found that working with a financial advisor can lead to higher investment returns and improved financial outcomes.

6.2. How to Choose the Right Financial Advisor

- Credentials and Experience: Look for a financial advisor with relevant credentials and experience, such as a Certified Financial Planner (CFP).

- Fiduciary Duty: Ensure the financial advisor has a fiduciary duty to act in your best interests.

- Fee Structure: Understand how the financial advisor is compensated, whether through fees, commissions, or a combination of both.

- Client References: Ask for client references to get feedback on the financial advisor’s services.

Choosing the right financial advisor is crucial for achieving your financial goals. Resources like the National Association of Personal Financial Advisors (NAPFA) can help you find qualified advisors.

7. Making the Most of Retirement

Retirement is not just about financial security; it’s also about enjoying your time and pursuing your passions.

7.1. Pursuing Hobbies and Interests

- Travel: Explore new destinations and cultures.

- Volunteer: Give back to your community and make a difference.

- Learn New Skills: Take classes or workshops to learn new skills and stay mentally active.

- Spend Time with Loved Ones: Enjoy quality time with family and friends.

Research shows that staying active and engaged in retirement can improve your physical and mental health.

7.2. Staying Active and Healthy

- Exercise Regularly: Engage in regular physical activity to maintain your health and fitness.

- Eat a Balanced Diet: Consume a nutritious diet to support your overall well-being.

- Get Enough Sleep: Prioritize sleep to maintain your physical and mental health.

- Manage Stress: Practice stress-reducing techniques like meditation and yoga.

Maintaining a healthy lifestyle can help you enjoy a longer and more fulfilling retirement.

7.3. Giving Back to the Community

- Volunteer Your Time: Volunteer at local organizations and make a positive impact on your community.

- Donate to Charitable Causes: Support charitable causes that are important to you.

- Mentor Others: Share your knowledge and experience with others.

Giving back to the community can provide a sense of purpose and fulfillment in retirement.

8. Real-Life Examples of Successful Retirements with $10 Million

To illustrate the possibilities of retiring with $10 million, let’s look at some real-life examples.

8.1. Case Study 1: The Early Retiree

- Background: A 45-year-old who accumulated $10 million through a successful tech startup.

- Retirement Plan: Invested in a diversified portfolio of stocks, bonds, and real estate, generating an annual income of $400,000.

- Lifestyle: Travels extensively, pursues hobbies like photography and hiking, and volunteers at a local charity.

This individual demonstrates the potential for early retirement with careful planning and investment management.

8.2. Case Study 2: The Philanthropist

- Background: A 60-year-old who accumulated $10 million through a successful business career.

- Retirement Plan: Established a charitable foundation to support education and healthcare initiatives.

- Lifestyle: Spends time traveling, mentoring young entrepreneurs, and managing the foundation.

This individual shows how wealth can be used to make a significant impact on the community.

8.3. Case Study 3: The Family-Focused Retiree

- Background: A 55-year-old who accumulated $10 million through a combination of savings, investments, and inheritance.

- Retirement Plan: Invested in a diversified portfolio of stocks, bonds, and real estate, generating an annual income of $350,000.

- Lifestyle: Spends time with family, travels with grandchildren, and enjoys hobbies like gardening and cooking.

This individual highlights the importance of family and personal fulfillment in retirement.

9. Navigating Unexpected Financial Challenges

Even with careful planning, unexpected financial challenges can arise.

9.1. Dealing with a Sudden Market Downturn

- Stay Calm: Avoid making impulsive decisions during market downturns.

- Rebalance Your Portfolio: Rebalance your portfolio to maintain your desired asset allocation.

- Consider Tax-Loss Harvesting: Use tax-loss harvesting to offset capital gains and reduce your tax bill.

Historical data shows that the stock market tends to recover over the long term. Staying calm and maintaining a long-term perspective is crucial.

9.2. Managing Unexpected Healthcare Expenses

- Review Your Health Insurance Coverage: Ensure you have adequate health insurance coverage to protect against unexpected healthcare expenses.

- Consider a Health Savings Account (HSA): An HSA can provide tax advantages for healthcare savings.

- Create an Emergency Fund: Set aside funds specifically for unexpected healthcare expenses.

Having a plan in place for unexpected healthcare expenses can provide peace of mind and financial security.

9.3. Supporting Family Members in Need

- Assess Your Financial Situation: Evaluate your financial situation before providing financial assistance to family members.

- Set Clear Boundaries: Set clear boundaries and expectations regarding financial assistance.

- Consider Gift Tax Implications: Be aware of gift tax implications when providing financial assistance to family members.

Providing financial assistance to family members requires careful consideration and planning.

10. How money-central.com Can Help You Manage Your Wealth

At money-central.com, we provide the resources and tools you need to manage your wealth effectively and achieve your financial goals.

10.1. Financial Planning Tools and Calculators

- Retirement Calculator: Estimate your retirement needs and plan accordingly.

- Investment Calculator: Project the potential growth of your investments.

- Budgeting Tool: Track your income and expenses to stay on top of your finances.

- Net Worth Calculator: Calculate your net worth and track your progress over time.

Our financial planning tools and calculators can help you make informed decisions about your finances.

10.2. Articles and Guides on Wealth Management

- Investment Strategies: Learn about different investment strategies and how to build a diversified portfolio.

- Tax Planning: Discover tax-saving strategies to minimize your tax liability.

- Estate Planning: Understand the importance of estate planning and how to create a comprehensive plan.

- Asset Protection: Learn how to protect your assets from potential creditors and lawsuits.

Our articles and guides provide valuable insights and information on wealth management topics.

10.3. Access to Financial Experts

- Connect with Financial Advisors: Find qualified financial advisors who can provide personalized advice and guidance.

- Ask Our Experts: Get answers to your financial questions from our team of experts.

- Attend Webinars and Workshops: Participate in webinars and workshops to learn about various financial topics.

Our network of financial experts can help you make informed decisions and achieve your financial goals.

Address: 44 West Fourth Street, New York, NY 10012, United States

Phone: +1 (212) 998-0000

Website: money-central.com

By leveraging the resources and expertise available at money-central.com, you can effectively manage your $10 million and achieve your financial goals.

FAQ: Is 10 Million A Lot Of Money?

FAQ 1: Is 10 million dollars enough to retire comfortably?

Yes, $10 million is generally enough to retire comfortably, as it can generate a substantial income stream through investments, ensuring financial security and a comfortable lifestyle.

FAQ 2: How can I invest $10 million for retirement income?

Diversify your investments across stocks, bonds, real estate, and alternative assets to generate a sustainable income stream while managing risk.

FAQ 3: What is a safe withdrawal rate for a $10 million portfolio?

A 4% withdrawal rate is often recommended, which would provide $400,000 per year, but it’s essential to adjust based on your individual circumstances and market conditions.

FAQ 4: How can I protect my $10 million from inflation?

Invest in inflation-resistant assets such as real estate, commodities, and inflation-indexed bonds, and periodically adjust your withdrawal rate to account for inflation.

FAQ 5: What are the tax implications of having $10 million?

Implement tax-efficient investment strategies, utilize tax-advantaged accounts, and consult with a tax professional to minimize your tax liability.

FAQ 6: Should I hire a financial advisor to manage my $10 million?

Yes, a financial advisor can provide expert guidance, create a customized financial plan, and offer ongoing support to help you achieve your financial goals.

FAQ 7: How can I ensure my wealth lasts throughout my retirement?

Create a well-diversified investment portfolio, maintain a prudent withdrawal rate, and plan for unexpected expenses to ensure your wealth lasts throughout your retirement.

FAQ 8: What are the key considerations for estate planning with $10 million?

Create a will or trust, designate a power of attorney, and plan for estate taxes to ensure your assets are distributed according to your wishes and your loved ones are protected.

FAQ 9: How can I give back to the community with my wealth?

Volunteer your time, donate to charitable causes, and consider establishing a charitable foundation to make a positive impact on your community.

FAQ 10: What are some common financial challenges faced by high-net-worth individuals?

Common challenges include managing inflation risk, market volatility, longevity risk, and healthcare costs, all of which require careful planning and proactive management.

By understanding these key aspects and utilizing the resources available at money-central.com, you can effectively manage your $10 million, navigate potential challenges, and enjoy a fulfilling and financially secure retirement. Remember, financial freedom is not just about the money; it’s about the peace of mind and opportunities it provides.

If you are ready to build more wealth than 90% of the population, grab a copy of my new book, Millionaire Milestones: Simple Steps to Seven Figures. With over 30 years of experience working in, studying, and writing about finance, I’ve distilled everything I know into this practical guide to help you achieve financial success.

Millionaire Milestone – Bestseller On AmazonClick the image and order a copy on Amazon today

Millionaire Milestone – Bestseller On AmazonClick the image and order a copy on Amazon today